In America, a warehouse store. A fully roasted chicken costs five dollars, the raw chicken beside it costs seven, and I stood between them like a man between two truths.

Golden. Hot. Seasoned. Spinning in glory under the lights, in a line of its brothers. Four dollars and ninety-nine cents.

I checked the raw birds. Seven dollars. Pale. Cold. You must do everything yourself.

This is not commerce. Commerce does not move backward. Somewhere in this building, mathematics lies defeated.

I asked the man at the counter. "How is the cooked bird cheaper than the raw bird?"

"Been five bucks forever. They keep it that way."

"But the store loses."

"Yep. On purpose."

On purpose. I held my receipt with both hands.

In my land, a lord who lowered the price of rice in a hard winter was remembered for generations. They built him a small shrine. This store does it every day, with chicken, and tells no one.

A woman behind me grew tired of my reverence. "It's just a chicken, sir."

It is not just a chicken. It is a wound the merchant takes on purpose, so that anyone, on any day, with five dollars, eats like a lord. The bird is the message. The price is the vow.

I will confess: I bought two. I did not need two. The second was not hunger. It was gratitude, and it was delicious.

Some prices are not prices. They are promises.

I return every week now. I take one bird. I bow toward the deli, briefly, so as not to alarm the staff. They have begun nodding back.

The vow holds. The bird turns. Five dollars.

Long may it spin.

Brazil's domestic payment system became the target of a formal U.S. trade investigation in July 2025.

The payment system is called Pix.

The central bank built it and runs it.

Individuals pay nothing to use it.

Merchants pay roughly 0.33 percent per transaction, compared to about 2.34 percent for credit cards.

It settles instantly, 24 hours a day, 7 days a week.

In 2024, Pix processed about 64 billion transactions.

That is more transactions than Visa and Mastercard handled in Brazil combined.

A small in-house team at the Central Bank designed it from scratch and launched it in November 2020.

Five years later, 93 percent of Brazilian adults use it.

Cash use in Brazil fell from 43 percent of payments to 6 percent over those same five years.

The U.S. Trade Representative argues that Pix gives an unfair advantage to Brazilian firms over American payment companies.

A formal Section 301 investigation began on July 15, 2025.

A public hearing was held in Washington on September 3, 2025.

Banco do Brasil has already launched Pix for cross-border payments in Argentina.

The Central Bank is studying expansion to other countries in the Americas, Europe, and Asia.

Brazil built the rail, the world is studying the model, and the United States is investigating the result.

Most capital allocators model Brazil on commodity exports.

The bigger export story may be the payment system.

.@PalmerLuckey: "Patents are Chinese instruction manuals" and we need to reinvent the US patent system:

"Stop patenting everything."

"The Founding Fathers never predicted a world where you'd have a globalized economy, and the entire patent office could be downloaded every single morning, ripped off, and then used to fight a war against you."

" We need to really fundamentally revisit the patent system."

"I think we need to massively expand the national security patent process. You can obtain a classified patent. You can get a patent on something that you are not allowed to disclose to anyone, but you still maintain the exclusivity on those rights."

" We need to massively expand that program."

Via @HooverInst

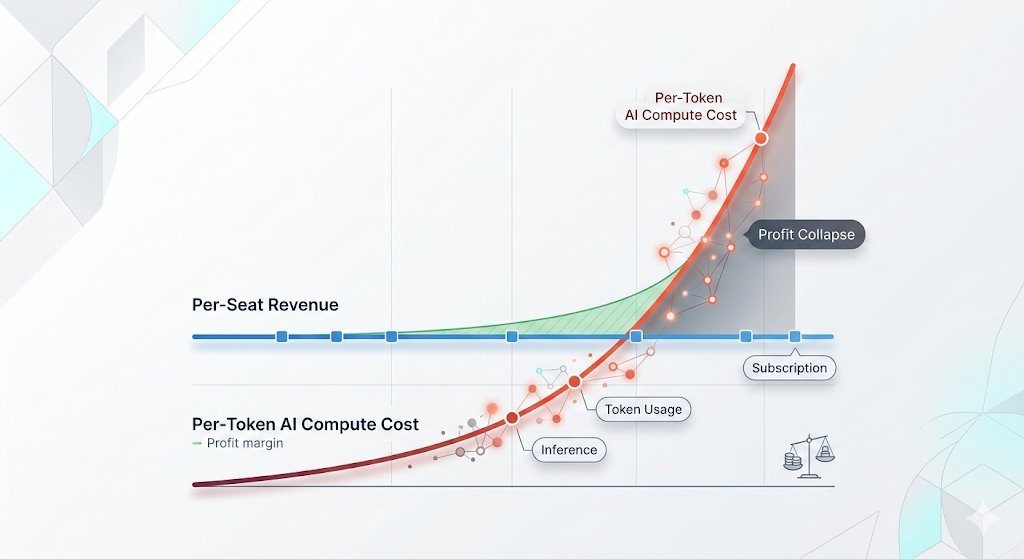

The AI cloud trap is snapping shut. 🪤

When even Microsoft and Uber choke on usage-based billing, the pendulum swings back to owning bare-metal compute. Predictable CapEx > infinite OpEx. Renting your brain is just too expensive. 🧠💻

Hedgie🤗

🦔Microsoft canceled its internal Claude Code licenses this week after token-based billing made the cost untenable, even for a company with effectively infinite cloud resources. Uber's CTO sent an internal memo warning the company burned through its entire 2026 AI budget in just four months. American AI software prices have jumped 20% to 37%, and GitHub (owned by Microsoft) is dropping flat-rate plans for usage-based billing across its products.

My Take

The AI subsidy era is ending in real time. The same company that put $13 billion into OpenAI and built the Azure infrastructure powering most of Anthropic's compute just looked at the bill from a competitor's coding tool and decided it was not worth paying. That is not a productivity failure on Anthropic's end. Token-based pricing is forcing every enterprise customer to confront the actual cost of running these models at scale, and the number turns out to be far higher than the flat-rate experiments suggested.

This ties directly to my Gemini Flash post yesterday. Anthropic, OpenAI, and Google all raised effective prices in the last six months. Enterprises that built workflows assuming AI costs would keep falling are now watching annual budgets evaporate in months. Two outcomes look likely from here. Either enterprises scale back AI usage to fit budgets, which slows the revenue ramp the labs need to justify their valuations ahead of IPOs, or the labs cut prices and absorb the losses, which makes the unit economics worse at exactly the wrong moment. Both paths land in the same place, the numbers stop working, and somebody has to take the writedown.

Hedgie🤗

Second-time Founders is my favourite gender :

1) no deck until someone asks three times

2) first hire is a lawyer

3) distribution for the product before the product exists

4) "we don't need a big round" and means it this time

5) replies to every customer email personally because they know what ignoring customers cost them last time

6) sleeps 8 hours and ships faster than everyone else

7) the only person in the room who isn't impressed by the term sheet

Second-time founders are the best breed of founders

Brazil built the kind of payment infrastructure the US still doesn’t have.

Pix made payments instant, cheap, and easy to use at scale..

That’s why X Money is interesting. If it ever becomes more than just another layer on top of the old rails…

Brazil's Pix processes 6-7 billion transactions per month.

Venmo, CashApp, and Zelle combined don't come close.

India's UPI took six years and eight months to reach 8 billion monthly transactions.

Brazil got there in five.

170 million Brazilians use Pix.

That's 93% of the adult population.

Merchant fees average 0.33% (cards charge 2-5%).

Transactions settle in seconds.

On December 20, 2024, the system processed 252.1 million transactions in a single day.

That one day exceeds the entire monthly volume of most European instant payment systems.

Then they built Open Finance on top of it. 60+ million active data-sharing consents.

Four times the API volume of the UK's Open Banking.

Nubank (built entirely on this public infrastructure) now serves 110 million customers, posted $895 million in quarterly profit, and carries an $85 billion valuation.

The most valuable financial institution in Latin America was founded 13 years ago by three people with no bank.

The Fed launched FedNow three years after Pix. Adoption remains minimal.

The US has no Open Finance mandate.

No active CBDC pilot.

Brazil is two full technology cycles ahead of the United States in public financial infrastructure.

The next time someone tells you Brazil is a "risky emerging market," ask them if they know what Pix is.

Read more here:

https://t.co/R8eWsrQi7i

@antonia_mdprjct More workers on site often means more coordination problems than progress. This is why experienced developers don't just throw bodies at delays.

@coreyganim Restaurants and salons are sleeping on this. The perception gap between what they think it costs vs actual cost is the entire business opportunity.