@itsTarH United Foodbrands had the highest Same Stores sales growth among all the QSR Companies at around 14.4%, perhaps thats the reason👇

https://t.co/DHFksXbgha

Wockhardt –An Indian Innovator Pharma Company

Here is an effort from my side to explain what all is happening with Wockhard and why stock is buzzing these days.

1. What is this new drug of Wockhardt (ZAYNICH - WCK 5222)-

Wockhardt is positioned to become the first Indian company to have a New Chemical Entity (NCE) undergo a Fast Track NDA review by the US FDA.

Timeline: Final US approval is projected for mid-2026.

Efficacy: The drug has been administered under compassionate use to 70 late-stage patients(including 3 in the US) who had exhausted all other treatment options. All lives were saved—a feat achieved after ~25 years of dedicated R&D.

2. Understanding the Pharma Landscape-

There are 2 types of Pharma Companies:

Generic (The Volume Game): Most Indian majors (Sun Pharma, Cipla, Dr. Reddy’s) dominate here. They manufacture copycat versions post-patent expiry. This is a high-volume, low-margin commodity business.

Innovator (The Value Game): Global giants (Eli Lilly, Pfizer) dominate here. They identify promising molecules and patent them (20-year protection). Drug development takes initial 10 years. Post-approval, they enjoy ~10 years of market exclusivity. This creates immense pricing power and high margins.

Transition: Until now, Indian companies largely participated in the innovator value chain via CDMOs (services). While the CDMO sector has "China+1" tailwinds, the primary profit pool remains with the IP owner(Innovator). Wockhardt is attempting to bridge this gap.

3. The Valuation Arbitrage-

Wockhardt is transitioning into an innovator with its new drug ZAYNICH.

Market Opportunity: The drug targets a "Superbug" segment(Anti-Biotic) with a massive addressable market. While conservative estimates suggest peak sales of $1.5-2 Billion(This is 6000 crore of sales vs current market cap of 24000 crore), some analyst and management estimates the total addressable market (TAM) across the US, Europe, India, and China could be as high as ~$9 Billion.

Current revenues of the company are ~₹3,000 Cr, yet the Market Cap stands at ~₹24,000 Cr. The market is partly pricing in the NCE potential as share price is up 6 times in last few years. If the company achieves even a fraction of the estimated peak sales and ramp up the sales of the drug quickly, the forward Price-to-Sales valuation becomes highly attractive even at these levels. This is what an innovator drug can do to a pharma company.

4. The Strategic Dilemma: Speed vs. Value-

Management currently faces two choices for commercialization:

A) Out-Licensing: Partner with a global distributor. This ensures immediate cash flow and speed but requires sharing a significant portion of the profit pie.

B) Self-Commercialization: Build a proprietary sales team in the US. This is a slower, capital-intensive process but retains 100% of the margins—beneficial long-term as Wockhardt has 5 other NCEs in the pipeline.

Its upto the company to decide which one suits them.

5. Institutional Validation-

The recent QIP issuance saw strong participation from marquee names like Tata, HDFC, HSBC, and 3P India (Prashant Jain), signaling institutional confidence in the company.

6. The Indian Innovator Precedents-

Only Few Indian companies have successfully navigated the NCE journey, Here are the examples:

Orchid Pharma: Developed Enmetazobactam. Licensed it to Allecra (which faced bankruptcy issues), complicating the commercial ramp-up.

Sun Pharma: Typically acquires late-stage assets (e.g., Ilumya) leveraging its cash reserves rather than relying solely on in-house discovery.

Glenmark: Recently licensed its oncology asset (ISB 2001) to AbbVie during Phase 1. They received upfront payments (total deal value ~$600M+,ie, around 5000 crore), de-risking the asset early.

Conclusion Indian Pharma is moving up the value chain: from Generic Manufacturers ➡️ CDMOs ➡️ True Innovators. Wockhardt is currently leading this high-risk, high-reward transition.

#Wockhardt

Wockhardt –An Indian Innovator Pharma Company

Here is an effort from my side to explain what all is happening with Wockhard and why stock is buzzing these days.

1. What is this new drug of Wockhardt (ZAYNICH - WCK 5222)-

Wockhardt is positioned to become the first Indian company to have a New Chemical Entity (NCE) undergo a Fast Track NDA review by the US FDA.

Timeline: Final US approval is projected for mid-2026.

Efficacy: The drug has been administered under compassionate use to 70 late-stage patients(including 3 in the US) who had exhausted all other treatment options. All lives were saved—a feat achieved after ~25 years of dedicated R&D.

2. Understanding the Pharma Landscape-

There are 2 types of Pharma Companies:

Generic (The Volume Game): Most Indian majors (Sun Pharma, Cipla, Dr. Reddy’s) dominate here. They manufacture copycat versions post-patent expiry. This is a high-volume, low-margin commodity business.

Innovator (The Value Game): Global giants (Eli Lilly, Pfizer) dominate here. They identify promising molecules and patent them (20-year protection). Drug development takes initial 10 years. Post-approval, they enjoy ~10 years of market exclusivity. This creates immense pricing power and high margins.

Transition: Until now, Indian companies largely participated in the innovator value chain via CDMOs (services). While the CDMO sector has "China+1" tailwinds, the primary profit pool remains with the IP owner(Innovator). Wockhardt is attempting to bridge this gap.

3. The Valuation Arbitrage-

Wockhardt is transitioning into an innovator with its new drug ZAYNICH.

Market Opportunity: The drug targets a "Superbug" segment(Anti-Biotic) with a massive addressable market. While conservative estimates suggest peak sales of $1.5-2 Billion(This is 6000 crore of sales vs current market cap of 24000 crore), some analyst and management estimates the total addressable market (TAM) across the US, Europe, India, and China could be as high as ~$9 Billion.

Current revenues of the company are ~₹3,000 Cr, yet the Market Cap stands at ~₹24,000 Cr. The market is partly pricing in the NCE potential as share price is up 6 times in last few years. If the company achieves even a fraction of the estimated peak sales and ramp up the sales of the drug quickly, the forward Price-to-Sales valuation becomes highly attractive even at these levels. This is what an innovator drug can do to a pharma company.

4. The Strategic Dilemma: Speed vs. Value-

Management currently faces two choices for commercialization:

A) Out-Licensing: Partner with a global distributor. This ensures immediate cash flow and speed but requires sharing a significant portion of the profit pie.

B) Self-Commercialization: Build a proprietary sales team in the US. This is a slower, capital-intensive process but retains 100% of the margins—beneficial long-term as Wockhardt has 5 other NCEs in the pipeline.

Its upto the company to decide which one suits them.

5. Institutional Validation-

The recent QIP issuance saw strong participation from marquee names like Tata, HDFC, HSBC, and 3P India (Prashant Jain), signaling institutional confidence in the company.

6. The Indian Innovator Precedents-

Only Few Indian companies have successfully navigated the NCE journey, Here are the examples:

Orchid Pharma: Developed Enmetazobactam. Licensed it to Allecra (which faced bankruptcy issues), complicating the commercial ramp-up.

Sun Pharma: Typically acquires late-stage assets (e.g., Ilumya) leveraging its cash reserves rather than relying solely on in-house discovery.

Glenmark: Recently licensed its oncology asset (ISB 2001) to AbbVie during Phase 1. They received upfront payments (total deal value ~$600M+,ie, around 5000 crore), de-risking the asset early.

Conclusion Indian Pharma is moving up the value chain: from Generic Manufacturers ➡️ CDMOs ➡️ True Innovators. Wockhardt is currently leading this high-risk, high-reward transition.

#Wockhardt

I think this is a smart capital allocation decision by the management. With the share price having doubled in a short period, they are taking advantage of the favorable market conditions to raise as much capital as possible for the company.

While Q4 was their strongest quarter in terms of execution, the nature of the business is such that revenues and order inflows can be lumpy. There is no guarantee that the upcoming quarters will be equally strong. If performance moderates, the company may not get another opportunity to raise capital at such favorable terms in near term. From that perspective, it makes sense to strengthen the balance sheet while the window is open. What do u think?

I know i am going too far, but this is a risk for Shivalik Bimetals. Their all 3 manufacturing is concentrated in this small area of Solan in Himachal Pradesh. This area is prone to all kinds of natural disasters like landslides, forest firest , earthquakes, floods etc. i hope everyone is safe.

Dis- Holding

#ShivalikBimetals

#WATCH | Solan, Himachal Pradesh | A massive forest fire stretches across the Kyarighat village area of Kandaghat. Residents and administrative officials are actively working to douse the fire.

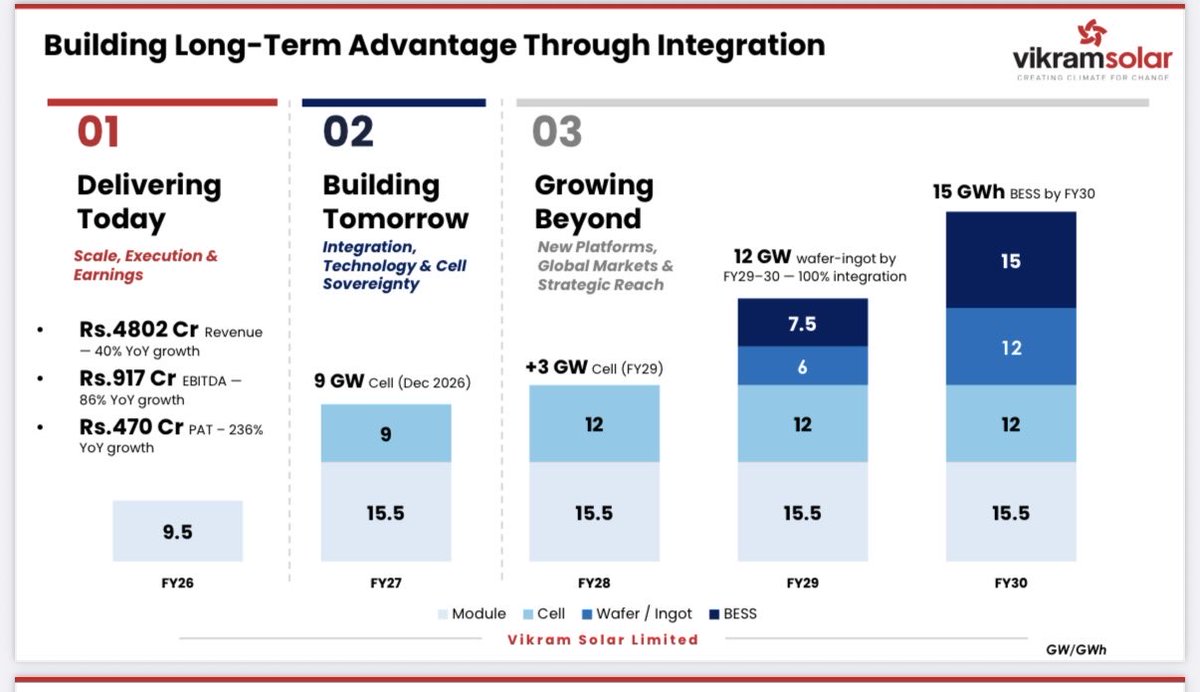

JSW Energy- The Past, the present and the future

Company is in an hyper aggressive expansion phase. From 4.5 GW in FY22 → 13.4 GW today → 30 GW by FY30.

A 24% capacity CAGR in past 3 years. And the next 5 years could be even bigger. Here is the past,present and future plans of the company.

A thread 🧵👇

#Thangamayil Jewellers Share is in such a strong Uptrend since 3-4 years that it has not Closed Comprehensively Below its 200 Day Moving Average since then. Not even in Trump Tariff, Iran War.

Reason- Look at the Strong Sales Growth YoY

Vikram Solar expansion plans are most aggressive in the entire Solar Space. Valuation are also relatively Cheap. Key Question is whether they will be able to execute this or will timeline shift. Markets also worry about the high Debt and Equity dilution this expansion plans may lead to.

Manufacturing Modules is easy but as said in Other Companies calls that Manufacturing/Stabilising and Running Solar Cells is very difficult.

Early Signs will come from next quarter whether the timeline is intact or shifts.

Overall High Risk High Reward bet- if they are able to pull this off, can be a rerating candidate. If timeline shifts, Markets will continue to punish it.

#VikramSolar

@AimInvestments Market is basically pricing it as a commodity company rather than a stable compounder like Gravita. Have too posted about it, do have a look👇

https://t.co/m6RU7pRqkR

Jain Resource Recycling is Down more than 30% in past 2 days since the declaration of Q4FY26 results. Here are the key reasons👇

The Business-

Jain Resource is a metal recycling company - copper (55% of revenue), lead (40%), and aluminium (~5%). Exports account for 62% of FY26 revenue. FY26 headline numbers looked strong - revenue +48%, EBITDA +53%, PAT +56% YoY.

So why the crash?

1. Q4 margin collapse-

Despite strong full-year numbers, Q4 was poor:

• Q3 FY26 EBITDA: ₹198.9 cr | margin: 7.2%

• Q4 FY26 EBITDA: ₹110.0 cr | margin: 3.5% (–45% QoQ)

• PAT from continuing operations: ₹129.5 cr → ₹66.0 cr (–49% QoQ)

Revenue actually grew 12% QoQ, but profitability nearly halved.

2. Why did margins compress - and why didn’t hedging protect?

The company hedges LME (London Metal Exchange) price risk - meaning the base metal price between buying scrap and selling finished metal is typically covered. But Q4 had two hits outside the hedge:

• Sale realisation as % of LME fell 1.25–1.50% - when copper spikes sharply, buyers push down the pricing formula. This “basis risk” is not hedgeable.

• Shipping costs spiked due to Iran-Israel conflict - vessel rerouting, higher port discharge charges, fuel costs - all absorbed in P&L, none recoverable from customers immediately.

Management calls these one-offs.But market dosent seems to believe.

3. Weak cash flow - the bigger concern

FY26 PAT: ₹347 cr

FY26 operating cash flow: –₹591 cr (negative)

Inventory nearly doubled: ₹675 cr → ₹1,477 cr

Receivables jumped: ₹1,295 cr → ₹4,760 cr

In Q3 concall, management had guided working capital to normalise by March and ~50% of PAT to convert into cash. Neither happened. FY26 closed with high inventory, high receivables, and rising debt. That gap between guidance and outcome is what markets punish.

4. Some Governance concerns-

Three separate issues have emerged:

• IPO proceeds worth ₹54 cr were used to repay a promoter loan - explicitly against the IPO prospectus. Company called it an “inadvertent error.” Shareholders ratified it via postal ballot in April 2026. CRISIL now shows no deviation, but the episode raised flags.

• SEBI imposed a ₹25 lakh penalty on promoter Kamlesh Jain for alleged insider trading in Refex Industries. Matter is under appeal at SAT.

• Company Secretary & Compliance Officer resigned, effective June 2026.

Each event in isolation may be manageable. Together, they compound the negative sentiment.

What to watch in Q1/Q2 FY27 going forward-

• EBITDA/tonne recovery - did the margin compression reverse as management guided?

• Working capital days - need to come back to 45–50 days from ~82 days

• Cash flow from operations turning positive

• Any further governance disclosures

Key Lessons from this entire Saga-

Whenever a new Company gets listed, do not jump right into it to invest purely on basis of management commentary especially if its in Commodity related sector. In Commodities sustainability of margins matter more than anything else. Watch out for earning, margins over atleast few Quarters before putting your hard earned money into it.

FY26 on paper was an excellent year. But Q4 quality of earnings - on margins, cash conversion, and governance-raised enough questions for a sharp re-rating.

Key Negatives Highlighted below👇

#JainResource

Jain Resource Recycling is Down more than 30% in past 2 days since the declaration of Q4FY26 results. Here are the key reasons👇

The Business-

Jain Resource is a metal recycling company - copper (55% of revenue), lead (40%), and aluminium (~5%). Exports account for 62% of FY26 revenue. FY26 headline numbers looked strong - revenue +48%, EBITDA +53%, PAT +56% YoY.

So why the crash?

1. Q4 margin collapse-

Despite strong full-year numbers, Q4 was poor:

• Q3 FY26 EBITDA: ₹198.9 cr | margin: 7.2%

• Q4 FY26 EBITDA: ₹110.0 cr | margin: 3.5% (–45% QoQ)

• PAT from continuing operations: ₹129.5 cr → ₹66.0 cr (–49% QoQ)

Revenue actually grew 12% QoQ, but profitability nearly halved.

2. Why did margins compress - and why didn’t hedging protect?

The company hedges LME (London Metal Exchange) price risk - meaning the base metal price between buying scrap and selling finished metal is typically covered. But Q4 had two hits outside the hedge:

• Sale realisation as % of LME fell 1.25–1.50% - when copper spikes sharply, buyers push down the pricing formula. This “basis risk” is not hedgeable.

• Shipping costs spiked due to Iran-Israel conflict - vessel rerouting, higher port discharge charges, fuel costs - all absorbed in P&L, none recoverable from customers immediately.

Management calls these one-offs.But market dosent seems to believe.

3. Weak cash flow - the bigger concern

FY26 PAT: ₹347 cr

FY26 operating cash flow: –₹591 cr (negative)

Inventory nearly doubled: ₹675 cr → ₹1,477 cr

Receivables jumped: ₹1,295 cr → ₹4,760 cr

In Q3 concall, management had guided working capital to normalise by March and ~50% of PAT to convert into cash. Neither happened. FY26 closed with high inventory, high receivables, and rising debt. That gap between guidance and outcome is what markets punish.

4. Some Governance concerns-

Three separate issues have emerged:

• IPO proceeds worth ₹54 cr were used to repay a promoter loan - explicitly against the IPO prospectus. Company called it an “inadvertent error.” Shareholders ratified it via postal ballot in April 2026. CRISIL now shows no deviation, but the episode raised flags.

• SEBI imposed a ₹25 lakh penalty on promoter Kamlesh Jain for alleged insider trading in Refex Industries. Matter is under appeal at SAT.

• Company Secretary & Compliance Officer resigned, effective June 2026.

Each event in isolation may be manageable. Together, they compound the negative sentiment.

What to watch in Q1/Q2 FY27 going forward-

• EBITDA/tonne recovery - did the margin compression reverse as management guided?

• Working capital days - need to come back to 45–50 days from ~82 days

• Cash flow from operations turning positive

• Any further governance disclosures

Key Lessons from this entire Saga-

Whenever a new Company gets listed, do not jump right into it to invest purely on basis of management commentary especially if its in Commodity related sector. In Commodities sustainability of margins matter more than anything else. Watch out for earning, margins over atleast few Quarters before putting your hard earned money into it.

FY26 on paper was an excellent year. But Q4 quality of earnings - on margins, cash conversion, and governance-raised enough questions for a sharp re-rating.

Key Negatives Highlighted below👇

#JainResource

Jain Resource Recycling is Down more than 30% in past 2 days since the declaration of Q4FY26 results. Here are the key reasons👇

The Business-

Jain Resource is a metal recycling company - copper (55% of revenue), lead (40%), and aluminium (~5%). Exports account for 62% of FY26 revenue. FY26 headline numbers looked strong - revenue +48%, EBITDA +53%, PAT +56% YoY.

So why the crash?

1. Q4 margin collapse-

Despite strong full-year numbers, Q4 was poor:

• Q3 FY26 EBITDA: ₹198.9 cr | margin: 7.2%

• Q4 FY26 EBITDA: ₹110.0 cr | margin: 3.5% (–45% QoQ)

• PAT from continuing operations: ₹129.5 cr → ₹66.0 cr (–49% QoQ)

Revenue actually grew 12% QoQ, but profitability nearly halved.

2. Why did margins compress - and why didn’t hedging protect?

The company hedges LME (London Metal Exchange) price risk - meaning the base metal price between buying scrap and selling finished metal is typically covered. But Q4 had two hits outside the hedge:

• Sale realisation as % of LME fell 1.25–1.50% - when copper spikes sharply, buyers push down the pricing formula. This “basis risk” is not hedgeable.

• Shipping costs spiked due to Iran-Israel conflict - vessel rerouting, higher port discharge charges, fuel costs - all absorbed in P&L, none recoverable from customers immediately.

Management calls these one-offs.But market dosent seems to believe.

3. Weak cash flow - the bigger concern

FY26 PAT: ₹347 cr

FY26 operating cash flow: –₹591 cr (negative)

Inventory nearly doubled: ₹675 cr → ₹1,477 cr

Receivables jumped: ₹1,295 cr → ₹4,760 cr

In Q3 concall, management had guided working capital to normalise by March and ~50% of PAT to convert into cash. Neither happened. FY26 closed with high inventory, high receivables, and rising debt. That gap between guidance and outcome is what markets punish.

4. Some Governance concerns-

Three separate issues have emerged:

• IPO proceeds worth ₹54 cr were used to repay a promoter loan - explicitly against the IPO prospectus. Company called it an “inadvertent error.” Shareholders ratified it via postal ballot in April 2026. CRISIL now shows no deviation, but the episode raised flags.

• SEBI imposed a ₹25 lakh penalty on promoter Kamlesh Jain for alleged insider trading in Refex Industries. Matter is under appeal at SAT.

• Company Secretary & Compliance Officer resigned, effective June 2026.

Each event in isolation may be manageable. Together, they compound the negative sentiment.

What to watch in Q1/Q2 FY27 going forward-

• EBITDA/tonne recovery - did the margin compression reverse as management guided?

• Working capital days - need to come back to 45–50 days from ~82 days

• Cash flow from operations turning positive

• Any further governance disclosures

Key Lessons from this entire Saga-

Whenever a new Company gets listed, do not jump right into it to invest purely on basis of management commentary especially if its in Commodity related sector. In Commodities sustainability of margins matter more than anything else. Watch out for earning, margins over atleast few Quarters before putting your hard earned money into it.

FY26 on paper was an excellent year. But Q4 quality of earnings - on margins, cash conversion, and governance-raised enough questions for a sharp re-rating.

Key Negatives Highlighted below👇

#JainResource

Welspun Living has done multiple Buybacks over the last few years. This has reduced its Equity Capital and in a way positive for existing shareholders.

Currently Company is on a recovery path from last years US Tariff Issue. Medium term target-

Revenue- 15000 Crore( Currently 9300 Crores)

Margins- 15%( Currently 8%)

Debt- <1000 Crore( Currently 2300 Crores)

Company will be a beneficiary of the rising FTA signings by India and Textile Sector being employment heavy, is a key focus are of government.

#Welspun

@Normal_2610 Great insights as always. Great to know that u too are positive on Wockhardt. I too posted about it some time back👇

https://t.co/SgOLR6txWK

Wockhardt –An Indian Innovator Pharma Company

Here is an effort from my side to explain what all is happening with Wockhard and why stock is buzzing these days.

1. What is this new drug of Wockhardt (ZAYNICH - WCK 5222)-

Wockhardt is positioned to become the first Indian company to have a New Chemical Entity (NCE) undergo a Fast Track NDA review by the US FDA.

Timeline: Final US approval is projected for mid-2026.

Efficacy: The drug has been administered under compassionate use to 70 late-stage patients(including 3 in the US) who had exhausted all other treatment options. All lives were saved—a feat achieved after ~25 years of dedicated R&D.

2. Understanding the Pharma Landscape-

There are 2 types of Pharma Companies:

Generic (The Volume Game): Most Indian majors (Sun Pharma, Cipla, Dr. Reddy’s) dominate here. They manufacture copycat versions post-patent expiry. This is a high-volume, low-margin commodity business.

Innovator (The Value Game): Global giants (Eli Lilly, Pfizer) dominate here. They identify promising molecules and patent them (20-year protection). Drug development takes initial 10 years. Post-approval, they enjoy ~10 years of market exclusivity. This creates immense pricing power and high margins.

Transition: Until now, Indian companies largely participated in the innovator value chain via CDMOs (services). While the CDMO sector has "China+1" tailwinds, the primary profit pool remains with the IP owner(Innovator). Wockhardt is attempting to bridge this gap.

3. The Valuation Arbitrage-

Wockhardt is transitioning into an innovator with its new drug ZAYNICH.

Market Opportunity: The drug targets a "Superbug" segment(Anti-Biotic) with a massive addressable market. While conservative estimates suggest peak sales of $1.5-2 Billion(This is 6000 crore of sales vs current market cap of 24000 crore), some analyst and management estimates the total addressable market (TAM) across the US, Europe, India, and China could be as high as ~$9 Billion.

Current revenues of the company are ~₹3,000 Cr, yet the Market Cap stands at ~₹24,000 Cr. The market is partly pricing in the NCE potential as share price is up 6 times in last few years. If the company achieves even a fraction of the estimated peak sales and ramp up the sales of the drug quickly, the forward Price-to-Sales valuation becomes highly attractive even at these levels. This is what an innovator drug can do to a pharma company.

4. The Strategic Dilemma: Speed vs. Value-

Management currently faces two choices for commercialization:

A) Out-Licensing: Partner with a global distributor. This ensures immediate cash flow and speed but requires sharing a significant portion of the profit pie.

B) Self-Commercialization: Build a proprietary sales team in the US. This is a slower, capital-intensive process but retains 100% of the margins—beneficial long-term as Wockhardt has 5 other NCEs in the pipeline.

Its upto the company to decide which one suits them.

5. Institutional Validation-

The recent QIP issuance saw strong participation from marquee names like Tata, HDFC, HSBC, and 3P India (Prashant Jain), signaling institutional confidence in the company.

6. The Indian Innovator Precedents-

Only Few Indian companies have successfully navigated the NCE journey, Here are the examples:

Orchid Pharma: Developed Enmetazobactam. Licensed it to Allecra (which faced bankruptcy issues), complicating the commercial ramp-up.

Sun Pharma: Typically acquires late-stage assets (e.g., Ilumya) leveraging its cash reserves rather than relying solely on in-house discovery.

Glenmark: Recently licensed its oncology asset (ISB 2001) to AbbVie during Phase 1. They received upfront payments (total deal value ~$600M+,ie, around 5000 crore), de-risking the asset early.

Conclusion Indian Pharma is moving up the value chain: from Generic Manufacturers ➡️ CDMOs ➡️ True Innovators. Wockhardt is currently leading this high-risk, high-reward transition.

#Wockhardt

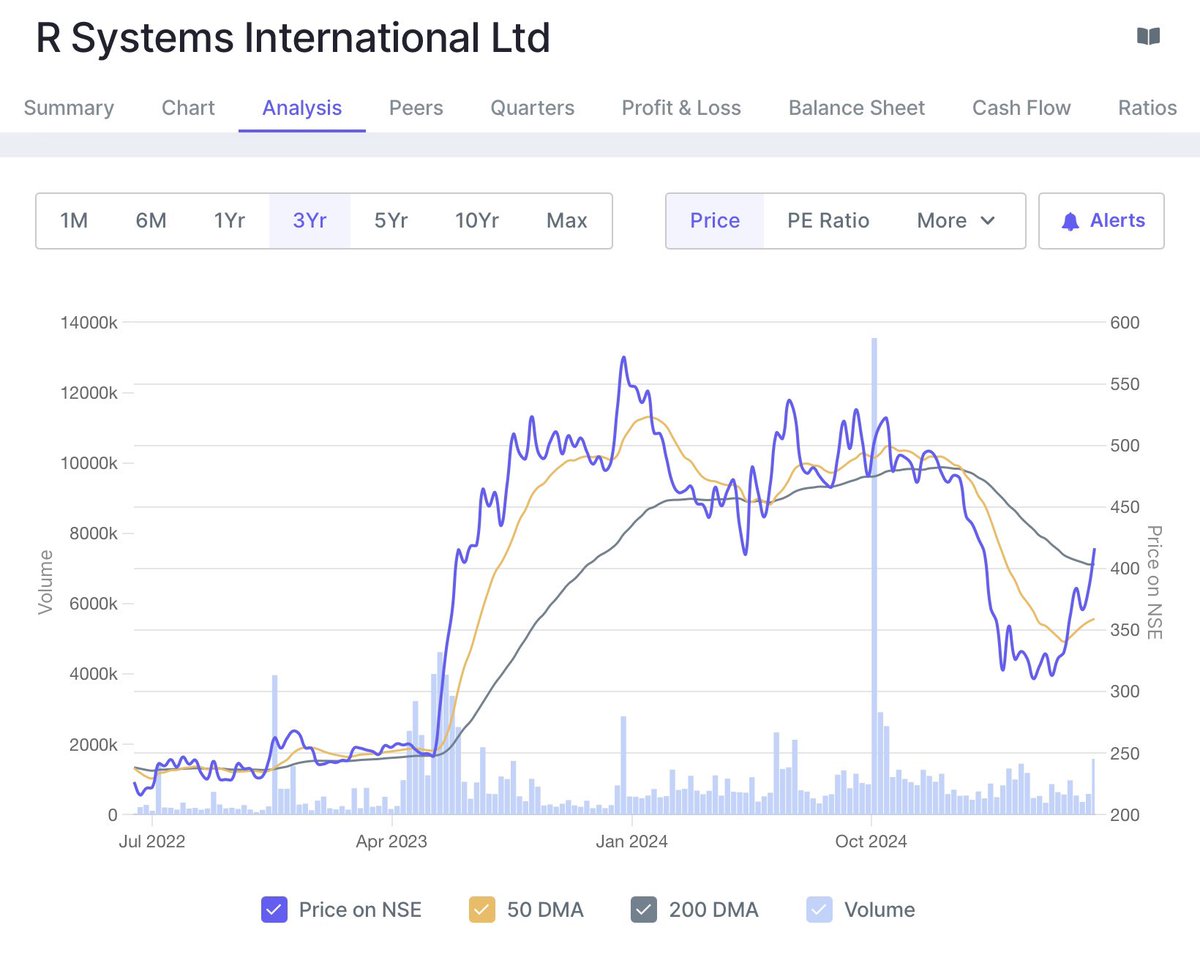

@EquityInsightss I have added more of my small cap IT Holding- RSystems International in last months and current fall. Reasons- Blackstone backed, Sales growth, Margin improvement, Acquisition , Good Valuation. Here is my past post on the same👇

https://t.co/rY48N2ZuqK

A small cap IT company is up 9% today, despite the entire IT sector undergoing pessimism. The company’s name is “ R Systems International”.

Here are some major facts about the company-

Reason for todays fall in #Kaynes Technology share price-

Big spike in inventories and Receivables. Cash Flow Continues to be negative for 2nd year in a row. Profits not translating into Cash Flows. At the same time Management continues to have aggressive expansion plans- may lead to more QIP and Dilution in future.👇