Deep Tech & Growth Investor | Exploring small caps and asymmetric setups.

Sharing my deep dives & fundamental research on $QS, $RDDT, $ASTS, $NBIS, $NVTS, $RBRK

You are not bullish enough on $QS.

⚡ The technology is real

844 Wh/L energy density. 12-minute fast charge (10–80%). 1,000+ cycles, less than 5% degradation. Anode-free lithium-metal with a ceramic separator thinner than a human hair.

🔋 The graphite problem nobody prices in

Every lithium-ion battery needs graphite. Over 90% of global supply comes from China.

$QS is anode-free. Zero graphite. Zero China dependency.

In a world of tariffs, supply chain decoupling, and energy sovereignty — it's a structural moat almost no analyst is modeling.

🤝 The commercial ecosystem is being assembled

Automotive:

• Volkswagen / PowerCo — Collaboration Agreement + $130M conditional royalty prepayment, up to 80 GWh licensed capacity

• Hyundai — JDA signed

• Honda — JDA signed

• Mystery North American OEM — JDA signed December 2025 👀

My hypothesis on the mystery OEM: Ford or Tesla.

→ Ford: Solid Power JDA expired Dec 31, 2025. ~$18B in conventional battery contracts cancelled. Timing is surgical.

→ Tesla: Maxwell Technologies acquisition history. CEO publicly commenting on anode-free patents. Not eliminated.

Both fit. I'm watching both.

Beyond automotive:

• Fluence ($FLNC, Siemens/AES JV) — multi-year stationary storage agreement (grid, data centers, solar)

Manufacturing supply chain:

• Murata — JDA signed October 2025 for ceramic separator industrialization. What most miss: Murata isn't just a supplier — they develop their own solid-state batteries. This is two SSB players aligning on a shared technology stack.

Corning isn't just helping $QS scale ceramic separator production. They have developed their own proprietary "Ribbon Ceramics" manufacturing process — a high-speed, high-precision ceramic forming technology that positions them not only as a supplier, but as a future seller of solid-state battery components at scale.

Corning's Program Director of Energy Materials put it plainly:

"Regardless of the chemistry, the technology gives us a winning advantage."

They're not betting on $QS out of charity. They're betting because their own commercial roadmap depends on solid-state batteries becoming real — and they've chosen $QS as the partner to make that happen.

• Digatron — Eagle Line production equipment

This is not a startup with a deck. This is an ecosystem being assembled in plain sight.

🏭 Eagle Line is operational

First commercial-scale solid-state production line — inaugurated, running for months. The lab-to-factory transition is underway.

🏍️ Real-world proof point incoming

Ducati V21L — field testing live in 2026.

I'm personally watching two events:

→ World Ducati Week: July 2026

→ IAA Munich: September 2026

First public validation on a real vehicle. It's happening this year.

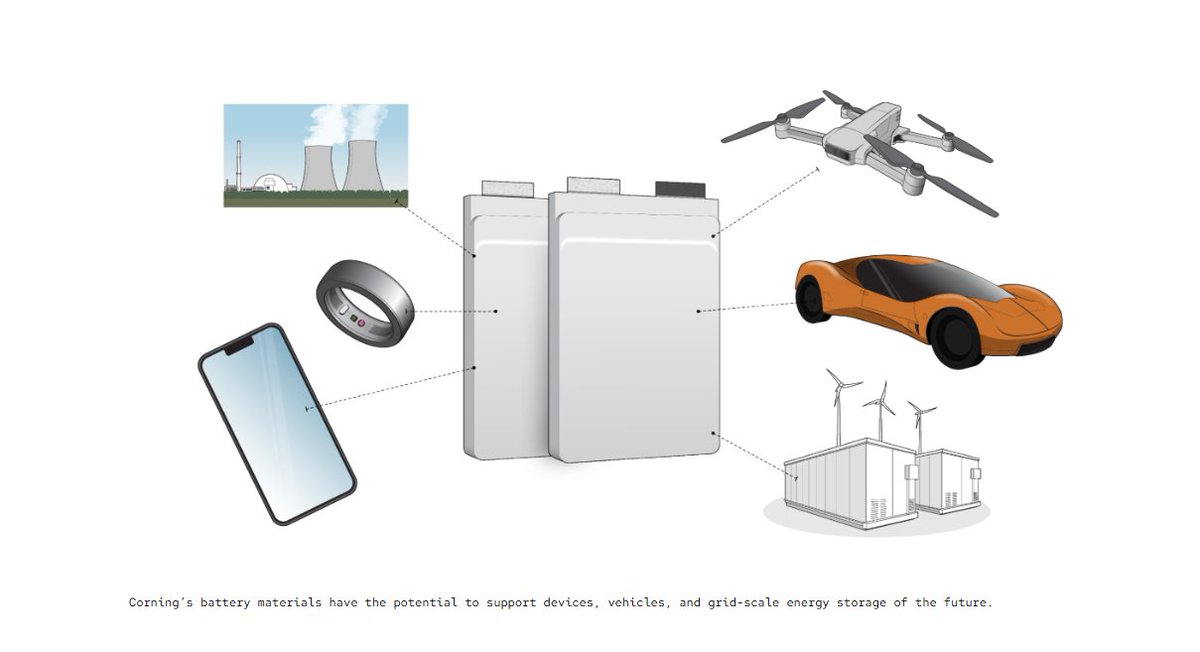

🚀 Beyond EVs — and I'm genuinely excited about this

The non-automotive pipeline is barely discussed. I believe 2026 will change that.

$QS has officially listed its target commercial applications:

→ Nuclear

→ Drones & defense

→ Electric vehicles

→ Wind energy storage

→ Smartphones

→ Smartwatches

Stationary storage & data centers: $QS already has the Fluence agreement in place. First-mover position in an infrastructure segment exploding with AI-driven demand. More news coming.

Drones & defense: No graphite = no China supply chain = full domestic production potential. The latest drone footage is not just a demo — it's a signal.

And this week $QS announced Dr. Mark Maybury to its Strategic Advisory Board.

Dr. Maybury is currently VP of Commercialization, Engineering & Technology at Lockheed Martin — leading the transition of cutting-edge research into scalable products for commercial and defense applications. He previously served as Chief Scientist of the U.S. Air Force (2010–2013), and as CTO at Stanley Black & Decker.

His own words:

"I see tremendous opportunity for QuantumScape to redefine energy storage across multiple sectors, including defense, where reliable, high-performance batteries are mission critical."

Consumer electronics: Density + safety at scale.

$QS is not priced for any of this.

The non-automotive TAM is real. The agreements are being signed. The people are joining. The announcements are coming.

You can't expect a 10x without stomaching 50–80% drawdowns.

Check your thesis. If it's still intact — and mine is — tune out the noise and trust management to execute.

The shorts won't win forever.

Thank you for reading.

@jean89601631 Honnêtement je ne sais pas mais je pense que les institutionnels et le marché pense que $QS a un potentiel et qu’il est plus important que c’est concurrent mais certain personne n’y croît pas et sont short.

$QS

Shahar Noy (General Manager & VP Data Center) is executing his first official mission right now (June 3-4) at the highly exclusive Bloomberg Tech Innovators Circle, surrounded by top-tier tech decision-makers.

This isn't a coincidence. It's a showcase. QuantumScape is proving they are going after the critical Data Center and AI market, expanding far beyond EVs.

@Defiantclient2 I don't really see how it could be otherwise. The same people who mock us because they see 0 revenue on earnings will buy when we reach 80

@cyberprince_rwo Given that new markets are a goal this year, we should normally have defense contracts with an $LMT investment. However, I think we could have both, along with datacenter contracts.

Been following this stock closely for a few days now. Discovered it thanks to the excellent analysis by @ThematicTrader. If you're looking for more info to dig deeper, I know @ren_aramb and @CKCapitalxx cover the name, and I know my friend @tournonskiwi is also positioned.

I am long $ADTN. I initiated a position at $17.3. At ~1.4× 2026E EV/Revenue ($1.5B market cap), it is massively undervalued. Wall Street still prices it as a plain FTTH vendor, severely discounting its Optical Networking division (+24% YoY in Q1) relative to pure-play photonics peers. There are three compounding drivers that will reprice this stock, with the core thesis centered on AI Data Center infrastructure.

This AI infrastructure shift is the ultimate driver here, because the real AI scaling wall isn't compute — it's power budget. In a 10,000-GPU cluster with 8-16 ports per node at 800G, a standard DSP-based transceiver burns 10-15W per port. The delta runs into tens of megawatts at AI datacenter scale, which acts as today's binding constraint and pushes operators into severe power and thermal limits. Adtran's answer is LiteWave800, launched March 10 and showcased at OFC 2026 in Los Angeles. It's an OSFP 800G DR8 LPO module for short-reach intra-datacenter links up to 500m. Its specifications are in a different class: 1 pJ/bit, ~0.8W total power consumption — 12-18× more efficient than DSP-based 800G, and 6-10× better than gen-1 LPOs. This edge comes from full vertical ownership, combining an in-house IC team inherited from ADVA and single-mode 1310nm VCSEL partners to optimize at the module level holistically where discrete component designs fail.

This is far from a one-off product, fitting into a complete AI infrastructure vertical that features coherent pluggables 100/400/800G, plug-and-play DCI up to 1.6T, automated open line systems, and quantum-safe transport via the FSP 3000 co-developed with euNetworks as "Quantum Shield". The industry signal is unambiguous as giants like Broadcom, Marvell, and NVIDIA evaluate LPO as an alternative to DSP for their 800G and 1.6T AI fabrics. Adtran is already there with a shipping product, not a roadmap. Meanwhile, a peer like Ciena has run up nearly 200% in a year riding the exact same optical narrative, trading at a vastly higher multiple on ~$6B in revenue. ADTN at $1.5B while targeting the highest-growth segment in AI is a complete mispricing.

The second catalyst, supporting this foundational momentum, is the BEAD program, backed by $42.5 billion in federal funding for rural US fiber deployment. First purchase orders have already been received for Delaware, Louisiana, and Nevada. Management expects a meaningful revenue contribution starting in H2 2026, with peak deployment in 2027, unlocking an estimated TAM of ~$1B for Adtran across the full program. In Europe, the transatlantic dynamic is identical: BT is targeting 24 million fiber homes by the end of 2026, Germany is aiming for 22 million homes, and FiberCop in Italy selected Adtran in January 2026 for its national metro transport rollout utilizing the FSP 3000, Mosaic Network Controller, and coherent 100ZR pluggables. Adtran is a key vendor in this massive copper-to-fiber wave.

On top of this, there is a third silent but powerful driver: Huawei displacement in Europe. The January 2026 revision of the EU Cybersecurity Act makes it binding for member states to replace high-risk vendors from critical infrastructure, directly including fiber optics alongside 5G. Roughly 30% of installed equipment across the EU still comes from high-risk suppliers, impacting key markets like Germany with Vodafone, O2, and T-Mobile, Italy with Windtre, or Spain with MasOrange. At the Needham conference, Tom Stanton described this access and optical opportunity as roughly equal in magnitude, citing a $10 billion-plus installed base to replace over time—a multi-year pipeline where Adtran stands as the best-positioned Western alternative due to its deep ADVA heritage across European carriers.

Q1 2026 fundamentals fully validate the recovery: $286M revenue (+15.5% YoY), +42% YoY US growth, and non-GAAP EPS exploding +367% to $0.14 (a 55% beat). Non-GAAP operating margin expanded +300bps YoY to reach 6.9%.

The only bear case is the DPLTA structure, a German law giving minority shareholders the right to tender shares at €17.21, creating a ~$351.7M contingent liability against $88.3M in cash. Algos panic and sell, causing the discount. In reality, the tender pace is slow (~0.2M shares in Q1 for a ~$4.1M outflow), and liquidity is sufficient. This is just an accounting friction. The massive re-rating trigger will be a LiteWave800 hyperscaler design win or H2 2026 BEAD revenues.