2025 officially in the books with a 27% YTD gain

we beat $SPX by 10% in the first year of systematic trading/Investing

including the past 3 months of chop/dd

2026 will be about going live with intraday strategies

I hit a trader milestone I thought I'd share for anyone following the journey:

I just went through my first major DD where I almost blew my acct so my psychology was tested and ended up driving home the fact of why I choose systems over discretionary trading EVERY time! to protect my trading.

- from April 22 to June 4 almost everyday we lost money and we gave up all our funded account profits since getting funded in Feb and came within $200 of blowing the acct.

- Plus to make the DD worse than it should've been I had an error last month that made me miss the only good trade of the entire month of May right before the actual DD period started on Topstep

- And lost 40k in funding from Darwinex over the DD

(Paper hands)

This is the first DD period that went this deep so I was stressing about the strats failing and the process of building them being incorrect.... plus having a few friends on twitter now it would be very embarrassing to blow up

Thinking like that then leads to mentally starting to justify editing your system

I was so close to making adjustments this week and I would have only compounded the errors. The lesson is simple... DONT TOUCH ANYTHING. but until you go through it with actual money/consequences on the line you don't understand the challenge

I share this because today we made just about all of it back 😎

this post below explains the mental trigger that starts the bad decisions.

(no @ ing them cuz I dont wanna be an engagement farmer but give her a follow)

@dmartin_trading Exactly and thank you. It looks like tons of traders are going through a similar season rn with these market conditions. It reminds me of one of ur posts a while ago about how good trading goes against human nature and logic

(If Im remembering correctly)

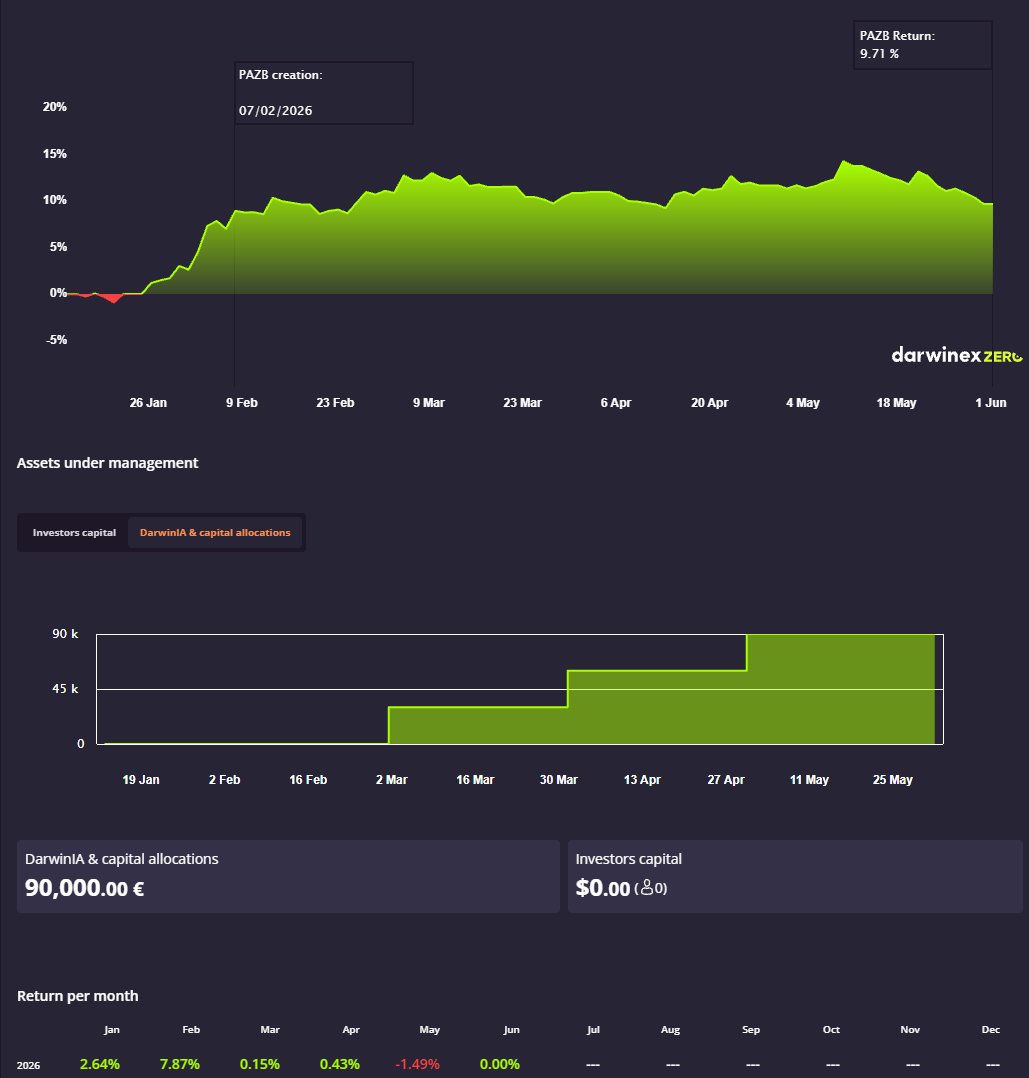

May Trading Recap:

Day Trading: -1.49%📉

IRA Strat: +3.40%📈

Overall: = +1.91%

As you can see, my day trading algos had a very difficult month but I have no reason to believe that the strategies are failing or overfit. The market conditions just did not algin with the conditions my algos need.

The repeatable pattern I noticed is that we would have an impulse out of market opening range and then price would revert to vwap and therefore stop me out.

The part that made it mentally difficult to watch everyday is that we started May with hitting ATH! then slowly gave up profits for 3 weeks straight.

What do I do next?

I'm going to make sure I build a monitoring system for my portfolio that uses industry standard methods / stats to tell me if any of my strats cross the threshold of being a failed strategy that is not live market ready. I don't want that to be a discretionary process. IT will also remove any doubts that creep into your mind during hard times/

OOF May has been tough to watch

Started with a huge win to start the month but ever since its just been small losses just about everyday since

Silver lining is that we need to test the portfolio to see if it holds up to the backtests

Nothing to hide no ego involved just being transparent

NQ Overnight Trading Strategy - 15 year backtest on 5m

The goal here is to catch a piece of the overnight trend so that we can add an additional edge to the portfolio of strategies. You can also expand upon this framework to ride the trend instead of just catching a bite of it. It's a repeatable behavior over time that I find interesting and recommend others should read up on. Here is what I was able to build, hopefully it helps:

The signal I was trying to capture is the documented "upward overnight drift" where a majority of the Indices returns occur from 6pm - 9:30am.

Part of this reason is from big inflows of orders that are pushed by a few daily repeatable factors like the Asian / London Session and Bank/Market Settlements.

The strategy captures this drift, but only on healthy market days.

How OVN Trend works:

1. Time: 18:00-18:15 PM NY OVN session open

2. Entry Conditions: VWAP + Vix + Vol

- Above W VWAP

- 1M VIX < 3M VIX

- Vol Gate = 1 - 1.50 Daily ATR

- Vix Cap = below 75% of past year percentile

3. TP & SL

TP = 0.5%

SL = 0.5%

(passed all parameter sensitivity tests)

3. Position Sizing: Daily ATR

How close is current price to W VWAP?

- Beyond 0.50 ATR = 1 con

- Within 0.25-0.50 = 2 con

- Within 0.25 ATR = 3 con

4. Exit: Time or Price

- Premarket open at 8:30 (can extend to 9:30)

- SL / TP

This strategy is replacing my current overnight strategy BUT FIRST it needs to go into demo forward testing to make sure that its legit. I will let you guys know what the end results are later this year. It was already able to reduce DD while maintaining similar returns on my overall portfolio so fingers crossed this makes it to the lineup. As always I'm no pro and still a beginner myself so feel free to hmu with any tips or feedback. There is so much to learn

#AlgoTrading #DayTrading $NQ

@el_strock yes with 1-3 con position sizing

you are probably looking for the performance if I used % of equity per trade not 1-3 fixed sizing.

beats NQ

@SanjoyRK100 I use tradingview and cme 5m OHLC in python. I don’t have use mt5 but that could be a good addition to verify the strat works across different engines