Dear @Infosys_GSTN , @cbic_india

Why the system is making the blocks red when I am myself setting off the liabilities using rule 88A ? (not using system suggested figures)

Further the error calls me pay IGST tax when there is no IGST liability.

@abhishekrajaram

How much Gold Jewellery and Ornaments you can hold legally without proof?

As per many High Court Judgements, & CBDT Instruction No 1916

Married Women – 500 grams

Unmarried Women – 250 grams

Male Member – 100 grams

For example, in a family consisting of a Father, Mother, Married Son & his Wife and unmarried Daughter, total 5 members can hold

2 Married Women – 500 *2 = 1000 gms

2 Male Member – 100*2 = 200 gms

1 Unmarried Women = 250*1 = 250 gms

Total = 1450 gms of Gold Jewellery

The CBDT guidelines in Instruction No 1916 define the limits for Search operation and seizure and not for assessment, however, various High Court rulings considering Indian Traditions and Customs are of the opinion that such holding found in possession will not be questioned for its source and acquisition.

The quantities specified in the instruction are to be treated as reasonable and therefore explained and should not be the subject matter of additions during assessments

As per Hindu Tradition, gold is given as streedhan or inherited via Will or else received as gift during marriage or other occasions as customary practice since time immemorial. Many times the invoice or proof of buying is not available. In such cases, the limits as mention above can be assumed as reasonable as per Hindu traditions and the status of the family.

Note the above limits are applicable only for Gold Jewellery in form of ornaments and not for Gold coins or bars.

Further, there is no ceiling or limit upto which you can own Gold Jewellery and Ornaments or Gold Coins or Bars provided it is acquired from the explained source of income and inheritance (Eg proof like bills and Will), meaning legitimate holding of Gold to any extent is permissible and protected

#Tax #GoldTax #Gold #GoldHolding

🚨Sunday Special: High Court favors petitioners in recent Indian Input Tax Credit (ITC) cases under GST!

🚨 Stay updated with these latest case laws and their citations in this thread 🧵👇

What to do with inappropriate/baseless GST Reg rejection order passed by superintendent? How to proceed with such negligence by CGST officer of CPC Cell? Where to raise the issue/complaint?

Officer asking docs on Call but not under SCN.

@Infosys_GSTN@cbic_india@abhishekrajaram

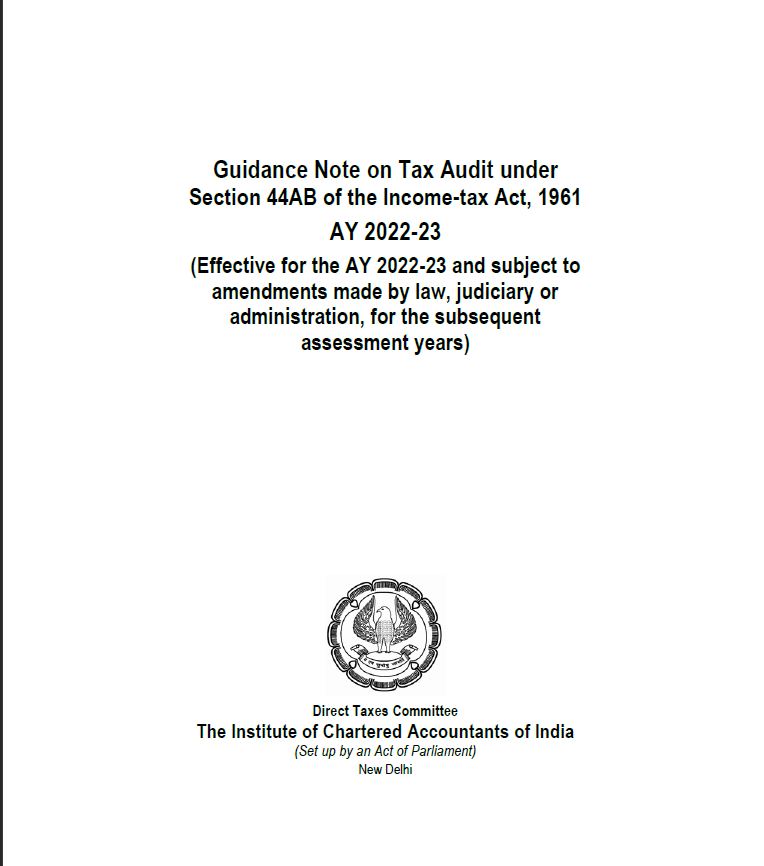

A Thread 🧵on Clause 44 of Form 3CD as per Guidance Note issued by @theicai today

Guidance Note issued after 8 years, last GN was issued in 2014

Link to download the same is here: https://t.co/fNpBNHH5yY

@cbic_india@Infosys_GSTN

The ticket is still open even after 1 week and is not yet resolved.

What is the implication of Sec 28(1) r.w.r. 19 for this delay ?

@cbic_india@Infosys_GSTN

The ticket is still open even after 1 week and is not yet resolved.

What is the implication of Sec 28(1) r.w.r. 19 for this delay ?

@cbic_india@Infosys_GSTN

I want to change principal place of business address along with state jurisdiction but the related columns are shown as blocked fields for editing.

My earlier application already rejected on account of wrong state jurisdiction.

Kindly correct system.

@cbic_india@Infosys_GSTN

I want to change principal place of business address along with state jurisdiction but the related columns are shown as blocked fields for editing.

My earlier application already rejected on account of wrong state jurisdiction.

Kindly correct system.

#Inspection of Goods in transit

Hon'ble P&H HC has held that if the goods are accompanied with Bill and EWB, then authorities should not proceed to make case u/s 129.

Useful judgment for industry and professionals.

CWP NO. 18392/2021, Dt. 04.02.2022

[2022] 134 https://t.co/ZuVjoLq17G 42 (Calcutta) HIGH COURT OF CALCUTTA-LGW Industries Ltd. v. Union of India

Gist of Cases referred by Petitioner on Validity of Input Tax Credit in Genuine Transaction..Must to be referred in submissions..Thread contains reference to decisions.

Rely law not circular. One more time view on limitation vindicated.

Time period for filing of Refund gets extended by the order of hon'ble SC in SMWP No. 3/2020.

After madras, now hon'ble Bom HC also confirms same in case of Saiher Supply Consulting PL Vs. UOI.