Lava Card earns you bitcoin with every purchase.

Last week we announced 5% back in BTC on all purchases at Apple, Amazon, and Netflix for all users.

Next week we're announcing even more.

Build up your long-term BTC savings every time you spend. Live now for everyone.

Ethena has partnered with Janus Henderson, a $480 billion asset manager, to allocate and support the distribution of their liquid high-quality CLO tokenized funds.

As part of the partnership Janus Henderson has made a strategic investment into Ethena's governance token, will allocate into USDe as part of their treasury cash management, and is also exploring avenues to distribute USDe to their client base via exchange traded instruments.

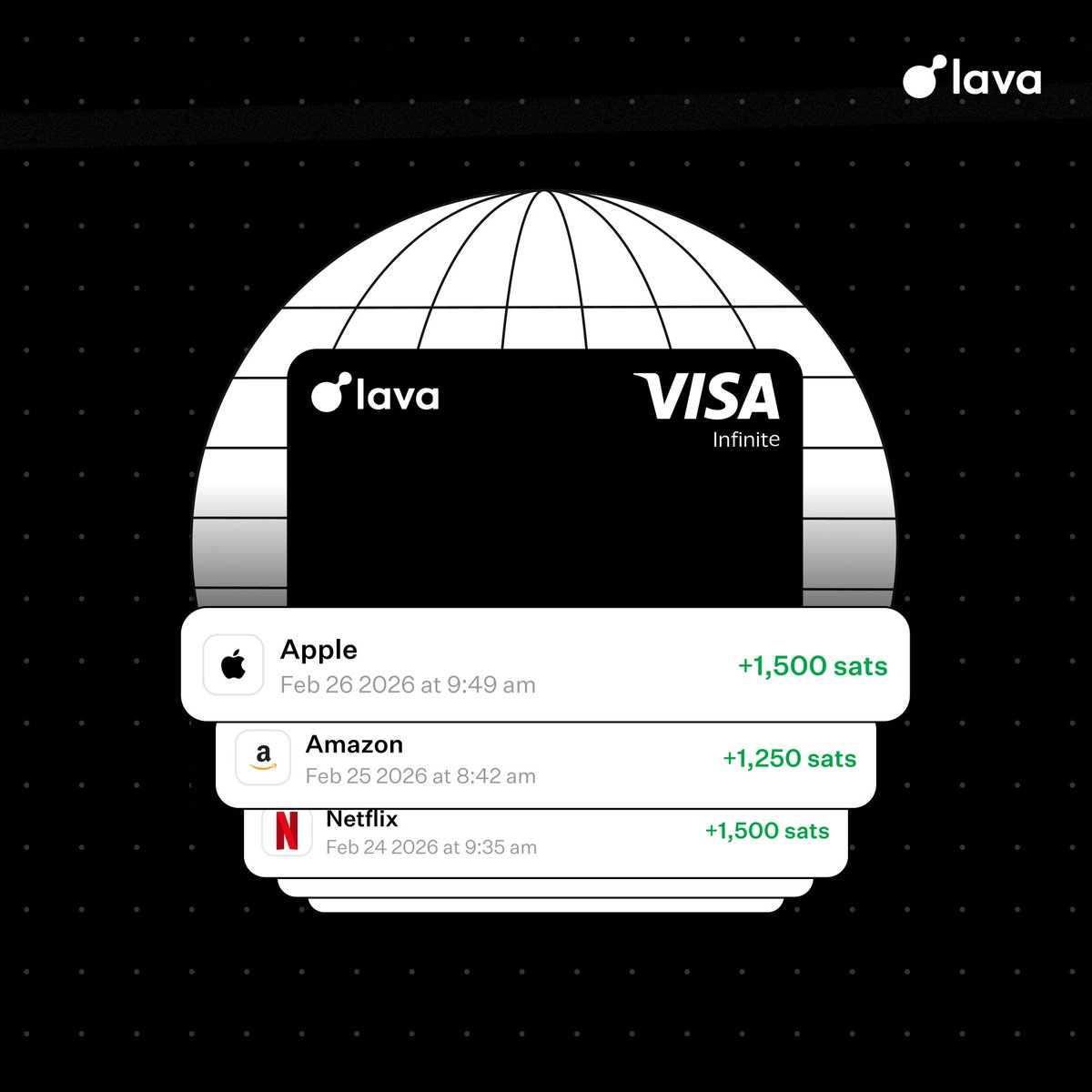

Today we're introducing a new way to earn bitcoin every time you spend.

Lava Card is officially live!

Earn up to 5% back in bitcoin anywhere Visa is accepted, with no annual fee and no FX fees.

Documenting the headwinds I now see for AI.

It won't seem like it, but I love AI and am long-term positive. But when "math doesn't math" I take note.

1. The core thesis for foundation model lab investment has been high upfront investment made worthwhile by significant long-term profits.

2. These are capital intensive businesses and the compute commitments are very high relative to revenue and require strong growth over long time periods. The "leverage" (commitments versus revenue) is extremely high.

3. The fundamentals are not as positive as they previously were:

• Input costs are higher (commodities, chips, power)

• Interest rates are higher

• Competition is more intense

• Scaling Laws are now problematic: exponential costs/power cannot continue

4. Forecasting compute spend is challenging and high risk due to (a) revenue uncertainty and (b) algorithm uncertainty

5. Revenue growth appears to be slowing. The technology is valuable, but ROI is proving to be more expensive and take longer than anticipated.

6. The future is likely "different models for different use cases" with the lower end of the market being highly competitive.

7. Core use cases such as agentic software engineering are likely to need approaches beyond next-token prediction. They are Σ₂ᴾ complexity problems requiring multi-objective optimization and likely a combination of Transformers and other methods.

8. Current forecasts in memory makers are built largely on quadratic attention. That will not persist: we are already seeing work from DeepSeek, Minimax and Nvidia that can cut RAM needs by 80% or more.

9. This means semiconductor valuations are substantially overinflated and will go through the traditional glut versus shortage cycle.

10. For foundation model providers: lower costs with competitive differentiation is good. However, lower costs with a lack of differentiation would mean lower revenues. This makes it harder to (a) service commitments and (b) pay back investors.

11. Leverage is substantially higher than in previous cycles, evidenced by leveraged ETFs, call option activity and margin loans. Korea is particularly susceptible.

12. 0DTE options create a profile that has stronger parallels to portfolio insurance and 1987 than any other point I can remember.

13. The combination of exponential increases in call activity coupled with the ties of semiconductors to structured products means there is a non-trivial systemic risk to the financial system.

14. Implied earnings growth rates are inconsistent with other periods in history.

15. Macroeconomically we cannot and should not fund exponential cost increases. History has shown us repeatedly that there are better ways (see Quick Sort and Simplex).

16. Significant supply is hitting the market via IPOs.

––

Taken together: costs and competition are increasing while revenue growth is likely slowing. Valuations are fragile and prone to technology disruptions that are already here. Systemic financial market risk is extremely high.

the SEC tokenized stock delay has nothing to do with perps. i get the sticker shock of this announcement might be alarming but this isn't bearish for perps and perp related businesses as perps are a derivative and not tokenized equities.

^ it is important to remember that the SEC and CFTC are not the same. perps fall under the CFTC's umbrella not the SECs. ppl will point to this announcement as the reason hyperliquid:native and ethereum:0x232ce3bd40fcd6f80f3d55a522d03f25df784ee2 are down but i think that is more so just a normal market correction for these two assets as they have run hard over the last few weeks despite rates going higher and equities slowing. this SEC announcement will not meaningfully effect hyperliquid or lighter's business in the near term

A breakdown of how our engineers reduced the costs of proving transactions so much that Lighter is the lowest cost product in the market while also being verifiable, from our Fireside with @VitalikButerin

Been diving into Lighter (ethereum:0x232ce3bd40fcd6f80f3d55a522d03f25df784ee2 ). If Ethereum wants to keep perpetuals volume on-chain, this is the killer app it needs.

Here is the thesis on why it works, current metrics, and how it co-exists with Hyperliquid and isn't just a "beta" play:

The Metrics

-Volume: ~$112M daily

-Valuation: ~$345M market cap

-Position: Top 5 DeFi trading volume globally

The Architecture

We need infrastructure that proves Ethereum can handle high-frequency trading. Lighter is an app-specific zk-rollup built for central limit order book (CLOB) trading.

-Execution: Off-chain matching with millisecond latency.

-Settlement: Trustless settlement on Ethereum via zk-SNARKs and blob data.

-Custody: If the sequencer fails, users can reconstruct their accounts and force an exit directly on L1.

Co-existing with Hyperliquid

The derivatives market is large enough for multiple architectures.

-Hyperliquid (Sovereign L1): Optimizes for raw speed and independent consensus. Requires trusting a standalone validator set.

-Lighter (Ethereum L2): Optimizes for Ethereum alignment. Sacrifices sovereign control to inherit Ethereum's security budget.

Hyperliquid proved the demand for fast, on-chain order books. Lighter takes that product-market fit and anchors it to Ethereum. Both models will capture significant volume as traders diversify their counterparty risk profiles.

Cooking something new in the lab - a new approach to RFQ within our fully verifiable onchain order book.

Whales looking to trade RWAs in size - reach out to us at @Lighter_xyz to try the beta.

https://t.co/wzf9ZQbrik

Lighter compresses data by over 300X. This hybrid DA while still being fully verifiable is only possible by being a custom ZK L2 rollup on top of Ethereum.

Source: @l2beat

https://t.co/lZ7PoByCb2

so @l2beat just independently rebuilt Lighter's verifier circuits from source and confirmed they match whas actually deployed on Ethereum -- including the desert verifier.

translation: if Lighter's sequencer ever dies or the team disappears, you can generate a ZK proof on your own laptop and withdraw straight to L1; no permission, no "trust me bro".

pretty much no other perp DEX can say this

@toly do you still think that @Lighter_xyz is CEX?

Lighter's escape hatch just got independently verified: if the sequencer ever dies, you can generate a ZK proof and withdraw directly on Ethereum.

Thanks to @L2beat for the writeup on our fully verifiable and permissionless onchain trading infrastructure.