CFA. Debunked Bloomberg's $SMCI spy BS. $GME OG. Ran a $100M+ L/S solar book. Semicap & China enthusiast. Princeton. 1A fan. Value guy, buyer of last resort.

Quite the move in $ACLS / $VECO today - anyone know what's going on beyond the broad strength in semicap?

I'd posted a $VECO long pitch last month (tldr solid growth outlook, too cheap relative to comps):

https://t.co/IY93sisKXX

@stoolpresidente I’m of mixed opinions on him (the blackwater shit is gross), but the way all the worst people are going after him really says something 🤔

Either way Collins is a corrupt POS so can’t possibly in any way be worse than her!!

$DDI just did Q126 FCF/ADS of $0.94, ending the quarter with $10.10/ADS in net cash (up from $9.19/ADS at Q425). $11.25/ADS offer price continues to look like a joke.

Parent company DoubleU Games offering to buy out minority shares of $DDI. The offer price seems way too low, and hopefully DoubleU will be forced to increase it

I wrote up a $DDI long in February

https://t.co/8ktsA7O1O4

"DoubleU offers $11.25 a share to buy out $DDI investors"

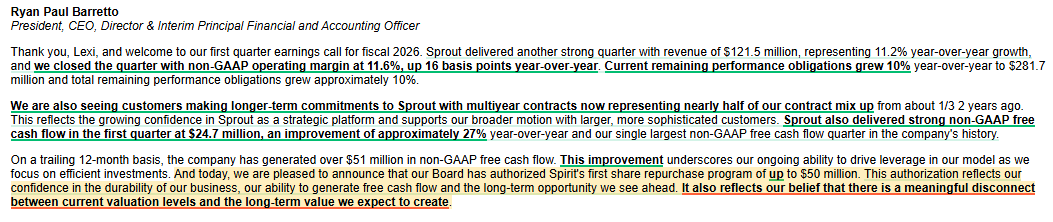

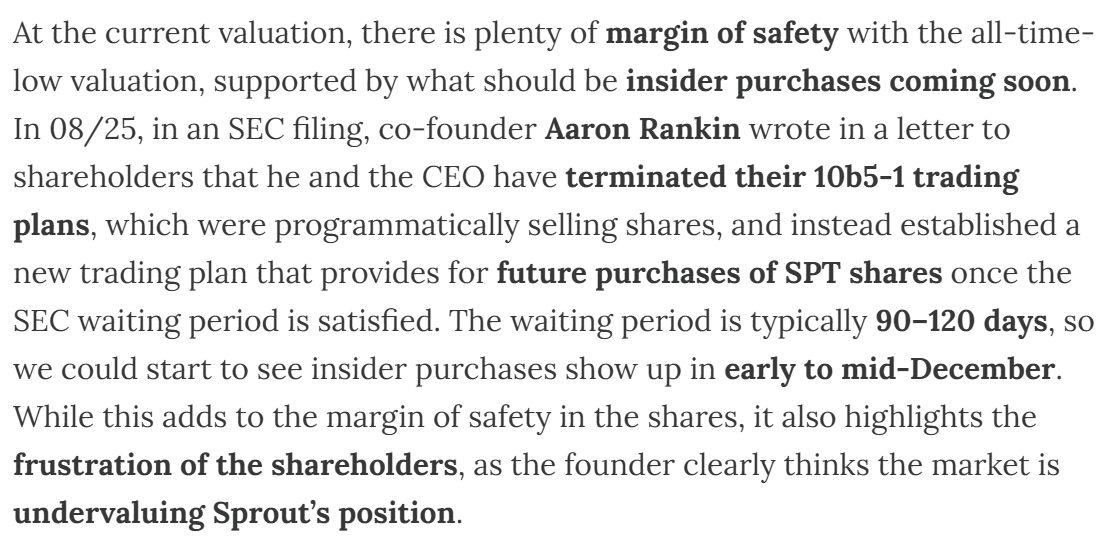

$SPT posted a modest beat/raise in Q126, but more importantly IMO, announced a $50M buyback (against a ~$450M mkt cap). At 0.75x EV/S & 6x EV/FCF on '26 for ~10% top line growth and margin expansion, this is way too cheap and it's good to see the company finally stepping up

Anyone else think $SPT at 1.2x Sales for 10% top line growth, 10% FCF margins is really interesting? I get that all of software is a zero, but what if it’s not 🤔

I’ve been buying this one since November…

$SPT +5.7% post-market on low volume. CEO buys $1M in shares. This comes after co-founder Aaron Rankin purchased $1M a few weeks ago. FWIW, my buyout bets post pitched $SPT as a prime 2026 buyout target and called for planned insider buys to act as a margin of safety 🤣🤣(which clearly has not been the case, still see SPT being bought out tho).

$SPT has been the subject of reported acquisition interest multiple times, including as recently as 3 months ago ( $ADBE )

Ultimately I think this company gets sold much higher than here

Net cash balance sheet and is generating a lot cash. I'd like to see a buyback announcement.

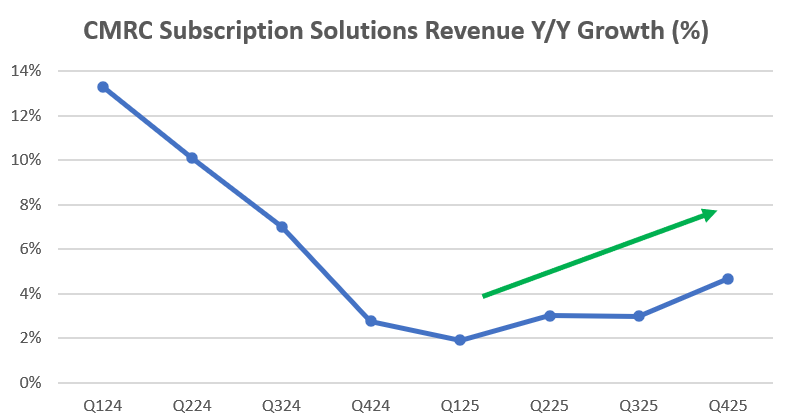

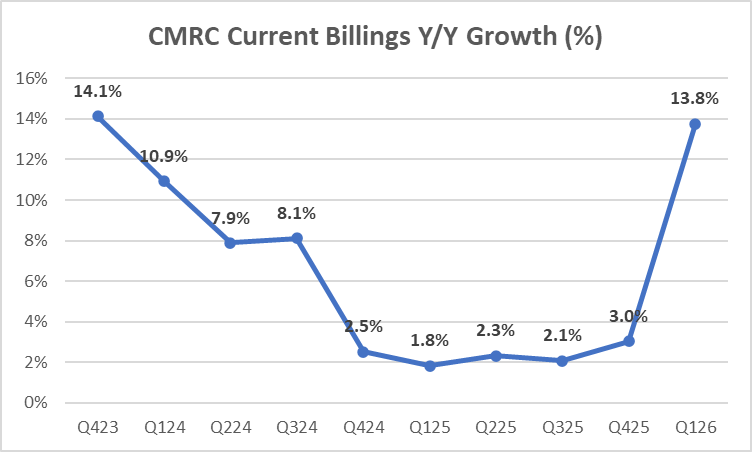

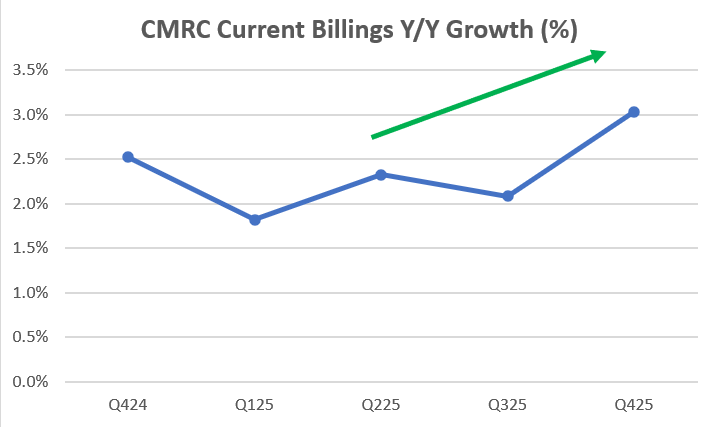

In addition to the blowout acceleration in billings growth, $CMRC reported their first GAAP EPS profitable quarter with $0.05 in Q126 ($0.20 annualized GAAP EPS)

This stock should not still be trading at <1 EV/S (currently 0.87x on CY26)

Turnaround plan at $CMRC seems to be working. The last time $CMRC had 14% billings y/y growth, this was an $8+ stock, except this time around growth is accelerating, not decelerating...

Turnaround plan at $CMRC seems to be working. The last time $CMRC had 14% billings y/y growth, this was an $8+ stock, except this time around growth is accelerating, not decelerating...

Now that $CMRC is disclosing GMV, some observations:

- $CMRC monetizes its GMV as well/better than $SHOP in terms of subscription revs

- $SHOP's better monetization overall is driven by payments ( $CMRC is launching payments this qtr)

- Biggest delta is of course in relative valn

Quite the move in $ACLS / $VECO today - anyone know what's going on beyond the broad strength in semicap?

I'd posted a $VECO long pitch last month (tldr solid growth outlook, too cheap relative to comps):

https://t.co/IY93sisKXX

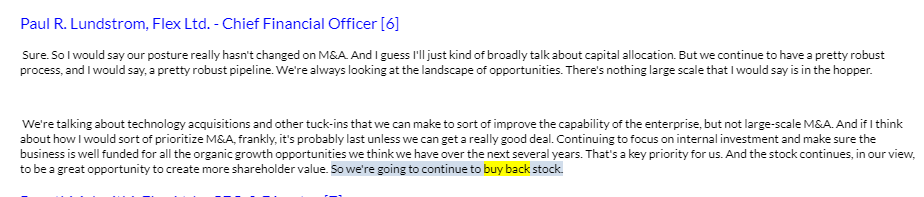

$FLEX now spinning out datacenter biz with the growth outlook below. "Cloud and Power

Infrastructure" segment 25% of revenue / 36% of EBIT in MRQ

Consolidated $FLEX still only trading ~25x fwd adj EPS post the pop

Management going whole hog on buybacks yrs ago looks genius

$FLEX, Buyback Machine

The company bought back $275M last quarter, will do $500M this quarter.

Market cap here is ~$10.5B so this is a serious clip.

Trading at ~11x adj EPS, these aggressive buybacks continue to be nicely accretive

@FishOnCapital It would be a fantastic ROI for DUG to do it at $15, and at that price they might get it done. They seem to want to do something here, and paying up a bit would still be a good deal.

Or maybe they're not serious given the lowball bid, and they'll just walk for now...we'll see