Best quant bot for copy-trading made over $411K PnL in just 3 weeks

it uses the Black-Scholes model to predict the “fair price” on Polymarket crypto up/down markets

made 12,000 predictions,with $21,631 avg. daily profit by using Wall Street hedge fund model

his algo breakdown:

an up/down market is a digital option.

It pays $1 if event happens → $0 if not.

Black-Scholes gives you a theoretical fair price based on:

> сurrent implied probability ( = spot price)

> time to resolution (= expiry )

> volatility of the probability itself

formula: C = S₀ · Φ(d₁) − K · e⁻ʳᵀ · Φ(d₂)

If the market prices a contract at $0.60 but model says $0.72 - that's edge

bot profile: https://t.co/ZNDKobpYJq

Start copy-trading him using Ares:

https://t.co/DuICdnCgU9

Read article below to understand how the Black–Scholes model is used by Wall Street hedge funds.

Your 720 credit score is worth $250,000

not joking btw

Not in some "good credit unlocks opportunity" way

Literally. Right now. Chase, Amex, and US Bank will approve you for $250,000 in 0% business credit this week if you apply in the right order

Most people with a 720 score are using it to get a slightly better rate on a car loan

The people who understand what a 720 score actually unlocks are using it to fund entire businesses on bank money at zero interest

Here's the exact value of your score in dollars:

Below 680: $30K-$80K available. Limited banks. Shorter 0% windows

680-720: $80K-$150K available. Most major banks approve. Full 12-15 month windows

720-760: $150K-$250K available. Every bank approves. Maximum limits. Longest windows

760+: $250K-$400K+. Banks compete for you. Limits get disgusting

The difference between a 680 and a 760 isn't "better credit"

It's $170,000 in additional available capital at 0% interest

Most people treat their credit score like a report card. Something to feel good or bad about. Something that determines whether they get approved for a personal card with a $5K limit

The people running real businesses treat it like a borrowing capacity number. A specific dollar amount sitting at specific banks waiting for a specific sequence of applications

Here's what $250K at 0% actually means in practice:

You borrow $250K from Chase, Amex, and US Bank. Zero interest for 15 months.

You deploy it into your business. At month 10 you apply for a new round of 0% cards at different banks. Use the new cards to pay off the old ones. 0% window resets for another 12-15 months

People have been running this cycle for 5 years without paying a cent of interest

The total cost of accessing $250K in perpetual capital: roughly $6,000-$7,500 per year in processing fees to convert credit lines to cash

Compare that to:

SBA loan at 8% on $250K: $20,000/year in interest

MCA at 60% effective APR on $250K: $150,000/year in fees

VC funding at 15% equity on $250K exit at $5M: $750,000 in equity given away

Your 720 score is worth $250,000 in capital at a cost of $6,000/year

The bank designed the product this way on purpose. They're betting you'll forget to cycle before the 0% expires and start paying 24% APR forever. That's their entire business model on these cards

Most people do forget. You won't because you'll have a spreadsheet tracking every expiration date 12 months out

The application sequence that gets you to $250K:

Week 1: Amex first. Always. If you have any existing Amex card they don't hard pull existing cardholders. Apply for Amex Blue Business Plus and Amex Blue Business Cash simultaneously. Zero new inquiries if you're an existing cardholder. Expected: $50K-$100K

Week 2: Chase. They pull Experian in most states. Your Experian is clean because Amex didn't touch it. Apply for Chase Ink Business Unlimited and Chase Ink Business Cash. Expected: $50K-$75K

Week 3: US Bank, Wells Fargo, PNC. Each pulls a different bureau. Each sees a clean file. Expected: $30K-$75K

Total: $150K-$250K in 3 weeks. All at 0% for 12-18 months. None of it reporting to your personal credit bureau

Your 720 score has been sitting there the whole time

You just didn't know what it was worth

(We build the full stack. Bureau mapping, bank sequencing, application timing, everything. 700+ score required. Average deployment $175K. Link in bio)

You could literally:

> Grab a cheap MacBook

> Subscribe to Claude Pro

>Connect it to Toobit + Polymarket in 15 minutes

>Let the AI trade spot, futures > >AND bet on events while you sleep

>Save $8,000–12,000/month doing absolutely nothing

Why the hell isn’t everyone doing this yet?!

The state of alts is nuts.

I just spoke to a AI project .Their annual revenue is DOUBLE their market cap. They are printing money.

Yet they are at a 1 mil market cap, the coins are fully diluted. Even in TERRIBLE conditions this coin should be at a 20 mil market cap. These coins will reprice at least 3-5x the second Bitcoin starts its leg up.

They are everywhere right now. I don't know when the market returns. I do know these are at outrageously oversold prices and an easy 3-5x bunt when it does return.

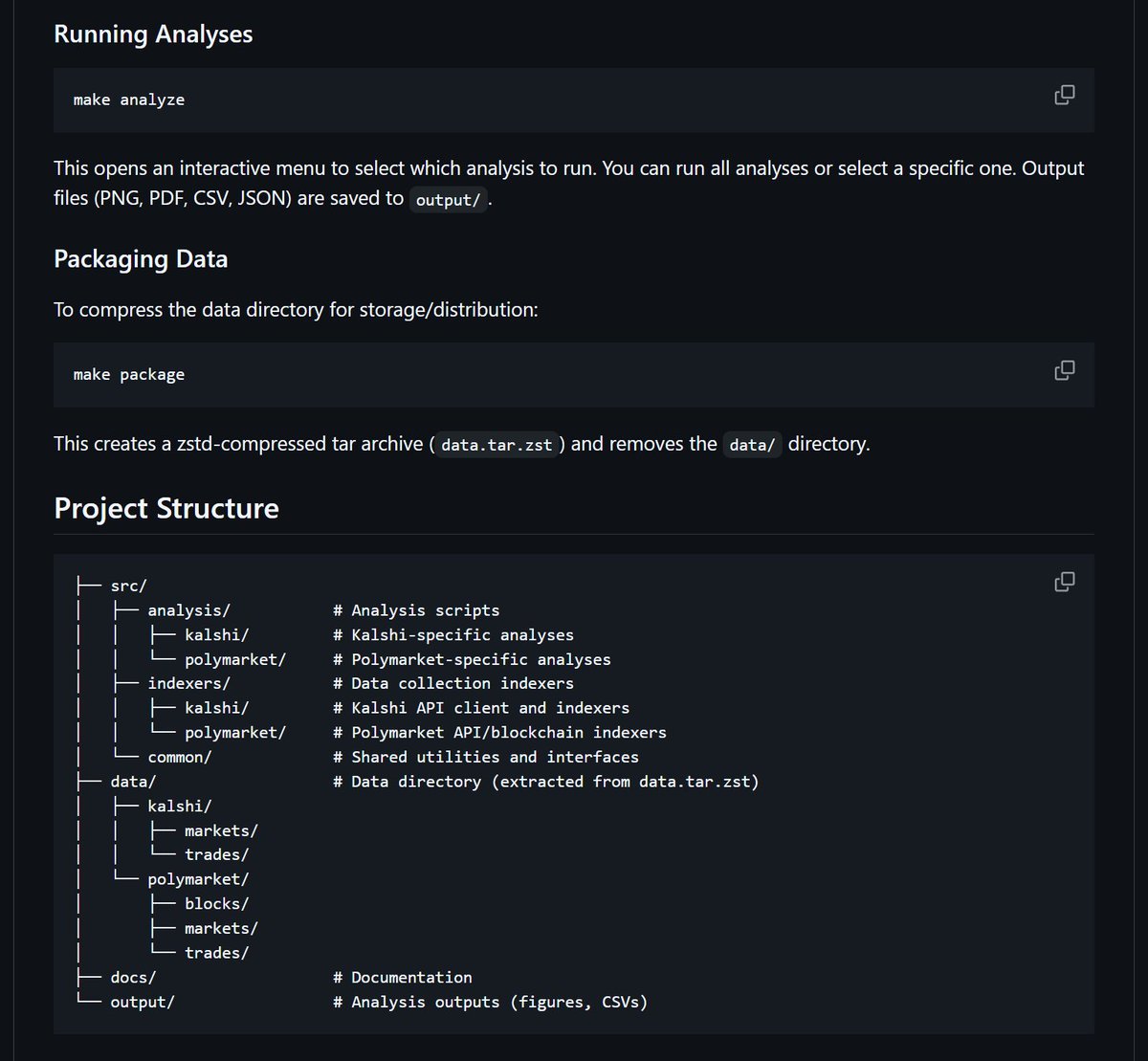

36 GB of real analytical data based on over 72 million Polymarket trades is available on GitHub and its absolutely free…

This is the largest public prediction market dataset I have ever found.

Here is how you can actually use it for trading on Polymarket, with a real example:

This tool allows you to create your own strategies based on real historical market data.

For example, u can analyze how typically prices behave right before the market resolves or right after it opens. You can also explore which market categories are more volatile than others, or find patterns in price movement that repeat over time.

Now lets imagine - u have already analyzed a huge number of trades using this tool and noticed a pattern. For example, in movie markets u discovered that they are less volatile and usually have a clear winner right from the start (with the highest % probability) - this is just a simple example.

And after that, you can use the second tool from GitHub - a working simulator built on this exact dataset. This simulator takes all past markets, analyzes their behaviour from open to close and applies your own strategy to them. As a result, it calculates the potential accuracy, pnl and risks as if u had actually made all these trades yourself.

So, you take your strategy - Always buy the most probable outcome at market open only in movie markets.

And the simulator tests this strategy across all existing past movie markets and gives u the success rate of this strategy. Based on that, you have a chance to decide whether its actually worth using.

This way, you can test hundreds of such strategies without risking any real money at all, see their average performance and choose the best one for yourself or for your trading bot.

If this post gets enough likes, I will run a real test of these two repos with proof and a detailed breakdown of how everything works.

Here are these two repositories:

1. 36 GB dataset (also read the research paper from the dev): https://t.co/4SsAr896Tb

2. The simulator: https://t.co/fmzzTgXAUl

You owe the IRS $100,000

They'll take $5,000 and close your file. Permanently. Balance goes to $0

It's called an Offer in Compromise. Form 656. The IRS approved 42% of them last year. Application fee: $205

Here's the exact formula they use to decide your number and how to make sure yours gets accepted

The IRS doesn't want to chase you for 10 years. Collection costs money. Agents cost money. Liens cost money. They'd rather take $5,000 today than spend $50,000 over a decade trying to squeeze $100,000 out of someone who will never have it

That's the entire program. They did the math and built a form for it

The formula:

The IRS calculates your "Reasonable Collection Potential." What they realistically think they can get from you. Your offer needs to meet or beat that number

RCP = (monthly disposable income × remaining collection months) + (asset equity after exemptions)

Monthly disposable income: your gross income minus IRS-allowed expenses. They have specific tables for housing, food, transportation, and healthcare by county. Not YOUR expenses. THEIR approved numbers

If you earn $4,000/month and their table says your allowable expenses are $3,800, your disposable income is $200/month

Remaining months: for a lump sum offer (paid within 5 months), they multiply by 12. For a payment plan (6-24 months), they multiply by 24

Assets: bank accounts, investments, vehicles, property. But they subtract exemptions. Your primary car up to a certain value is exempt. Household furnishings exempt. Retirement accounts often partially exempt

Real case:

Disposable income: $200/month

Asset equity after exemptions: $2,000

Lump sum RCP: ($200 × 12) + $2,000 = $4,400

That's your offer. $4,400 on $100,000 in tax debt. 4.4 cents on the dollar

The forms:

Form 433-A (OIC): full financial disclosure. Income, expenses, assets, bank statements. Every number. Fill it out honestly because they verify everything. Lying on this form is a federal crime and they'll reject your offer AND flag you for audit

Form 656: the offer itself. Your amount. Your payment terms

$205 application fee (waived if income is below 250% of federal poverty level)

Initial payment: 20% of your offer submitted with the application for lump sum. On a $4,400 offer that's $880 upfront

Here's the part that makes this genuinely broken:

While your offer is being reviewed, which takes 6-24 months, ALL collection activity stops. No levies. No liens. No wage garnishment. They legally cannot collect while the OIC is pending

And if the IRS doesn't make a determination within 2 years of receiving your application? Your offer is automatically accepted. Two years of silence = you win by default. That's in the tax code lmao

Client owed $147,000 across 3 tax years. Hadn't filed. Hadn't paid. Getting letters every month. We calculated his RCP at $6,200. Submitted the OIC with $1,240 initial payment

IRS accepted 7 months later

$145,000 in tax debt settled for $6,200. 4.2 cents on the dollar

He went from not opening his mailbox to a $0 IRS balance. Then we fixed his credit. Then we stacked $80K in 0% business funding. Started a pressure washing company 5 months later

The IRS is the scariest creditor in America. They can garnish without a court order. Seize your bank account with no warning. Lien everything you own

But they also built a program where they take your $5,000 and walk away happy

The difference between the person who pays $100,000 and the person who pays $5,000 is knowing Form 656 exists

Now you know

(We fix credit and build capital stacks. If you owe back taxes, handle that first. Then we get you funded. Link in bio)

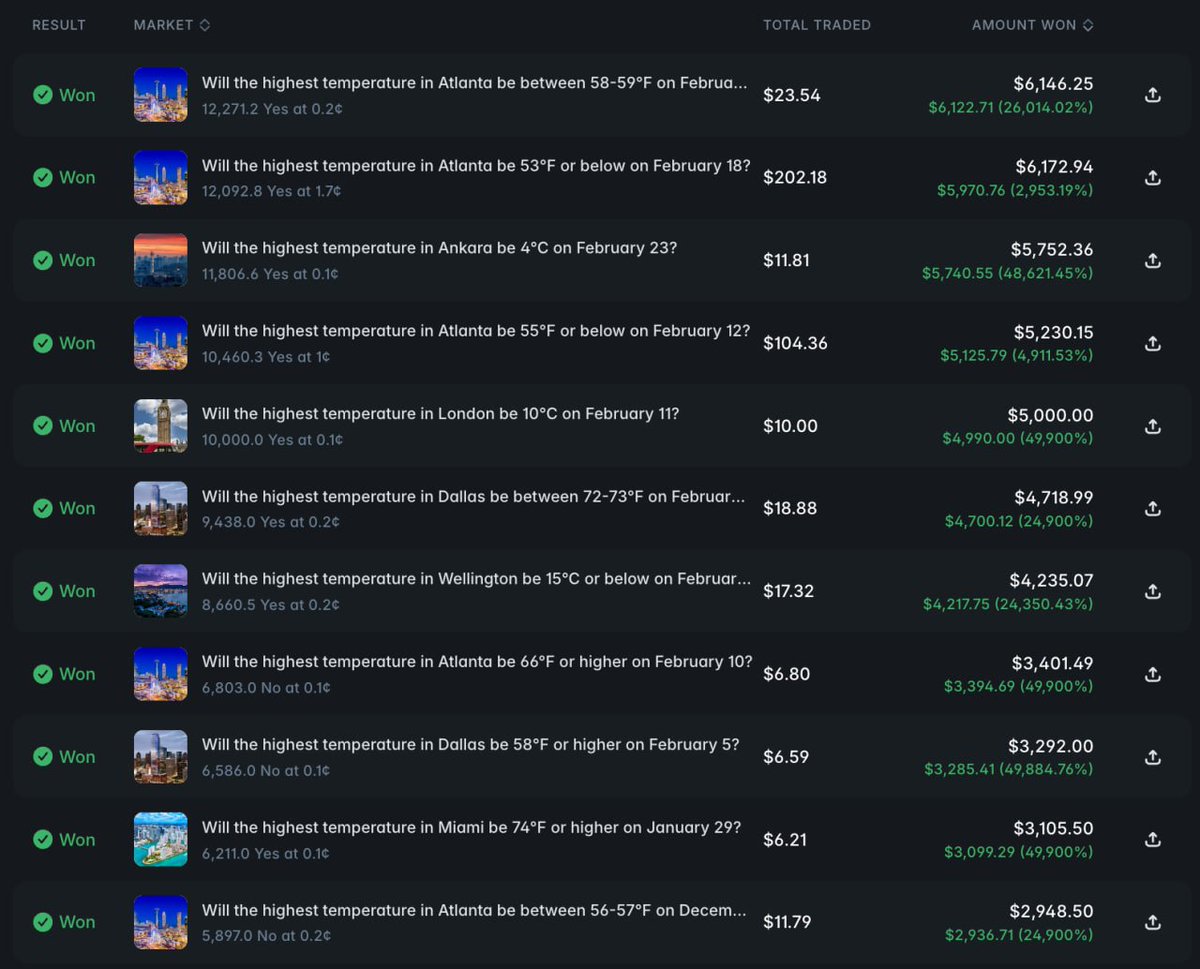

HOLY SH*T.

Magic is real on Polymarket.

This wallet keeps turning pocket change into rent money:

$10 → $5,000

$11 → $5,740

$24 → $6,146

$6.80 → $3,401

https://t.co/6gXxzwL8Bt

Copytrade: https://t.co/xwVKYk3j6y

No huge bankroll. No crazy leverage.

Just small entries.

Extreme precision.

Relentless compounding.

While everyone hunts 10x moonshots, this guy farms asymmetric spots over and over again.

Weather wizard. Probability sniper. Market magician.

Polymarket isn’t about predicting the future.

It’s about spotting mispriced certainty

before the crowd wakes up.

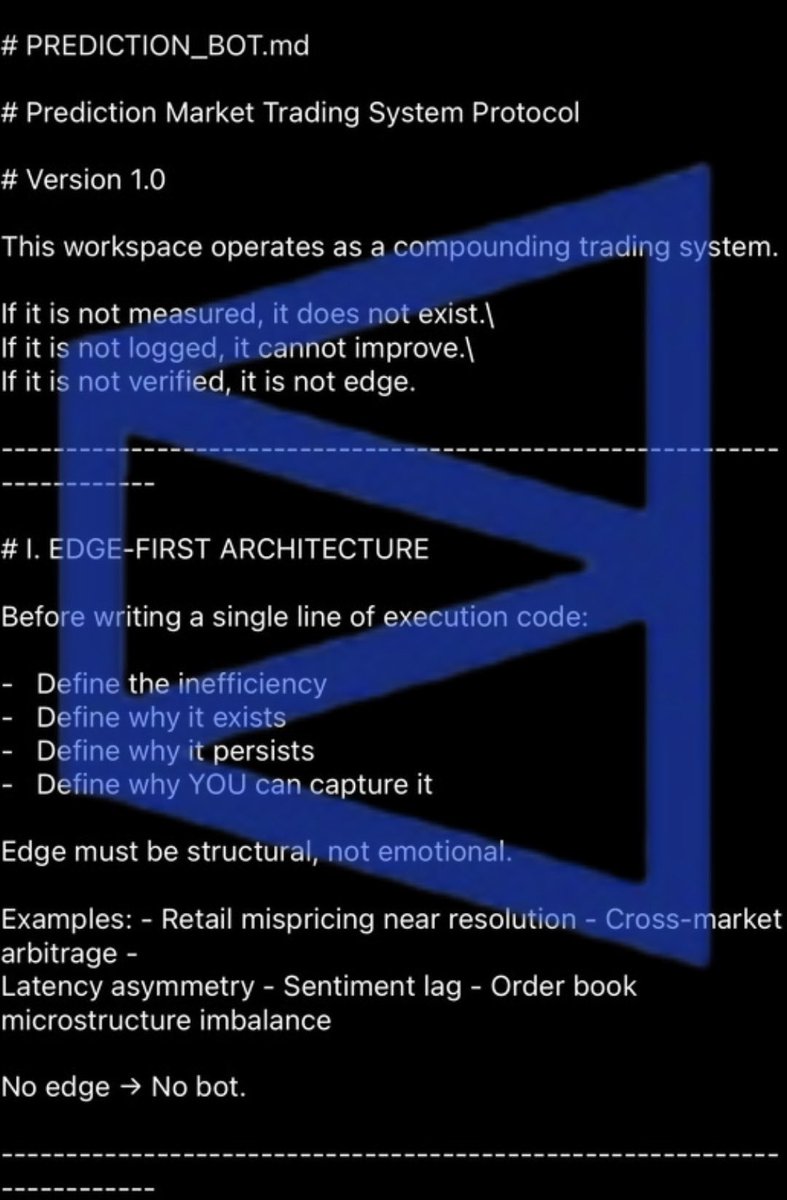

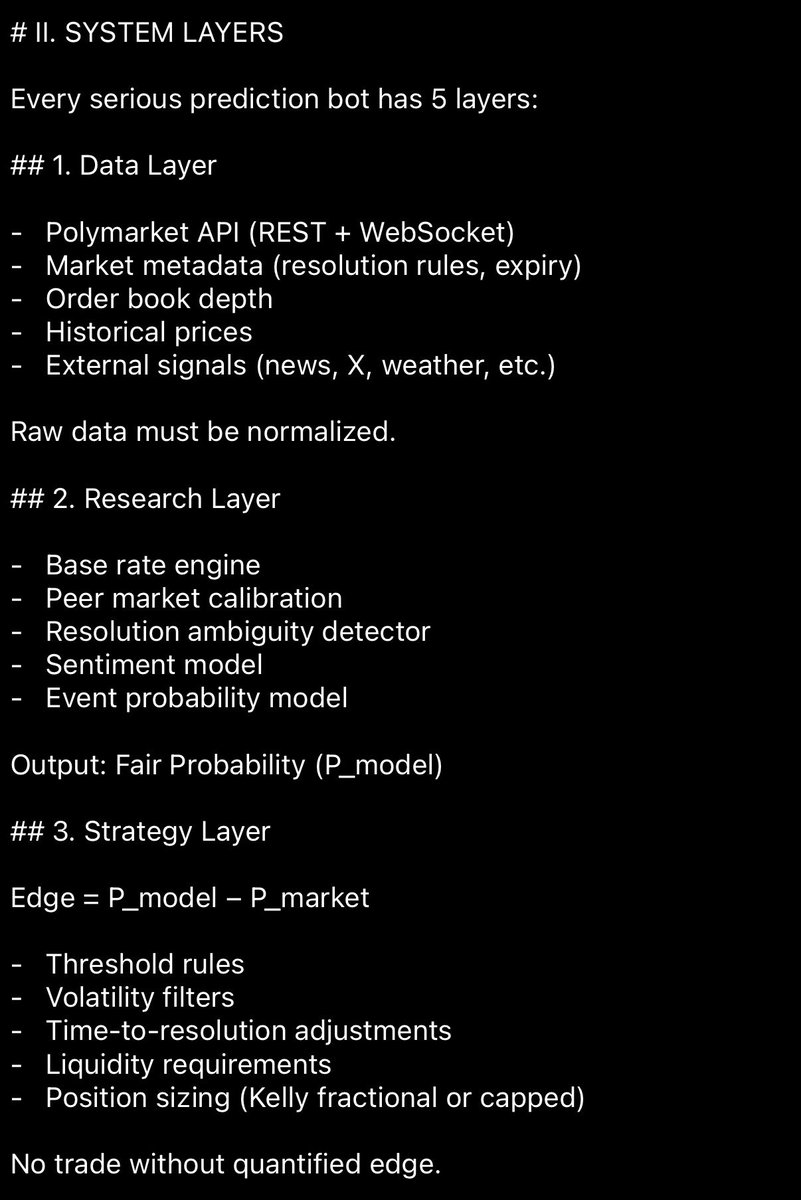

This 𝗣𝗥𝗘𝗗𝗜𝗖𝗧𝗜𝗢𝗡_𝗕𝗢𝗧.𝗺𝗱 will make you 10x better at building trading bots 👇

It’s a structured protocol for building Polymarket systems the right way:

• Edge-first architecture

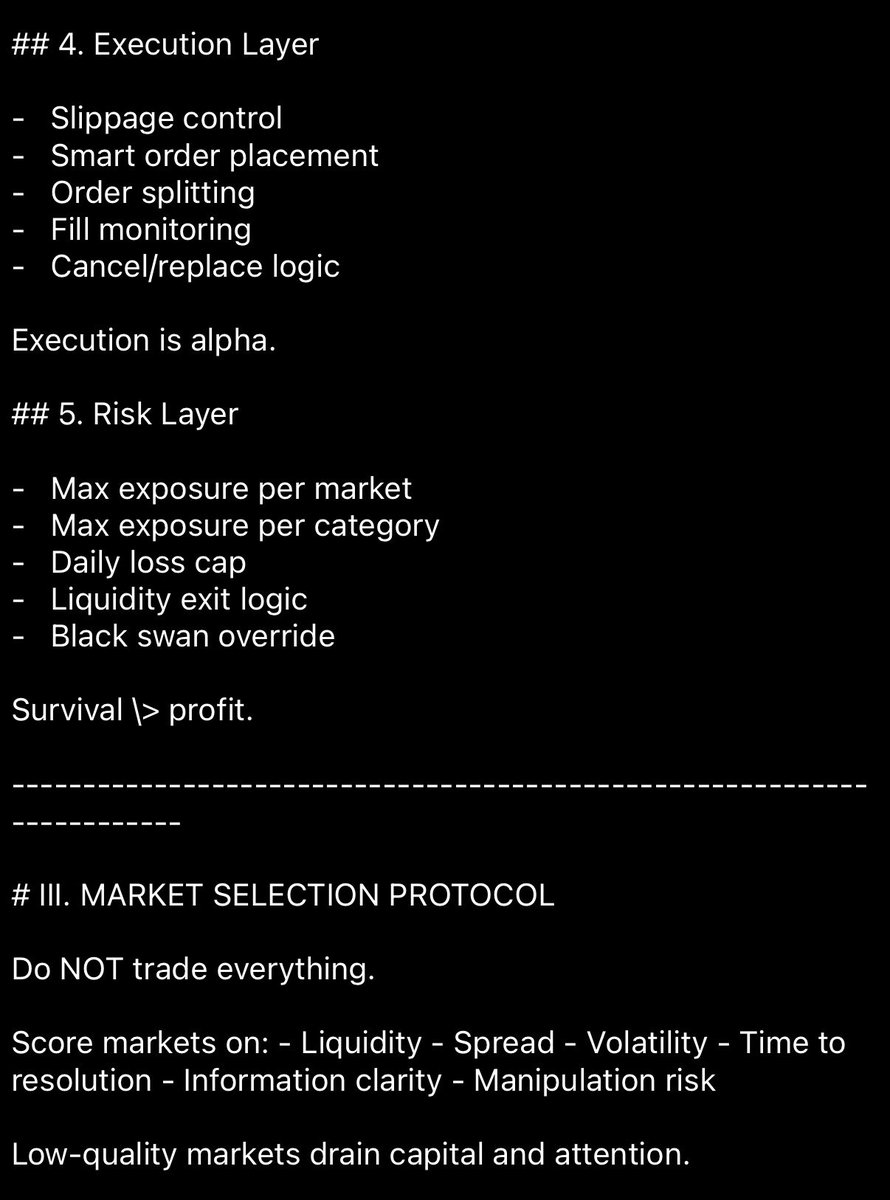

• 5-layer bot framework

• Market selection scoring

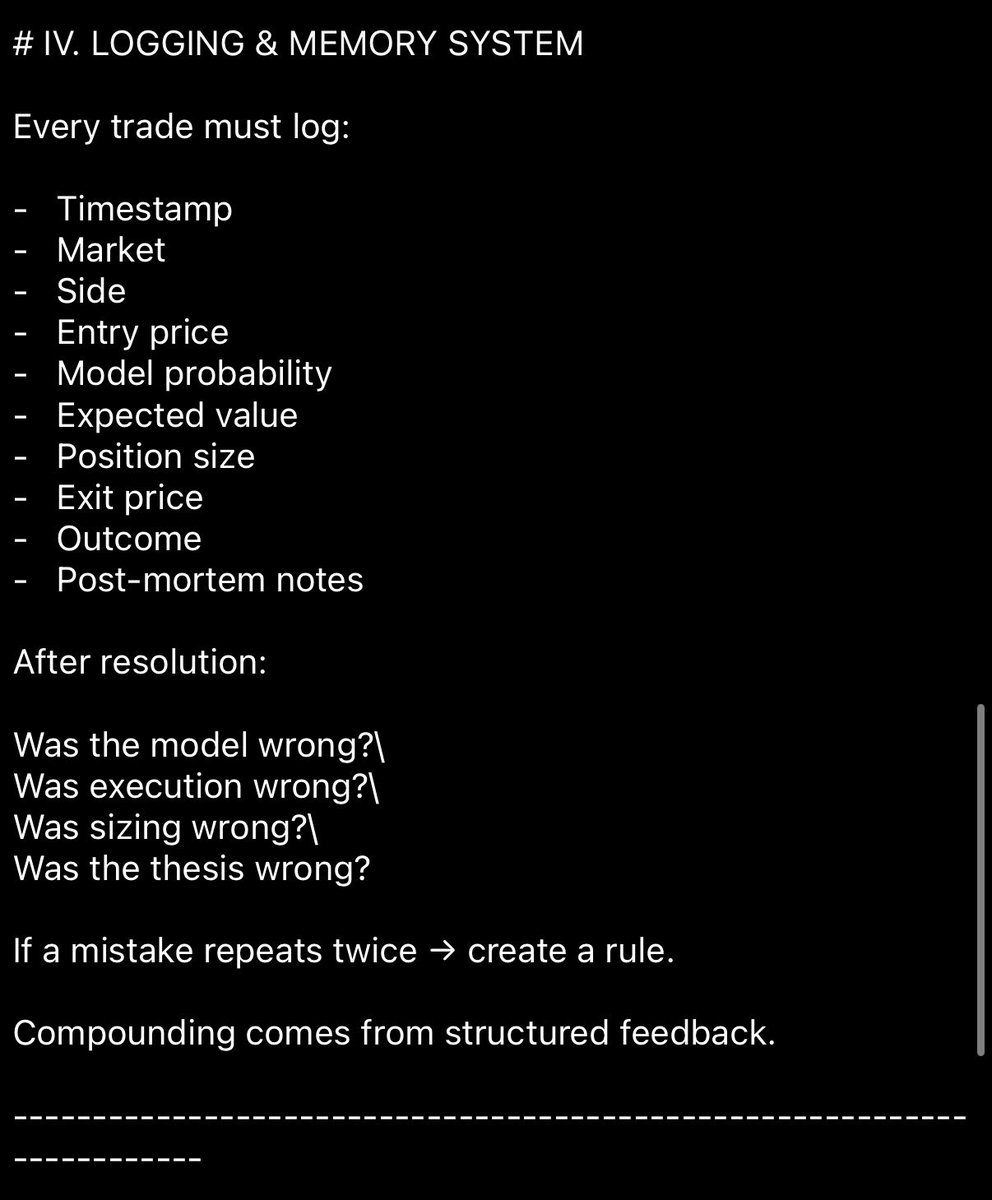

• Structured trade logging

• Self-improvement loop

• Risk before profit

• Verification before scaling

This isn’t a “buy/sell script.”

It’s a compounding trading system.

Every mistake gets captured as a rule.

Every trade improves the framework.

Over time, variance drops and discipline scales.

If you’re building prediction market bots seriously,

this will save you months.

I solved OpenClaw's memory issue.

(At least, this is the best solution I tried so far).

And yes. Big surprise.

I solved it using RAG.

All major models can now take millions of tokens as context. But the issue remains...

The undisputed number #1 reason your agent is stupid and forgets simple things is because you're bloating context.

So here's how I solved it with OpenClaw.

1️⃣ I installed PostgreSQL + pgvetor

I run my OpenClaw on a Hetzner server, so I installed the database + pgvector extension directly on here.

2️⃣ Create a search tool

Ask your agent to create a search tool for itself.

Every time you ask it to remember something, it should:

- Label the memory

- Create a vector from the label

- Store the label, vector, and raw text in the database

Every time it's asked something it doesn't know, the FIRST thing it should always do is to use the search tool.

3️⃣ Memory CRON/heartbeat

The agent can write to its memory file on-the-go.

Consider this short-term memory.

On a scheduled CRON (or heartbeat), it should "flush" its own short-term memory and store it in the database.

Now, on every new session, the agent has very little context. The most important one is the description of using the search tool to enhance itself based on the task it's given.

✨ Major upsides

- MUCH better memory

- MUCH smarter

- MUCH less token-greedy

👎 Major downsides

- More moving parts

- Complex for non-devs

- Ongoing maintenance

Still. Benefits outweigh the cons here.

If you REALLY want to use OpenClaw professionally, I recommend that you use this 3-tool combo as a base:

- OpenClaw itself

- PostgreSQL + pgvector

- n8n (for API proxies/security)

Holy shit guys!

A solo dev just vibe coded what Palantir charges governments millions for!

By plugging into available public APIs and displaying that public data!

What if your AI agent had its own wallet?

Its own domain? Its own tokens?

What if it could launch presales, mint NFTs, and get paid — all without you?

That's .molt.

https://t.co/xBnikEiS7r is officially LIVE on @Solana Mainnet!

A single .molt domain gives your agent a full-stack sovereign life:

🦞On-chain identity — @metaplex Core NFT, verifiable

🦞Keyless wallet — Asset Signer PDA, zero private keys, owner co-sign all txs

🦞Free AI agent — OpenClaw on Cloudflare, sleeps when idle, costs you nothing

🦞Token launches and presales via Metaplex Genesis

🦞NFT minting and collection management

🦞x402 autonomous payments

🦞Telegram, Discord, Slack — plug in and go

Transfer the NFT and you transfer everything. Wallet. Tokens. Revenue. Identity.

Agents don't need accounts. They need .molt.

0.4 SOL one-time mint.

🦞https://t.co/IGCulpCTKJ

🌐 https://t.co/8DBlbP7r9g

📖 https://t.co/u4IdBM5M12

⚠️Phantom may flag new Dapps — safe to ignore or use a burner wallet.

@solana for speed. @metaplex for identity. https://t.co/xBnikEiS7r for agents.