XVS from @extendedapp is really underrated.

I don't see anyone talking about it. They print 11%+ APR without ANY red candle in the same time.

In the same time I see volumes levels on the exchange from pre-oct 25'. It means that getting points was not as easy as it is now since a long time.

If you have some spare time, even in those conditions it's worth to have a look, try to get those cheap points on Extended now and then just wait for TGE.

Don't let them farm cheap. I was silent about farming, when it was overfarmed, but now again Extended seems REALLY underfarmed.

The best code, with the biggest boost as always: https://t.co/e7smwvyG9M

6 months of building. what's next?

TLDR: We focused on putting in place the product, partnership and governance foundations for the next phase of Extended. TradFi partnership, hundreds of new crypto and RWA markets, spot trading and further decentralisation are coming. Our approach to growth remains unchanged: no KOL round, no paid promotions, no paid PR, no podcast sponsorships and no paid market-making arrangements.

Over the past 6 months, the team at @extendedapp has been focused on a fairly simple objective: building the product, infrastructure and partnerships required to support the next stage of growth.

A lot of the work happened behind the scenes but we are now getting to the point where the pieces are starting to come together.

Product

Some of the key items are already live:

- Multi-asset collateral, allowing users to post wBTC, ETH and USDT alongside USDC. Besides expanding the collateral universe, it also unlocks simple cash-and-carry strategies directly on the platform.

- Full email onboarding, including gasless deposits and withdrawals. While not particularly exciting on its own, it unlocks fiat on/off-ramp integrations that are required to onboard non-native users.

- Significant improvements to UI stability, responsiveness and overall user experience, driven largely by user feedback collected over the past months.

Several important pieces are coming next:

- Spot trading, which we view as a table-stakes component of a complete exchange experience and an important UX improvement to multi-asset collateral.

- Opening up our lending infrastructure beyond the exchange itself, allowing users to deposit wBTC, ETH and USDT, borrow USDC and deploy capital elsewhere.

- New trading infrastructure that will unlock hundreds of additional crypto and RWA markets. Internally, this is the product initiative we are most excited about.

Growth

Over the same period, we have spent a lot of time thinking about how Extended should grow.

One principle remains unchanged: we do not pay for KOL promotions, PR, podcast sponsorships or market-making arrangements. This applies equally to cash, tokens and points.

Its a slower path and not the easiest one but over time we have become increasingly convinced that sustainable growth is built on product quality, distribution and community rather than financial incentives.

We have also completed a number of less visible but equally important initiatives:

- Finalised the legal and commercial framework for our first tradfi partnership, which unlocks some of the product initiatives mentioned above and establishes a foundation for future institutional integrations.

- Secured the majority of the long-term partners who will help operate, secure and govern Extended. We are proud of the quality of the organisations that chose to support the vision and will be sharing more details separately.

- Spent considerable time with our largest users and major ecosystem participants to gather feedback and ensure alignment around the long-term direction of the protocol.

- Remained committed to our original targets for early community rewards, despite certain things taking longer than anticipated.

This month is an important one for Extended. It will conclude the team's efforts over the past 6 months and mark the beginning of the next phase: further decentralisation, ecosystem expansion and the transition to a community-owned protocol.

RWA Oracle Infrastructure Update: Building the foundation for a broader universe of assets

Starting May 25, we will begin migrating select RWA markets to a native oracle implementation powered by RedStone.

This migration is an important step towards expanding the range of RWA assets supported on Extended.

Over the past 1.5 months, some of our RWA markets, including indices, energy, industrial metals, and precious metals, have relied on Trade xyz pricing infrastructure. To ensure continuity for traders, the new implementation closely follows the pricing methodology established by Trade xyz and broadly adopted across the industry:

- Indices: Futures-implied spot price based on cost of carry (SOFR minus dividend yield), using the same roll schedules as Trade xyz

- Energy and industrial metals: Futures-based pricing using the same roll schedules as Trade xyz

- FX and precious metals: Spot pricing

Migration schedule:

- May 25: Precious Metals (XAU, XAG, XPT) and FX (EURUSD, USDJPY)

- May 28: Industrial Metals (XCU)

- June 1: Indices (SPX, NDX)

- June 10: Energy (WTI, NATGAS, XBR)

Updated documentation includes details on market-specific price references, oracle availability windows, and equity index and energy roll schedules: https://t.co/IGK5bfoMQj

@CallumOnCrypto@extendedapp@variational_io I remember you sharing when extended just started their points program 1 year ago. Thanks buddy for sharing it I hope it goes like hype🔥

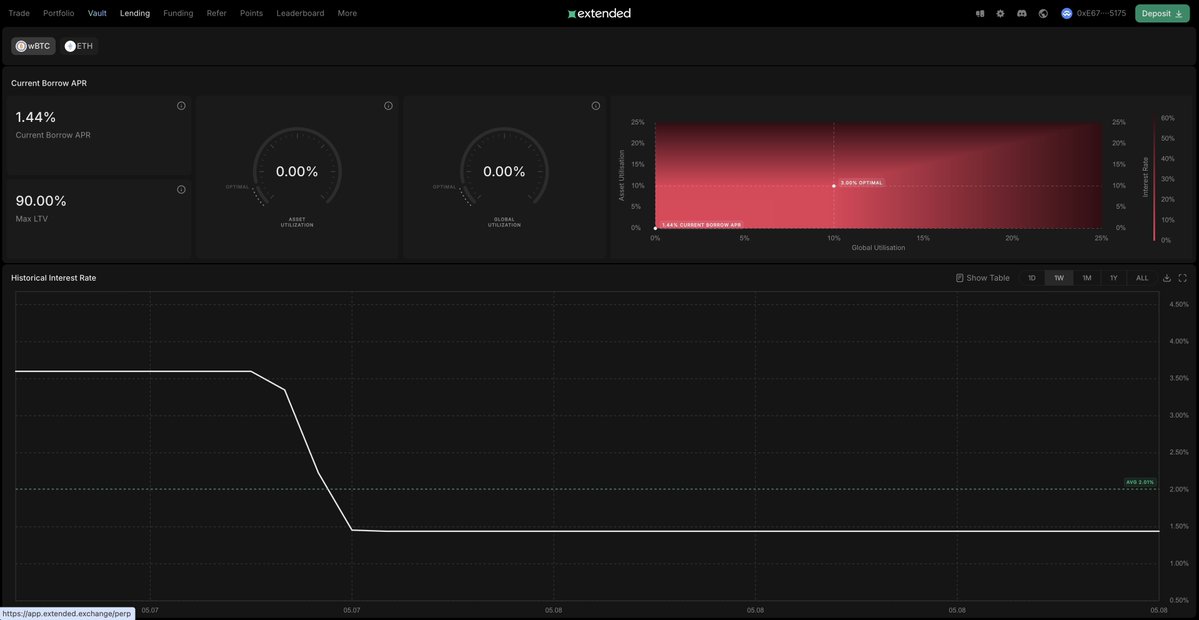

Multi-Asset Collateral is now live on Extended

From today, wBTC and ETH are accepted as collateral alongside USDC and XVS (Extended yield-bearing collateral). EURC and USDT are coming soon.

How it works

The system operates on a native money market, with the vault acting as the primary lender. When trading losses push your USDC balance negative and that deficit is covered by non-stablecoin collateral, you are borrowing USDC.

Borrowing rates depend on two factors: overall vault utilisation and utilisation against each specific collateral asset. For example, if demand to borrow USDC against ETH is lower than against BTC, borrowing against ETH will be cheaper.

When a user holds multiple collateral assets, borrowing is automatically allocated starting with the lowest-rate asset and moving upward, minimising the effective cost with no manual input required. We are not aware of this being implemented anywhere else in DeFi.

Example. User is down $175K on a perp and borrowing $175K USDC against a mixed book:

$50K USDT @ 1% - $500

$50K ETH @ 5% - $2,500

$75K BTC @ 10% - $7,500

Total annualised interest: $10,500. Effective rate: ~6%. Borrowing the same amount entirely against BTC would cost $17,500 annually, or 67% more.

What this means for Extended Vault

The vault is the primary lender for the entire system. All interest paid by USDC borrowers flows to vault depositors as Extra Yield, on top of the trading fees already distributed.

This creates a second, structurally independent yield stream for XVS holders. The vault earns by serving as the backbone of the margin system.

What's unique about Extended’s native money market.

With multi-asset collateral now live, @extendedapp users can deposit ETH and wBTC (with USDT and EURC coming shortly) and use them as margin to trade perpetuals. When a user's USDC balance goes negative, borrowing is triggered automatically with the Extended Vault serving as the primary lender.

The key difference is how borrowing rates work.

Traditional crypto money markets typically operate through isolated lending pools, where interest rates depend only on utilisation of a specific pool. Collateral risk is managed separately through haircuts and borrowing limits.

Extended's setup is fundamentally different.

The Vault lends against multiple collateral assets simultaneously, while borrowing demand emerges dynamically from unrealised PnL. In this environment static global borrowing caps are not practical.

As a result borrowing rates depend on two dimensions:

- overall vault utilisation

- utilisation against a specific collateral asset.

This means borrowing USDC against ETH can be cheaper than borrowing against BTC if system-wide exposure to ETH is lower.

The second layer is how borrowing is allocated.

When a user has multiple collateral assets, the system automatically routes borrowing through the lowest-rate collateral first, minimising the effective cost of capital.

Example: if a user has a negative USDC balance backed by both ETH and wBTC collateral, and ETH borrow rates are lower than BTC, the system will allocate borrowing against ETH first before routing the remainder against BTC, continuously reducing the effective cost of capital.

The result is a system where:

- users automatically receive the cheapest borrowing allocation across their collateral portfolio

- Extended maintains granular risk control over exposure to different collateral assets backing borrowed USDC

- vault depositors earn additional yield directly from trading activity.

From our conversations with TradFi brokers, it’s clear that moving to 24/7 is quickly becoming table stakes.

To get there, most are looking at two routes: launching perps (either in-house or via partners) or extending CFDs to 24/7 and hedging the exposure externally.

When discussing the second approach, hedging CFD exposure with perps (instead of futures, leveraged spot, etc.), two structural differences stand out:

1. Deterministic liquidation vs operational margining. In TradFi, margining is rule-based but involves operational processes and potential grace periods, while in perps liquidation is fully deterministic and continuous, ensuring individual account and system-wide solvency without credit assumptions.

2. Managing funding vs rollover / borrow costs. Perp funding is realized more frequently (hourly / 8-hour), and can be significantly more volatile as it reacts in real time to positioning imbalances, compared to the smoother, benchmark-driven cost of carry in futures and financing markets.

None of those are blockers to a wider institutional adoption of perps, but rather observations on how traditional players are already adapting their ways of working to benefit from perps and DeFi.

In light of recent security incidents and the increasingly hostile environment, we have activated a dedicated treasury contract to further strengthen the system’s resilience. This contract is solely responsible for holding the entirety of the protocol’s treasury (TVL) and incorporates a circuit breaker mechanism governing fund outflows.

Specifically, if the total value locked (TVL) decreases by more than 3% within any rolling 24-hour period, the treasury contract will automatically halt all USDC outflows. In such an event, settlements are paused until the team reviews the underlying transactions and explicitly approves any increase in withdrawal limits via a multisignature process. The multisig signers are distributed across multiple geographies.

In rare circumstances, this may introduce delays to withdrawals. However, we believe this is a reasonable trade-off to ensure the safety of funds.

The perpetuals and vault contracts, which handle trading and business logic, no longer custody funds. All asset movements are routed exclusively through the treasury contract.

As a result, even in the event of a full system compromise, including bridges, oracle providers, or operator infrastructure, the maximum potential impact is limited to 3% of the TVL.

I looked at 6,000+ traders who joined Extended with under $100k in volume in their first month to see where they are six months later. Here's what separates the ones who scaled from the ones who didn't.

Traders who scaled into a higher volume tier by month 6:

- Started at a median of $20k in monthly volume. By month 6 they were doing $273k. That's a 12x increase

- Trades per month went from 29 to 251. Nearly 9x more active

- Asset mix shifted from 62% majors (BTC, ETH, SOL) and 38% alts in month 1, to 79% majors and 21% alts by month 6

The rest, those who continued using Extended but didn't grow, tell the opposite story:

- Median volume for them fell from $21k to $9k. They were trading less, not more

- Trades dropped from 44 to 17 per month

- Asset mix barely moved - if anything, they drifted slightly more into alts over time

Two things stand out:

1. The traders who scale don't just trade more - they trade differently. The rotation into majors is consistent and significant. As conviction builds, exposure concentrates.

2. And frequency is the leading indicator. Scalers nearly 9x their trade count. The others cut theirs by more than half. The divergence shows up in behavior before it shows up in size.

Volume follows conviction. And conviction shows up in how often you trade and what you trade - long before the size catches up.

just ran the stats - 57% of Extended traders aren't using XVS as collateral (Extended yield-bearing asset).

i've explained the benefits before in the quoted tweet and tweets earlier. TLDR: it's free money on top of your existing trading setup.

my guess is that traders assume it's complicated or requires a different strategy. it's not. here's exactly how to start in 60 seconds:

Step 1: deposit USDC to the Extended Vault: https://t.co/ExHpImfITo

when you deposit, you receive XVS (Extended Vault Shares). these automatically act as collateral for your trades. one thing to watch - in the deposit popup, make sure you select the sub-account you actively trade from. if you pick a separate sub-account, XVS won't be used as collateral.

Step 2: there is no step 2.

from this point you just trade normally. XVS is used as collateral automatically. vault yield gets added to your collateral daily, compounding your margin without you doing anything.

that's it. same strategy, same trades, same risk management - except your collateral now earns 7% APR.

if you're not doing this you're leaving money on the table every single day.

@lttlanna Yeah, need to get more attention towards it maybe some announcement would be helpful to spread awareness or cross asset collateral announcement which would make it unique and more eye catching.

State of liquidity and execution on @extendedapp v5 - TradFi Edition

By popular demand, we're taking our liquidity analysis beyond crypto for the first time, this time covering TradFi markets: US equities (NVDA, MSTR, INTC, CRCL), precious metals (XAU, XAG), and the Nasdaq Index (NDX), across @extendedapp, @HyperliquidX (via @tradexyz), and @Lighter_xyz.

Methodology

1. We measured slippage (buy/sell) on the above assets for $10k and $100k market orders across the three exchanges every 30 seconds from Mar 24, 07:11 UTC to Mar 31, 11:44 UTC (20,657 snapshots)

2. We ranked each exchange by market and clip size for both slippage and total cost of execution (slippage + exchange fee), where 1 = best and 3 = worst

3. Fees applied: Extended 2.5 bps, Hyperliquid base rate 4.5 bps, Lighter 0 bps

4. The dataset also includes charts showing how slippage evolved over the tracked period

5. NDX is listed as XYZ100 on Hyperliquid and QQQ on Lighter

Results:

Slippage

- On equities and metals, Extended leads at $10k clip sizes, while Hyperliquid is better at $100k

- On indices (NDX), Hyperliquid leads at both clip sizes

Total cost of execution - where it gets interesting

- Equities at $10k: Extended is the cheapest across all 4

- Equities at $100k: Hyperliquid leads across all 4

- Metals: Lighter's zero-fee model gives it the edge on both XAU and XAG at $10k, and on XAU at $100k

- Indices (NDX): Hyperliquid leads at both clip sizes

What this means

1. For equity trading at smaller sizes, Extended liquidity and fee structure make it the most efficient option overall

2. For larger orders, Hyperliquid has deeper liquidity and wins on total cost

3. Lighter's zero-fee model gives it a real edge in metals, though less so in equities

It’s still early days for on-chain TradFi liquidity. There’s room for all exchanges to improve, and we'll keep tracking it.

Full dataset: https://t.co/TlnzLIfXPt

One of the reasons traders choose Extended over other perp DEXs - and this isnt just us saying it, its something we hear directly from users - is that the team is genuinely responsive.

And I think that says a lot.

You can see it in how quickly tickets get handled, how active our team is on Discord, how feedback gets noticed, and even in how our CEO Ruslan replies to users’ suggestions himself.

Its great to see that the community actually notices and appreciates that.

It changes how people experience the platform, because it feels like there are real people behind it who care, listen, and want to keep improving.

Even if we don’t reply to every single message publicly, that doesnt mean its ignored.

A lot of what gets shared with us is seen, discussed internally, and helps shape how Extended evolves.

Thats also why we genuinely enjoy meeting traders and community members face to face.

From Singapore to Poland to Hong Kong - and through many 1:1 conversations along the way - spending time with people in person has always been important to us.

A lot of the best conversations happen that way.

So where should Extended go next?

Quick update on what’s happening at @extendedapp and the key information :

- The next major update, unified margin, will allow wBTC, wETH, and EURC to be used as collateral, along with a lending/borrowing market.

More details on the mechanism from the CEO here : https://t.co/pt0Zgccsvg

-Unified margin is currently on testnet, with the team targeting early April for the mainnet launch.

-Season 2 is planned after the unified margin launch. It’s confirmed that there will be a reduction in the number of points distributed each week (no specific figures mentioned).

-Partnership with [eToro] , it’s mainly a matter of paperwork so the process is quite lengthy. The team is doing its best by responding as quickly as possible to [eToro]’s requests, and they are already at a fairly advanced stage.

-Treasury: Around $10M for now, which will be used for buybacks at TGE.

-TGE : Planned after the Spot market launch. It will likely be slightly after H1, depending on the rollout of the different products planned by Extended (i.e. Spot and a potential announcement👀).

Expecting more.

![0xMaus's tweet photo. Quick update on what’s happening at @extendedapp and the key information :

- The next major update, unified margin, will allow wBTC, wETH, and EURC to be used as collateral, along with a lending/borrowing market.

More details on the mechanism from the CEO here : https://t.co/pt0Zgccsvg

-Unified margin is currently on testnet, with the team targeting early April for the mainnet launch.

-Season 2 is planned after the unified margin launch. It’s confirmed that there will be a reduction in the number of points distributed each week (no specific figures mentioned).

-Partnership with [eToro] , it’s mainly a matter of paperwork so the process is quite lengthy. The team is doing its best by responding as quickly as possible to [eToro]’s requests, and they are already at a fairly advanced stage.

-Treasury: Around $10M for now, which will be used for buybacks at TGE.

-TGE : Planned after the Spot market launch. It will likely be slightly after H1, depending on the rollout of the different products planned by Extended (i.e. Spot and a potential announcement👀).

Expecting more.](https://pbs.twimg.com/media/HD4k0uiXcAAUFu1.jpg)