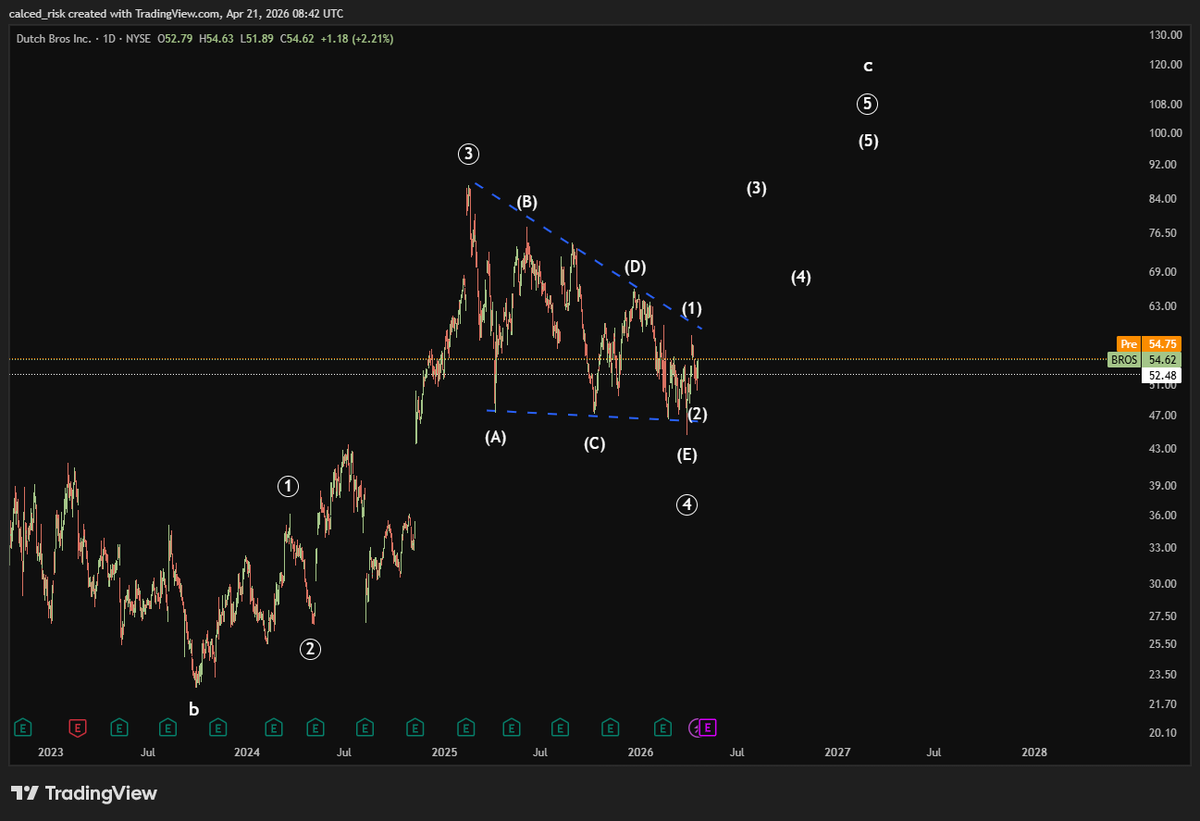

$BROS thesis

I think Dutch Bros represents a tremendous opportunity, both technically (Elliott Wave Theory) and fundamentally.

Think Starbucks, but cheaper, hipper, and with far more room to grow.

72% of orders in 2025 came through the loyalty program.

Read that again.

72%.

That signals very high repeat engagement and strong habit formation.

They are drive‑thru first, so they don’t need large cafés.

CapEx per new store was around 1.3m in 2025.

Same‑store sales growth is solid.

At the same time, store count is expanding aggressively while capital discipline remains high.

New stores are typically paid back within 2–3 years at the shop level.

Revenue is growing at 20%+ annually.

Summary: great growth story with strong unit economics.

Technically speaking, I’m entering at current prices.

Stop loss at 50.26.

Targeting a new ATH.

Let’s see what happens.

Have you ever thought about the fact that gold isn’t scarce if you zoom out? Technology will advance to mine gold in the core of earth. Technology will advance to mine gold on asteroids. Who will still buy gold when this happens? Investment demand will vanish instantly when the market realises. Only a question of time. Only bitcoin is safe (and some other cryptos)

@KillaXBT@cz_binance I’m sorry bro, but I think you’re wrong. Maybe I’ll eat my words, but I’m pretty sure we’ve seen the lows. I think we’ll get a pull back to around 65 but no new lows.

@krishdotdev This is not new guys. I’ve done research on this a year ago. They aren’t the only one, either. At least 3 important other players.

However, brain cells can’t survive for very long. 6 months max is how long they live. Have fun retraining it every 6 months.

All software companies are doomed—without exception. Some argue that “pure” software firms (those creating standalone tools) will die first, while those deeply embedded in client processes (with access to valuable data) might survive. I disagree. Long-term, no software company stands a chance. It boils down to a prisoner’s dilemma.

Consider two large corporations, both relying on SAP modules for finance, HR, ERP, and core operations.

Company A sticks with SAP—it’s already woven into their systems, minimizing short-term disruption.

Company B grants AI full access to all internal data, tasking it to rebuild and optimize SAP’s functionality from scratch. This carries risks: data exposure, potential errors. But if it succeeds, Company B now runs superior, customized software at a tiny fraction of SAP’s licensing fees.

Outcome? Company B slashes prices, captures market share, and outcompetes rivals. Company A, clinging to the old model, gets squeezed out by market forces.

Refusing AI access seals your fate. Every firm will face this choice: embrace the risk or perish. SAP’s cash flows might hold for a few extra years as transitions drag on, but the end is inevitable.

Software is dead. Shouldn’t be worth more then the next couple of years of discounted cash flows

#Software #stocks #ai

@Danny_Crypton These are puts. Blue bars are puts, grey bars are calls. Barely any calls at 20k. These are mostly in the money puts. This graphic is not overly complicated yet still misunderstood. Crazy shit how easily people are influenced