Como no tengo canal YouTube propio, varios me han pedido un listado de todas mis participaciones en canales amigos.

Cada nueva participación la agregaré a este Playlist.

https://t.co/e6hqozHUoa

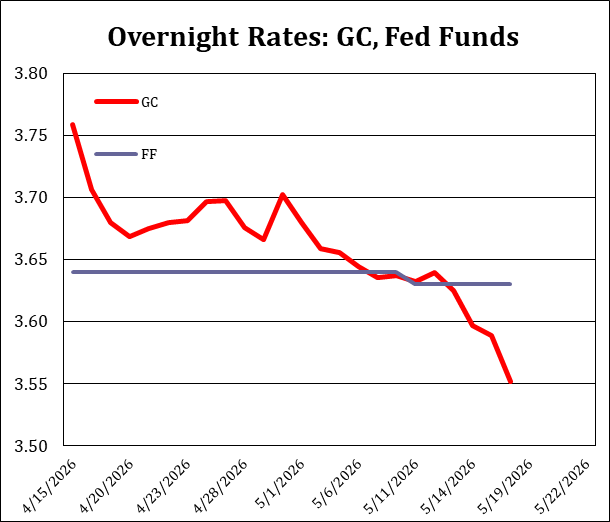

TGCR trading at the lower bound - RRP Offer. This is happening because GSE's are deploying cash into REPO this week, Treasury has spent down TGA post tax-day, and the Fed's RMP. GSE cash will leave leave next week and Treasury is increasing TBill and CMB's lifting this rate. cc @ScottSkyrm@KastoRepo

It looks like the soft REPO funding bottomed. The big move should occur on Tuesday when the GSE cash leave the market and the $140 billion net new issuance begins for the week

#SOFR M6M7 spread hits 40 bps.

The spread between Jun26 and Jun27 SOFR futures has risen over 92 bps since late Feb, as inflation concerns have fueled a dramatic shift in market expectations from cuts to hikes.

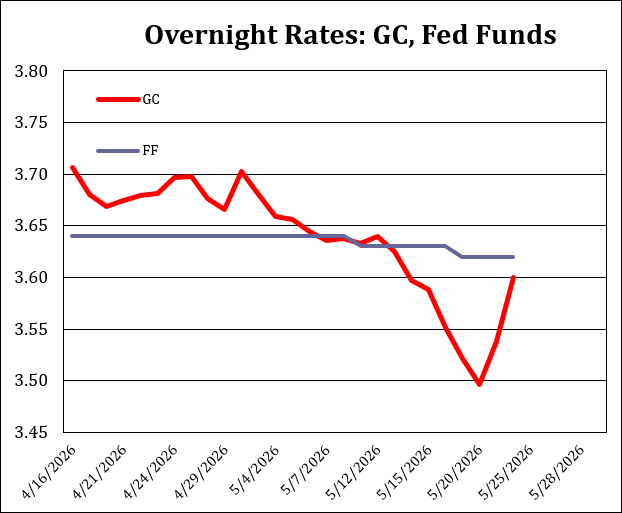

Repo GC continues to move lower. I attribute it to Treasury paydowns, hangover from the late April collateral shortage, and some fundamental factor which added cash to the market. It's a toss up going forward

Anyone who wants to blame Japan for US rates should think long and hard about this graph

The first thing they would/are selling on the back of intervention or to support real demand destruction from oil will be short duration USTs

Clearly plenty of willing buyers.

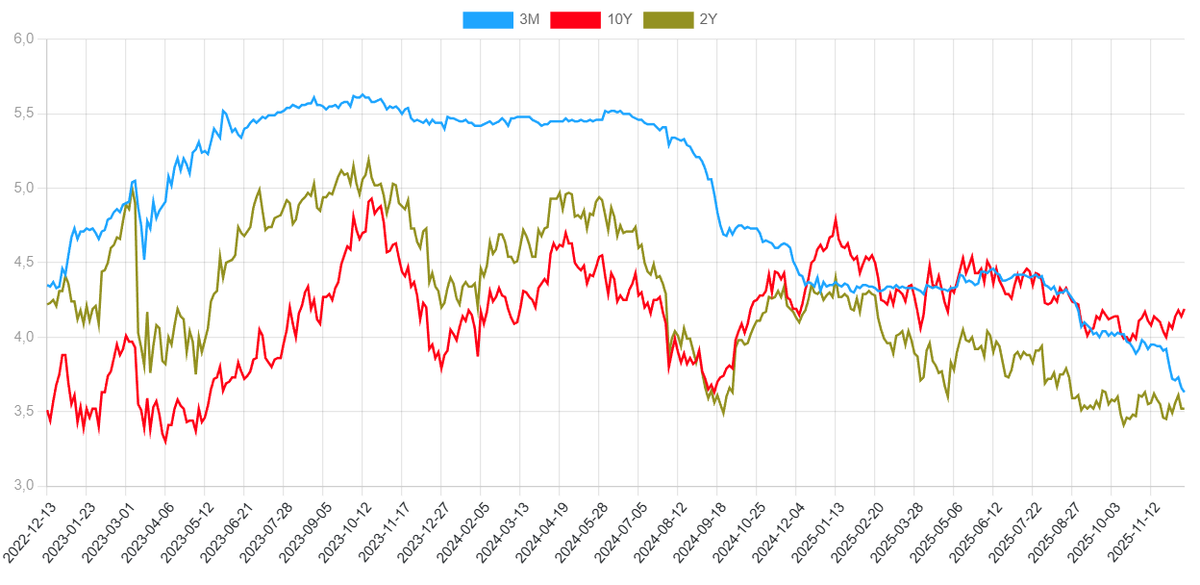

Una curva desinvertida es coherente para el negocio bancario y seguramente sea uno de los objetivos

ya que los bancos se financian a corto plazo y prestan a largo

cuando el spread largo–corto se amplía, mejora el margen de intermediación.