“America sees Sweden better than we see ourselves.”

I came across an article arguing that the new US-Sweden Technology Prosperity Deal reflects something many Swedes struggle to see right now.

From the American perspective, Sweden is not a small country on Europe’s northern edge.

It’s a technology powerhouse.

The agreement highlights Swedish strengths in AI, telecom, semiconductors, advanced manufacturing, energy, defense, space, and critical digital infrastructure.

What struck me is that the same blind spot exists in investing.

As a Swede, it’s easy to spend all day studying Nvidia, Broadcom, and the rest of the US tech ecosystem.

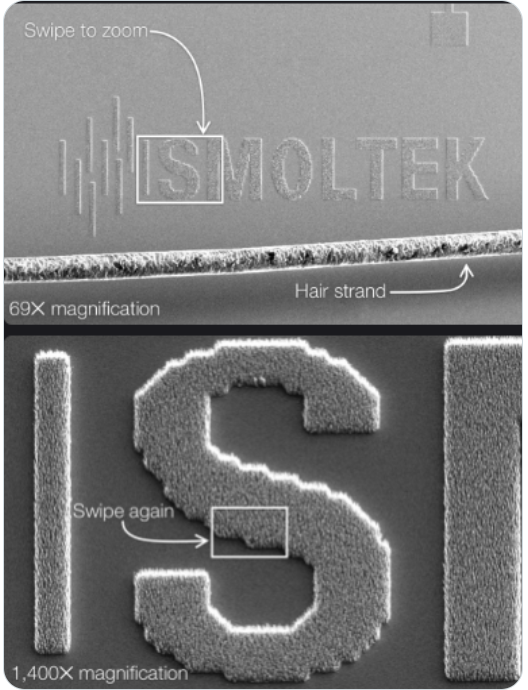

Yet some of the most interesting Swedish tech companies I’ve researched lately, companies like $SIVE, $ACCON, $SHT and $SMOL, were first brought to my attention by fellow investors abroad, mainly in the US.

Sometimes it takes an outsider to recognize the value of what’s right in front of you.

Sweden may need the American pat on the back.

But read the fine print.

The world’s largest economy doesn’t sign strategic technology partnerships out of generosity.

It signs them because it sees capabilities it needs.

America needs Sweden.

https://t.co/Ut4XdUKDRU

New position that can be interesting in the coming days

$LPK

$SMOL

I still have lot of other I keep my eyes on and keep scanning all day

Anything in the same field that got your attentions?

$SMOL seems to be in the same optic of $KOPN and $FABC which have some

Link with how $MRVL just got hyped by $NVDA ceo where these are bottleneck chocking point solution that could run big if adopted by big player like $TSM and such.

Those are my wild card so far but I want to add more.

I’m also in $Accon some lowcap Swedish one

Back in $SMOL 10% port size at 3.34 SEK. Completely different risk/reward now that the company is funded for the foreseeable future. I still think a licence deal is close, and the liquidity is no longer a worry.

Bear case: dilution.

Bull case: Smoltek is now funded to focus on execution.

Bears see this dilution as a death sentence when in fact it is a life sentence.

This financing provides the resources needed to advance commercialization, deepen customer discussions, and prepare for future production scale-up.

The market often prices today’s dilution while ignoring tomorrow’s opportunities.

$SMOL 🚀

$SMOL #Smoltek

A lot of investors seem to view the rights issue as purely negative.

I think the situation deserves a more balanced discussion.

Yes, dilution is never ideal.

But the rights issue also provides something equally important: time.

Based on the company's stated plans and current cost structure, the capital raise significantly extends Smoltek's runway and could provide roughly 18 months of operational funding at current burn rates.

That matters.

Industrial partnerships are rarely signed on the timeline retail investors want. Large industrial players want to see stability, execution capability and a partner that will still be around to deliver.

A stronger balance sheet can improve negotiating position rather than weaken it.

Another point worth considering:

Just weeks ago the market was willing to value Smoltek around SEK 6 per share.

After adjusting for the dilution from the rights issue, a simple theoretical calculation still implies a value around SEK 3.8 per share before considering market sentiment, future news flow, execution risk or additional value creation.

Meanwhile, the company continues to:

• Industrialize with ITRI in Taiwan

• Advance the Gen-One capacitor platform

• Expand manufacturing capabilities

• Work with Heraeus in hydrogen applications

• Pursue a licensing and royalty-based business model

The technology still has to be commercialized.

Commercial agreements still need to be signed.

Nothing is guaranteed.

But there is a meaningful difference between raising capital to continue industrialization and raising capital simply to stay alive.

$SMOL $SMOL (Smoltek Nanotech Holding AB) is a Swedish micro-cap nanotechnology company developing carbon nanofiber (CNF) technology platforms with direct relevance to the AI semiconductor supply chain — particularly in advanced packaging and power delivery for high-performance chips like those in VR200/Rubin racks.

Business Overview

Core Tech — SmolGROW™ / CNF-MIM Capacitors: Patented process for growing 3D carbon nanofibers on substrates (e.g., silicon). Enables ultra-thin CNF-MIM (Carbon Nanofiber Metal-Insulator-Metal) capacitors that can be integrated extremely close to processors (interposers, advanced packaging, heterogeneous integration).

Key benefits: higher capacitance density, lower inductance, better power stability, and reduced heat in power-hungry AI/HPC chips.

Business Split: Smoltek Semi: Focus on semiconductors/AI (decoupling capacitors for power delivery networks in next-gen processors).

Smoltek Hydrogen: CNF electrodes for PEM electrolyzers (lower iridium usage for green hydrogen).

Stage: Pre-commercial / industrialization phase. Targeting volume production 2026–2027 via licensing to partners (not manufacturing themselves).

Q1 2026: No revenue, ~SEK -9.4M loss, thin cash position. Micro-cap (market cap ~SEK 90-500M range recently, volatile; shares around SEK 3-4). Listed on Spotlight Stock Market.

The whole swedish nano, micro and small tech market did an Episodic pivot. We have had a devastating bear market cycle in the short lived history of swedish small and micro cap markets up to 2025-2026.

We have companies like Obducat, Terranet and Smoltek that were down 99.8% as well as new IPO:s. And a stocks like $ACCON and $SIVE with proven tech was down 94% and 95% from highs in 2024 and 2025.

@aleabitoreddit $SMOL 20 years of R&D and patenting. 2026 is Smoltek's breakthrough year. The year in which Smoltek transitions to sales, licensing and revenue generation! With the backing of ITRI, Yageo, Heraeus, and Tong Hsing, the journey now begins for a unique Swedish deep-tech company!