@elevamiami Público da sw4 e da pajero sao conservadores o bastante pra trocar pelo mesmo carro. O público que sobra pra gwm vai desanimar pelo motor mais manco... pecou nesse detalhe.

@ZattarRafael Eu uso grafico como medidor de pânico/euforia. As médias móveis e o distanciamento do preço auxiliam em obter sempre o melhor risco:retorno nas operações. Canso de ver colegas que acertam o trade por fundamentos mas passam por um desnecessário drawdown...

Brazil’s illegal shut down of @X and account freeze at Starlink put Brazil on a rapid path to becoming an uninvestable market. China committed similar acts leading to capital flight and a collapse in valuations. The same will happen to Brazil unless they quickly retreat from these illegal acts.

@HeglerHenri Petro tem um histórico de grande queda por influência política quase que todo ano nos últimos 20 anos... Antes disso sempre sofre bastante ruído, independente do governo, essas "apostas" sempre ocorreram. O cara com um PL alto pode fazer essas especulações normalmente

@vladluxx Nunca gostei de fone intra auricular, sempre incomodou num uso mais prolongado e isso me fazia sempre usar airpods, até experimentar o Galaxy Buds 2 PRO que veio junto com o celular... cancelamento de ruído + conforto + bateria excelentes, além de mais em conta.

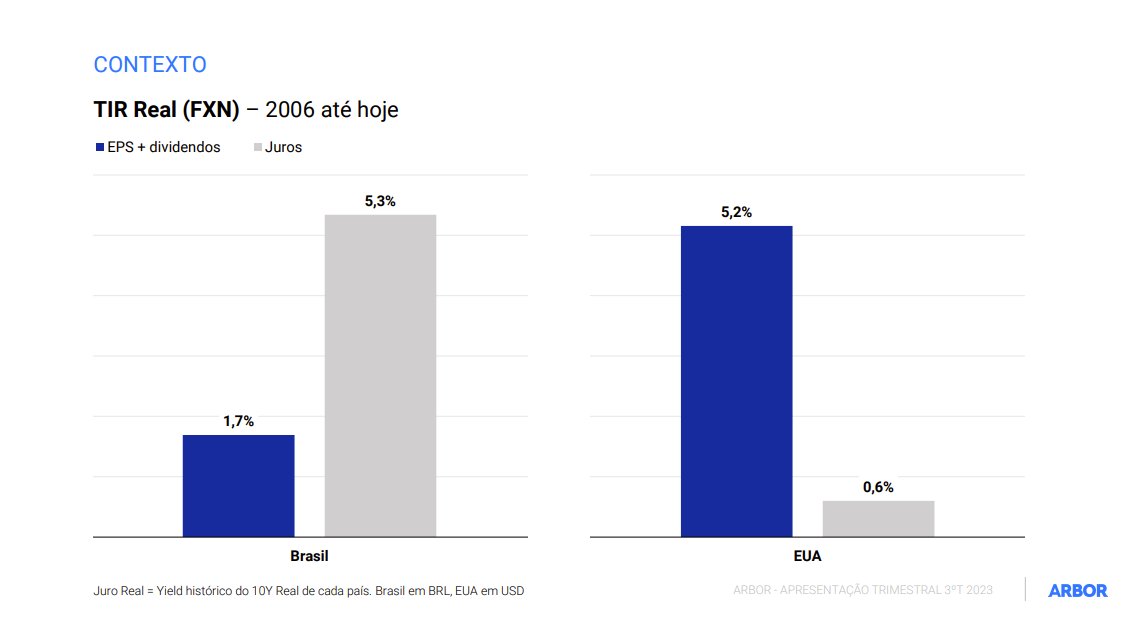

Essa imagem é muito importante para todo mundo que investe em ações.

Comparamos o crescimento real de lucro do bovespa com o juro real brasileiro desde 2006. Fizemos a mesma comparação para o índice S&P500.

Na ausência de variação no múltiplo P/E, e assumindo o repasse de inflação nos preços/receita. Para uma ação superar o juro real, o lucro precisa crescer em uma taxa superior ao juro.

Na imagem mostramos que o lucro das empresas brasileiras não crescem rapido o suficiente.Lucro real bovespa: 1,7% - vs - Juro real Brasil: 5,3%

Algumas hipóteses do motivo por trás dessa underperformance da bolsa vs renda fixa.

1) Falta de capital humano: No Brasil, há uma carência de profissionais especializados nas indústrias de fronteira. Essa falta de capital humano exerce uma desvantagem competitiva nas empresas brasileiras. E o pouco capital humano, muitas vezes estuda fora e fica por lá.

2) Empresas em setores de baixo valor agregado: Conforme apontado por estudos, como o realizado pelo Damodaran, as empresas brasileiras estão em setores de baixo valor agregado. Isso implica, em retornos sobre o capital investido baixoa. Assim, o potencial de retorno para o investidor é baixo tambem, tornando o mercado de ações local cíclico e muito ligado ao preço das principais comodities.

3) O fato dos juros aqui serem muito altos inviabiliza que as empresas se beneficiem de um componente importante de valor – a engenharia financeira. A tática mais comum utilizada nos EUA são as recompras de ações. Ao seguir uma estratégia como essa, o balanço da companhia é otimizado e o retorno para o acionista aumenta. Conforme acontece nos fundos de private equity..

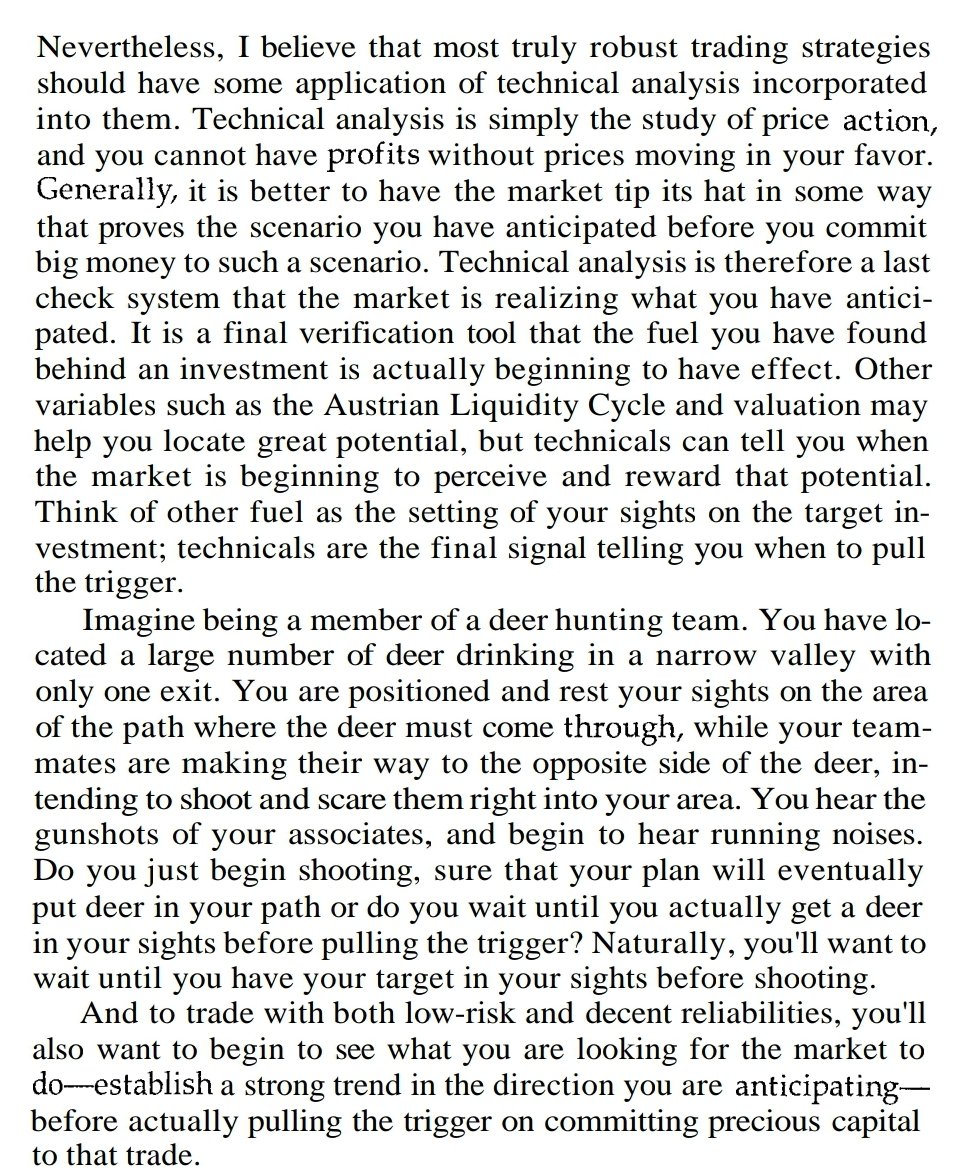

This week's main event, the CPI, was overshadowed by a mid-day government bond issuing gone poorly. The CPI came in a little hotter than expected, but Core was in line at 4.1%. The interesting thing about economics is data manipulation. An old joke is that two economists see a bird in the sky. One shoots a foot to the left, and the other shoots a foot to the right. They both missed but celebrated as, on average, they had two perfect shots. The point is the details of these data releases can become critical when so much depends on them. According to Ophir Gottlieb of Capital Market Laboratories,

"shelter inflation is now 70% of total inflation over the past 12 months. When shelter inflation is computed using the private indices (like Zillow and ApartmentList), CPI is now 1.5% over the last year; below Fed target and is 1.1% annualized over the last six months."

That's a major discrepancy and a critical one regarding how much is dependent on the inflation data. I think the market recognizes it, and that is why, despite the slightly hotter-than-expected CPI, markets started the day positively. The trigger that caused the market to roll over hard was the bad Government bond auction that indicated higher interest rates. In my view, despite CPI grabbing all the headlines, the market is more concerned about higher rates, which can induce a recession, rather than resurgent inflation.

The Russell 2000 is the most representative of stocks impacted by a slowing economy, and it fell off a cliff with a 2.26% drop. Needless to say, net lows continued on both exchanges.

So, is it all bad? Well, it could have been better without the poor bond auction, but CPI having less of an impact is a huge step forward. Inflation is the dragon that needs to be slayed. It is the genie that can't be let out of the lamp because it can feed on itself and grow uncontrollably.

We need to watch whether bond yields continue to expand, but the main concern definitely seems to be changing. The good news is that climbing yields will result in a dovish FED, partly neutralizing its climb. This doesn't mean a surge in yields can't hurt stocks, but we need to be aware of the change.

There is another important part of this development. Whenever the main reason for concern changes, that impacts stock rotations. Under the surface, smart investors begin shifting capital to stocks that will be less affected by the new 'problem.' Take a look at the leading stocks, and you'll notice that all of the biggest losers today were recent winners and are all linked to the economy or commodities. On the other hand, higher growth technology stocks were relatively unscathed, given the Russell 2000 drop. This may change, but this rotation and the new trend must be closely watched as it typically precedes bull markets in growth names.

A strong move higher from here could be a great expectation breaker after today's action, and I want to be prepared for it. On the downside, my remaining pullback buys have all been showing outstanding relative action. If markets don't deteriorate much further, I am still happy to do some buying on a pullback in leading names. This will be a day-by-day analysis as we remain with net lows but above our recent follow-through day - an undecided position.

The key remains to identify the changing market dynamics, identify leaders, and focus on low-risk setups with controlled overall exposure (maintaining adequate cash positions given conditions). We remain in control, and we know when our plans have failed. We are empowered to act. No fear, just decisive action with objective data.

$NTNX $TTD $UBER $META $NVE $LLY

@ManfroiRenato Se fosse tão simples assim... como ficariam os repasses aos municípios nesse caso? E se a exploração de petróleo na margem equatorial for sucesso, como ficariam os royalties? Essas regiões usufruem muito menos do que produzem + corruptos perpetuando no poder por lá, da nisso.

Continuing to track price leadership names in combination with the highly liquid institutional darlings...

Bunch of 'top dogs' in this list worth $STUDY

Will chart them out w/ some extra thoughts ↓

$DUOL

$SQSP

$ONON

$ALGM

$AI

$FSLR

$NVDA

$TSLA

$FOUR

$LNTH

$ELF

@ZattarRafael Uso o inter e cora, em dois PJ. Ambos me atendem muito bem, so far so good. Acho q depende mto do negócio... O meu é em shopping e preciso de sangria o tempo todo, então ambas me dão essa possibilidade com custo reduzido. (Deposito via boleto).