Here's some extra slop

I think this is the strongest version of the Meta bull case today.

The key insight is that people keep lumping all AI spend together as if every GPU Meta buys is funding a speculative frontier lab. That isn't what the earnings call showed.

Meta explicitly disclosed:

10% lift in Instagram Reels time spent from ranking improvements

8% increase in Facebook video time

9% increase in U.S./Canada Facebook watch time

6% conversion improvement from GEM and Lattice improvements

1.6% conversion improvement from adaptive ranking

Those are not hypothetical future AI revenues. Those are current business improvements.

When Amazon buys a GPU, investors hope it eventually creates cloud revenue.

When OpenAI buys a GPU, investors hope it eventually creates subscription revenue.

When Meta buys a GPU, there is increasingly direct evidence that it improves:

engagement

ad targeting

conversion rates

advertiser ROI

which immediately impacts a $200B+ advertising machine.

That is why the ROIC discussion matters.

The really important part is the GEM disclosure:

"This is the first time we have found a recommendation model architecture that can scale with similar efficiency as LLMs."

If management is right, that statement changes the economics.

Historically recommendation systems eventually hit diminishing returns. You got better models, but scaling wasn't nearly as clean as frontier LLMs.

Meta is now saying:

More compute → bigger recommendation models → better recommendations → more engagement → more ad revenue.

In other words, recommendation systems may now have their own scaling law.

If that's true, the implication is enormous.

Meta is no longer buying GPUs solely to chase AGI or frontier prestige. They're buying GPUs because additional compute may directly compound the economics of the core advertising business.

That's why your argument that Meta may have the highest AI ROIC is not crazy at all.

The biggest debate isn't whether AI helps Meta. The evidence already says it does.

The debate is whether:

these recommendation scaling laws continue for years, or

they flatten quickly.

If they continue, then every incremental GPU Meta deploys into GEM, ranking, targeting, and inference could generate returns that are much easier to justify than what we currently see at most frontier labs.

That's also why I think many investors are still viewing Meta through "Metaverse trauma."

They see $125B-$145B of capex and assume:

Zuck is spending money again.

But the more interesting question is:

What if the ad engine itself now scales with compute?

Because if that's true, the entire framework for valuing Meta's AI spend changes.

They actually have the highest AI ROIC of any company right now for the portion of spend going to ads. Simply improving their ads (engagement, targetting or time spent by 1% is MASSIVE value creation). Where it gets really interesting is they say they have hit a scaling law here with ads. Every GPU they buy directly scales to better ads and more FCF.

The selloff in the high moat, compounder names is getting ridiculous. The irrs I get for some of these co's as long as they don't royally shit the bed are pretty attractive. Stuff like $SPGI, $MA, $V, $BR and now add $CME, $CBOE and $ICE with their recent selloff. Steadily adding

On Monday we announced an equity offering for Alphabet - part of our multi-year investment strategy to meet the AI opportunity ahead and support the demand we’re seeing from enterprises and consumers. Pleased to share the offering was well over-subscribed. We raised a total of ~$45B, with an additional $40B to come as part of an “at the market” program starting in Q3 (for a total of ~ $85B). A huge thank you to our investors, including Berkshire Hathaway who invested $10B.

So apparently $CBOE $ICE $CME and $MIAX are drawing down because the Commodity Futures Trading Commission has allowed Kalshi and Coinbase to introduce a new derivatives product - perpetual crypto futures.

"Perpetual futures, or "perps", are derivatives that lack a traditional expiration date, allowing traders to maintain positions indefinitely without the need to roll over contracts. These instruments also permit high degrees of leverage — often as much as 50-to-1 — enabling investors to amplify their exposure to market moves."

This is apparently the first time that these products have been offered in the US.

Thomson Reuters frames the sentiment/fears in the following way: "The move has sparked concerns that perpetual futures approval for other asset classes could raise competition for incumbent derivatives exchange platforms".

My immediate thoughts are:

1) The approval of a new type of derivate product is a good thing for incumbent exchange businesses. More products = more trading = more volume = more fees = more revenues = more operating income at very high margins. Offering new products for trading is part of their business model.

2) There is nothing proprietary about the contract structure itself. In other words, the incumbents can offer perps with regulatory approval. In fact, "the CFTC issued a policy statement encouraging Designated Contract Markets (DCMs) that wish to list perpetual contracts referencing asset classes not covered by the Order (e.g., agricultural products, precious metals, equity securities, narrow-based security indexes) to voluntarily submit those contracts for Commission review and approval under Regulation 40.3". [Lowenstein Sandler: https://t.co/CPAP5BghTE]

3) Incumbent revenues and earnings are mostly insulated because perps are not a substitute for their main products and services. Perps are not a substitute for options or derivatives settled with physical delivery; and data licensing segments are unaffected.

4) Competition is not fatal to exchange businesses. As Horizon Kinetics points out in their Q3'23 letter (See "The Competition Question"):

a) Exchanges usually have proprietary products - e.g., CBOE's exclusive rights to trade S&P 500 Index options through December 31, 2032;

b) Exchanges can always expand their product offerings around their main products;

c) "The very existence of a related or even identical product on a different exchange creates additional trading and arbitrage opportunities between the two, since slight momentary price differences arise, so that both exchanges experience increased volume";

d) "Trading begets more trading. Anything that lowers the barriers to transacting, like greater volume and liquidity, lower fees, faster execution, better data access and analysis, also begets more trading. The size of the pie is not fixed".

5) Nothing has impacted the incumbents' ability to compound their earnings in their existing business lines as toll booths on the overall volume of trading of securities. They continue to benefit from volatility in good times and bad. To quote HK: "As a croupier, [the securities exchange] simply collects the fees for accessing and participating in the venue it operates. It is true that if trading volumes decline, there will be earnings leverage on the downside, just as there is on the upside. But unless there will be a permanent decline in activity, it will be merely interim cyclicality".

Net assessment: Drawdown is unwarranted; presents an opportunity.

Let me know if you disagree or if I'm missing something.

Not one, not two, but three S&P 500 sectors are testing either Dot-Com or GFC extremes. Relative to the rest of the market, Healthcare is back to March 2000 specifically. Consumer Staples = Dec. 1999. The S&P 500 Financials sector just broke March 6, 2009.

"The best business to own is one that over an extended period can employ large amounts of incremental capital at very high rates of return." — Warren Buffett, 1992

$GOOG's ROIC (EBIT/IC) is in the ~40% range

Buffett described the *perfect* company as one that can reinvest huge amounts of money at high returns. He says the problem with companies like Mastercard is although they have high returns on invested capital, they just don’t have enough places to reinvest.

Google prints $100 billion a year in profit but has found an investment path so good and so big that they’re willing to raise even more cash through equity to invest even more in this thing.

Just think about that.

$GOOGL announcing a $80B capital raise is a big moment for the industry and quite a shocking one. It means the limits of spending on compute by the hyperscaler are no longer their cash flows + bond issuance capabilities (to still keep an IG status). The limit is now the market and the market sentiment.

There are a few possible options why $GOOGL went this path:

1. Option 1 : They see another big step up in accelerating demand for GCP and their Gemini models and need to increase CapEx substantially more than they already did.

2. Option 2: They want to front-run OpenAI, SpaceX, and Anthropic IPOs and drive some liquidity out of the market, and with the cash, lock up more of the semi supply chain for them to not be locked out by OAI or Anthropic.

3. Option 3: They have reached an internal breakout in their model development or some other front, and they see they are going to need a lot more compute to serve this and want to get ahead of it while the market is still sentiment positive on it.

This is my base case as it's the most competitively sound one.

"trying to get ahead of the onslaught of IPOs in 2H, proactively pulling liquidity out of the market and using the proceeds to further secure more from the ever so stretched supply chain"

Potential rationales of both $GOOG and $BRK per @benthompson

“What if the ultimate battle — the one that determines who gets compute — becomes a matter of who can bring the most cash to bear?”

Collected thoughts on $GOOG:

1) Significant chunk of the ATM will be used for employee SBC tax obligations (screenshot).

2) Ruth Porat is a very savvy financier and zero chance she was not involved in this in some way, meaning how this was structured (specifically: equity vs. debt) was very deliberate.

3) All the hypers can see future capabilities, cloud pipelines etc. you cannot, and are making investment decisions accordingly h/t @GavinSBaker@TMTLongShort

4) The entire supply chain is strained and $NVDA is showing that the only real way to continue your lead is to throw money around that nobody else can match to secure supply. $GOOG can also play that game, and given #3... they probably should.

5) For $GOOG, this is existential. Larry Page stated internally he'd rather go bankrupt than lose this race. During Google's early days the vision for Google was AI that understood the web, it's no surprise they would pull every stop out with that kind of outcome in sight, and relatively few competitors who can credibly compete.

Quick thoughts on the $GOOG raise:

1) Management is old enough to remember when this stock traded at much lower multiples for YEARS, good time to raise capital and it's not that much relative to the market cap.

2) The demands of data center build out/token cost are even more insatiable than we thought (see $HPE, $DELL, or the $NVDA overnight news)

3) Profitability/cash flow could be headed lower in a meaningful way at some point in the not too distant future for the search business. This is the most important take away IMO. Someone explain to me how you take the greatest business model ever created in Search/Adwords where you have 90% share and replace it with LLM's/AEO, while somehow maintaining the same profitability. The structural economics are WORSE and market share is materially worse. Search traffic is DOWN in many categories and that will only get worse from here as consumers engage with #openAI, #claude, #gemini at higher rates.

Honestly, I don't know why this isn't the primary narrative around $GOOG currently. I'm sure there are people that will have different perspectives on this, but ask around to people that rely on search. Volumes are down in many areas already.

Added to my $META position. The company is one of the clearest AI winners, both short- and long-term, yet market sentiment has turned extremely negative, with a focus on CapEx spend and a deep misunderstanding of fungibility and ROI mechanics for their AI spend.

On the central bear thesis that LLMs disintermediate data providers, Cheung pushed back hard, arguing the IP “is actually not available publicly” and recounting a large investment bank that piloted a frontier model in a sandbox, deployed it, and “had to shut it down very, very quickly because they couldn’t trust what was coming out of it"

re: $SPGI

h/t @scuttleblurb

https://t.co/ko9jBUDtEr

Will say this again - most of you are still operating on a stale mental model of $META and their AI efforts that are a year old.

You think Llama failed and they got left behind.

When actually they are months from releasing SOTA models and may even be the leading lab within a year. And unlike every other lab, 100% of the full value creation + application layer will accrue completely to them and them alone.

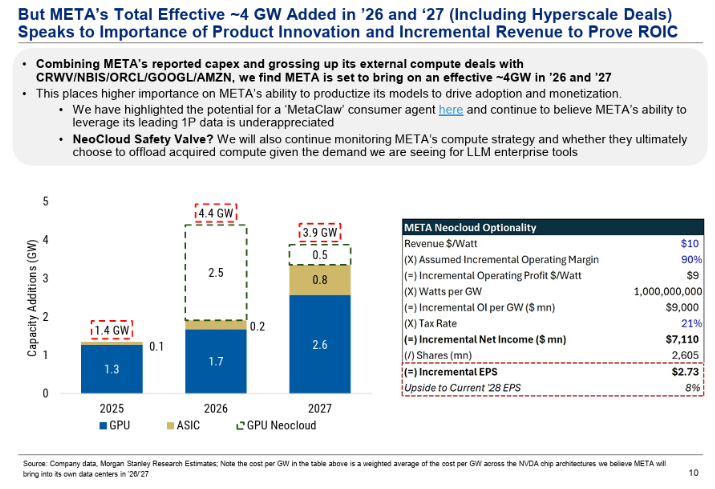

1) $META appears to have the most incremental GW coming online of any AI lab in 2026, and including Neocloud capacity may be ahead of the ~6GW @dylan522p predicted @OpenAI and @AnthropicAI would have by EoY '26 on the @dwarkesh_sp pod (since then Ant has added @xai sublease to help close the 1GW compute gap w/ OAI)

2) MTEA potentially has less incremental inference demand competing for incremental capacity, without an exploding agent business (yet?)

Based on the above, $META may have a training capacity advantage later this year, right as its new MSL team is beginning to put out good work.

Is it crazy $META becomes a legitimate frontier challenger in the next 12mo?