Despite energy price caps and direct support for households, we think euro-zone private consumption will fall further than most anticipate in the coming months, and we expect investment and exports to fall too.

Read more here:

https://t.co/gAqwEuUI5f

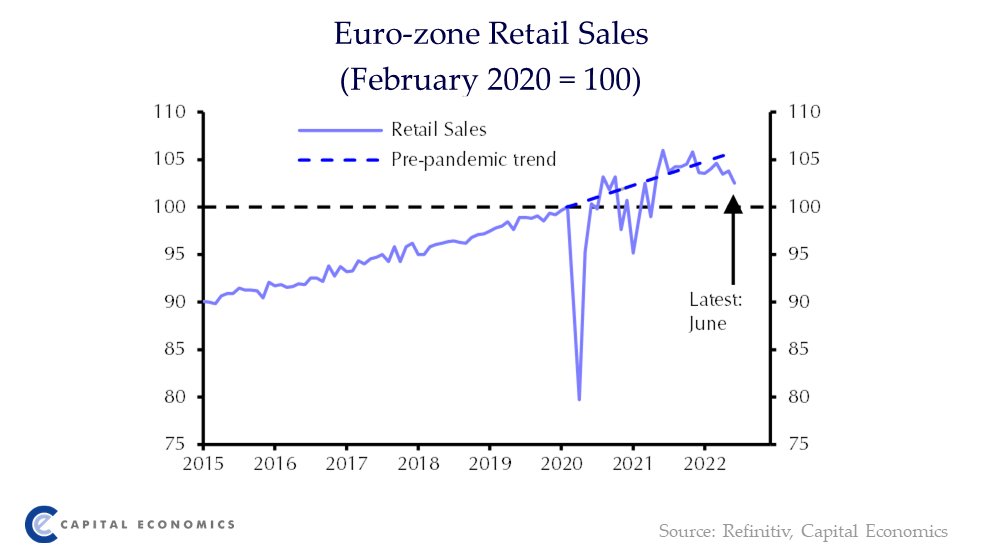

The 2% year-on-year decline in euro-zone retail sales in August will probably look mild by the end of the year. Measures of consumer confidence point to sales falling much further.

Read more here: https://t.co/7SqpZNwceh

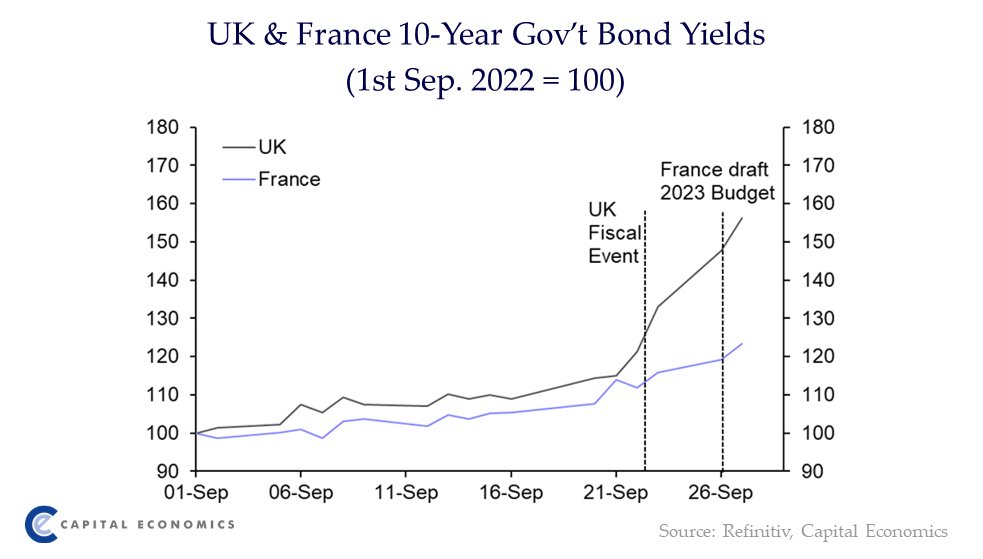

The UK government has not been alone in announcing new fiscal measures. The French government’s plan to stabilise the budget deficit at 5% of GDP next year looks optimistic. However, in contrast, French policymakers also emphasised the importance of medium-term fiscal prudence.

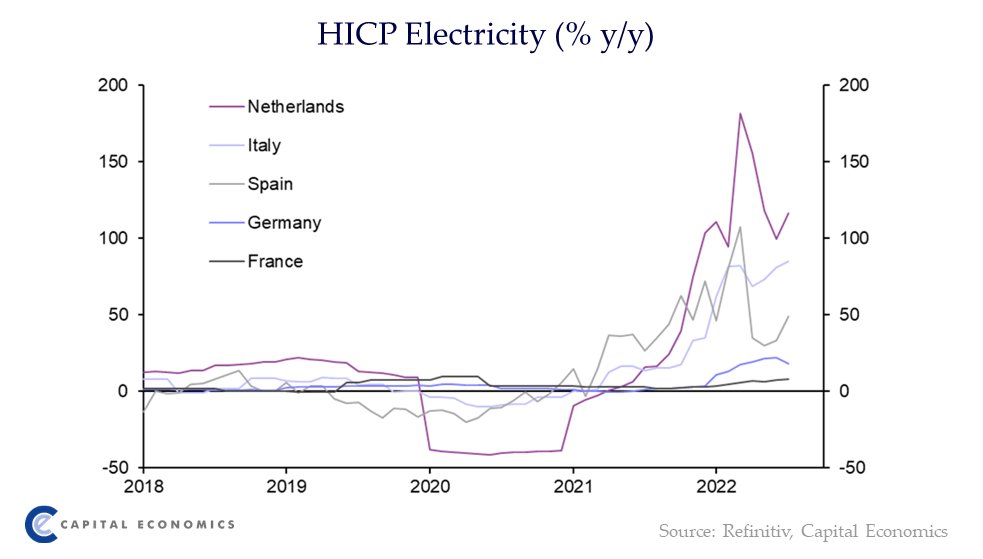

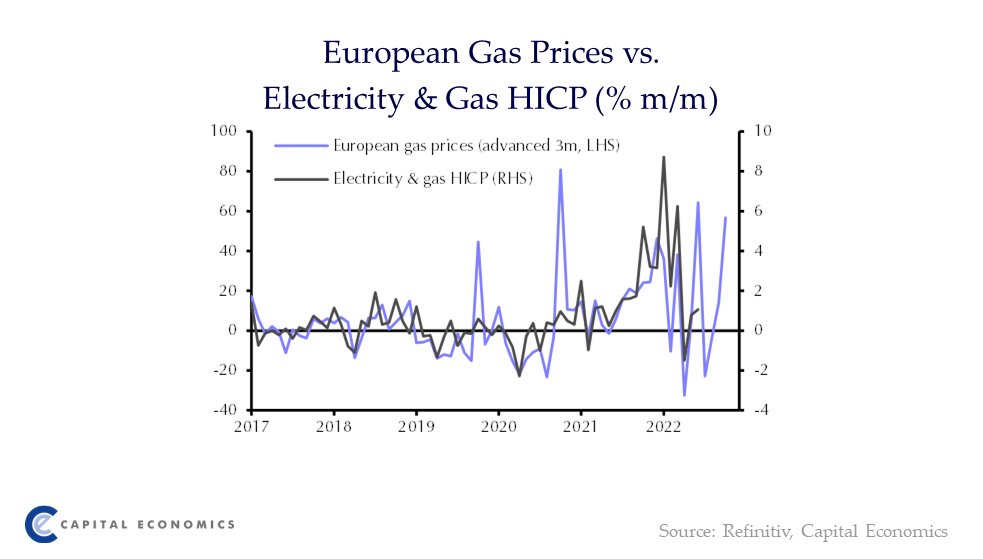

France’s low energy inflation rate relative to those of its neighbours reflects government policies that have limited the increase in retail prices even as wholesale prices have risen.

Read more here:

https://t.co/gBBdV1t9U1

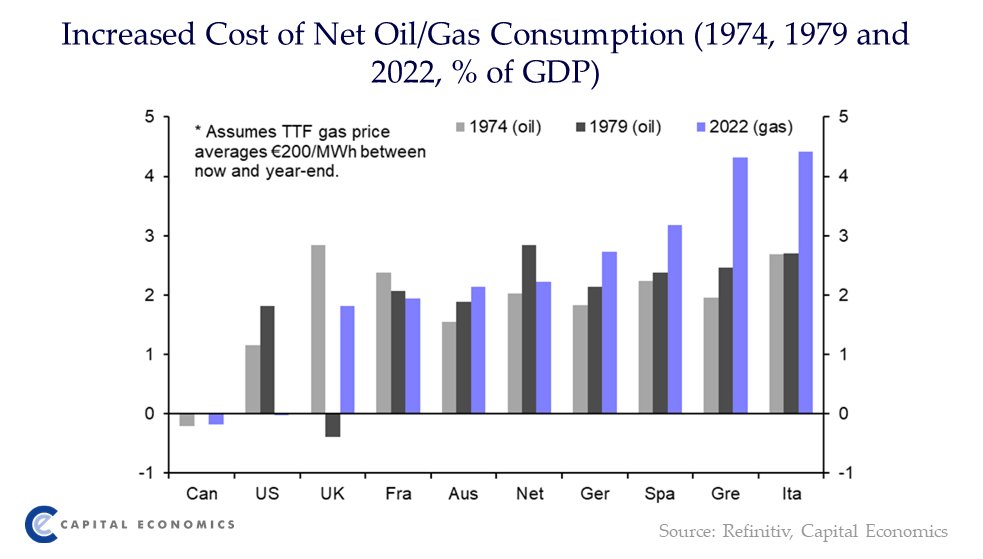

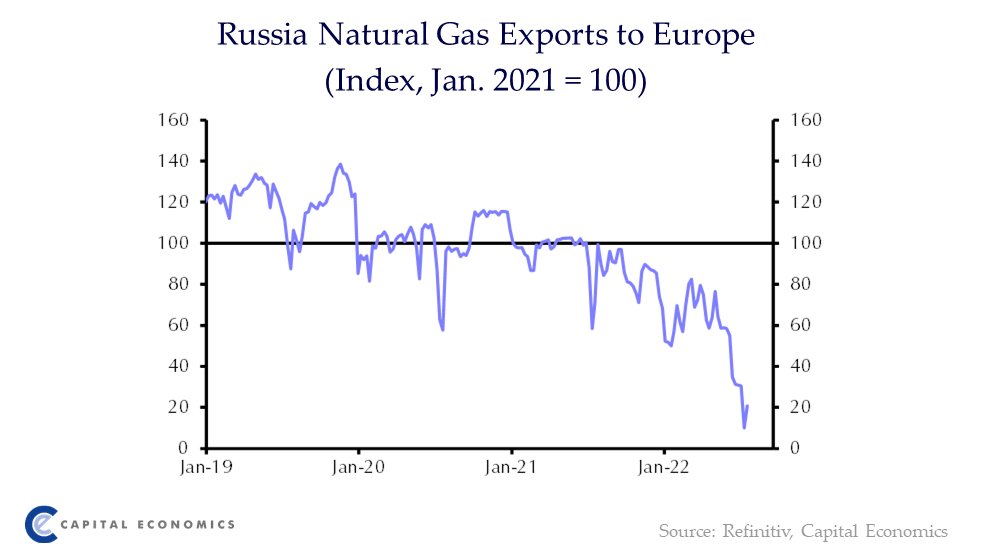

For most major euro-zone countries the terms of trade shock from higher gas prices this year will be bigger than both the 1974 and 1979 oil shocks. How this plays out in the coming months depends on many factors.

Read more here:

https://t.co/Wix1SEzbnh

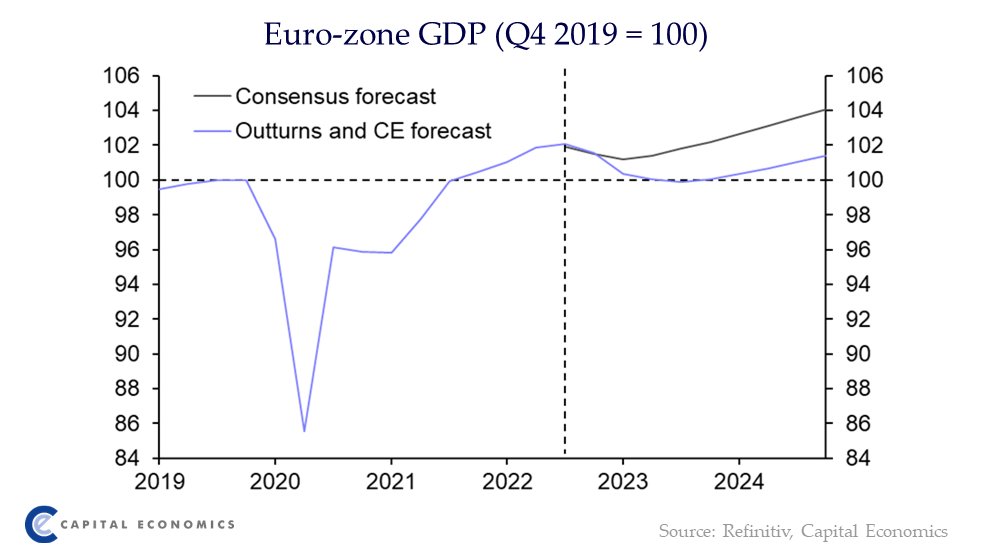

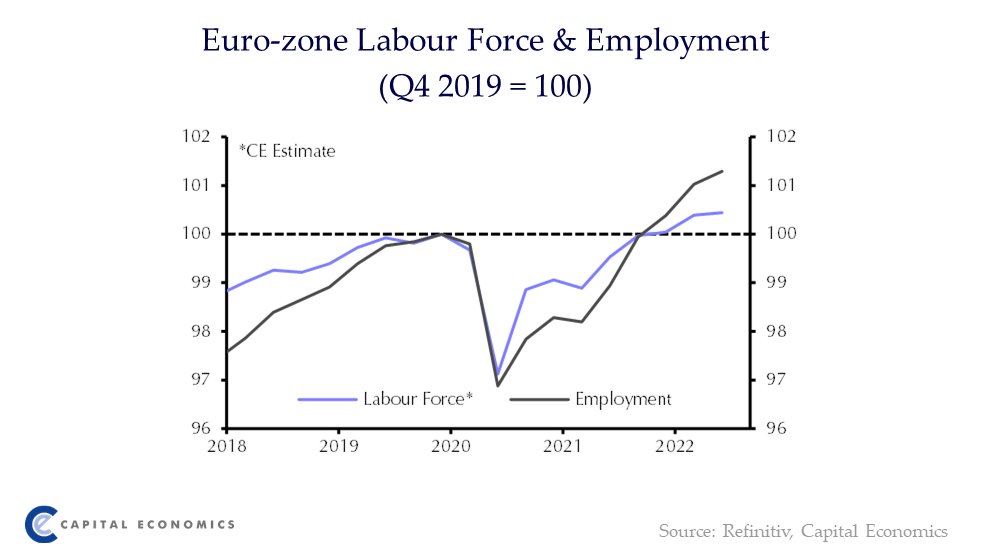

A chunky rise in euro-zone GDP in Q2 was accompanied by a further increase in employment. But a combination of high inflation, rising interest rates and the energy crisis will push the economy into recession before the end of this year.

https://t.co/GGdlBlUaNN

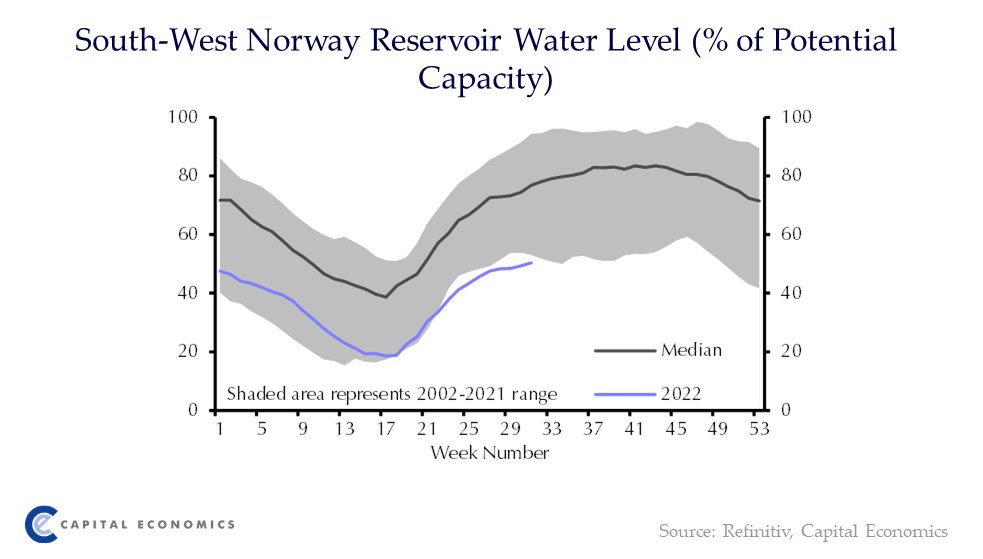

While Norway is not directly in the firing line from the reduction in Russia’s gas exports, it has now got its own problems with low water levels in its hydro reservoirs.

Read more here:

https://t.co/tpcYRNRHam

The biggest problem in Europe’s energy markets is the reduction in Russia’s gas exports. But extreme weather conditions are compounding the problem by making life difficult for nuclear, hydro and coal-fired power plants.

Read more here:

https://t.co/3ehgRkOLOx

The Norges Bank said in June that it was likely to raise its policy rate by 25bp at its meeting next week, but we now think it is more likely to go for a 50bp hike.

Read more here:

https://t.co/ir5H475kO8

We think the euro-zone will soon fall into recession as high inflation, tighter monetary policy and weak global growth take their toll. While the economy should recover next year, the rebound will be held back by a lack of policy support.

Read more here:

https://t.co/9cKKMkGjJ1

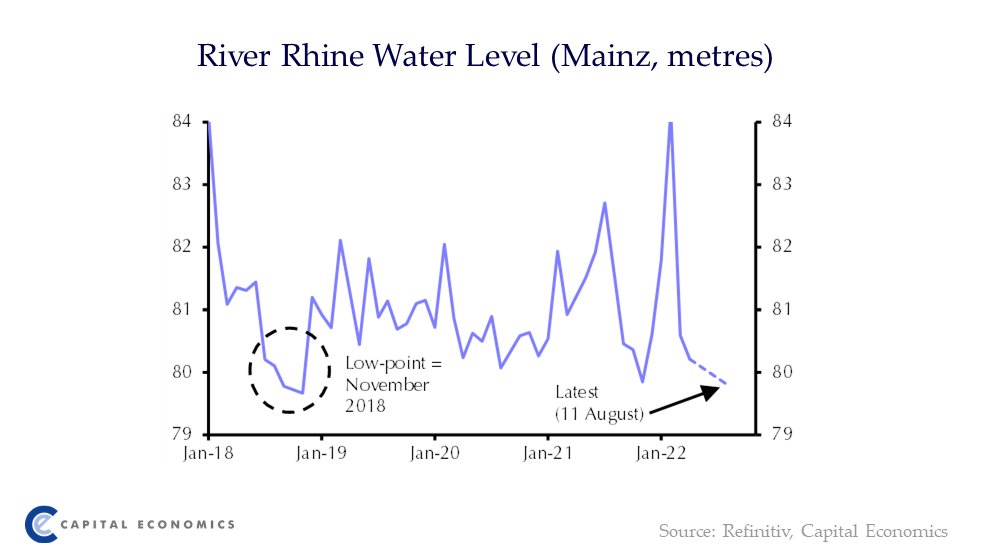

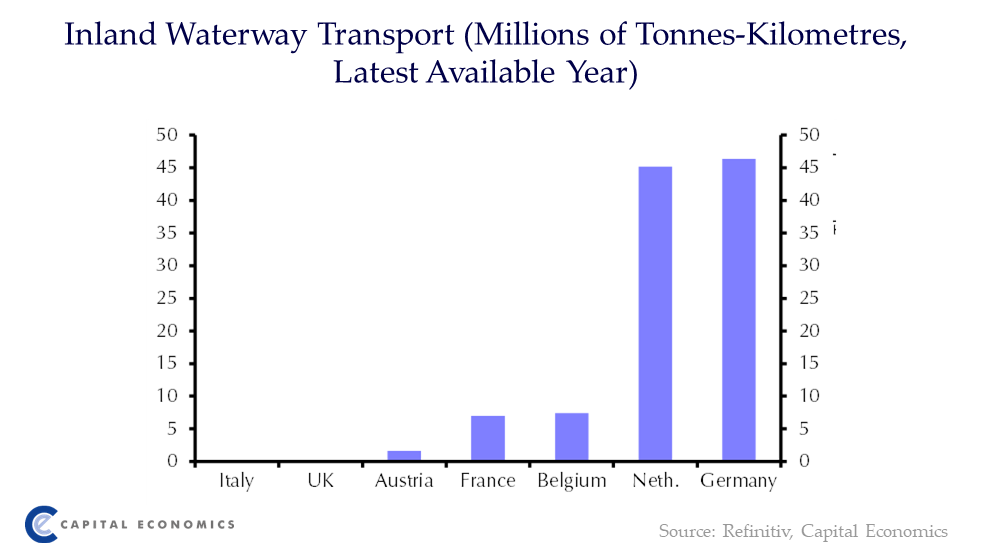

The fall in the Rhine’s water level is a small problem for German industry compared to the gas crisis, or indeed the recent shortage of semiconductors. If it persists until December it could subtract 0.2ppts from GDP in Q3 and Q4.

https://t.co/7VAFG118TW

An end to Russian gas exports to Europe would prompt us to forecast a deeper recession in the euro-zone this winter than we currently anticipate. The hit would come partly through higher inflation and partly through gas rationing.

https://t.co/nvcxsxZgZn

The sharp fall in euro-zone retail sales in June means sales contracted in Q2 as a whole. Final PMI surveys point to price pressures continuing to intensify and demand softening, we think household spending will struggle over the coming months.

https://t.co/MjIQx8VAvC

In June, the number of unemployed people rose in the euro-zone for the first time in 14 months. Nevertheless, we expect the labour market to remain tight even as the economy heads into recession.

Read more here:

https://t.co/Dr8nO63HwY

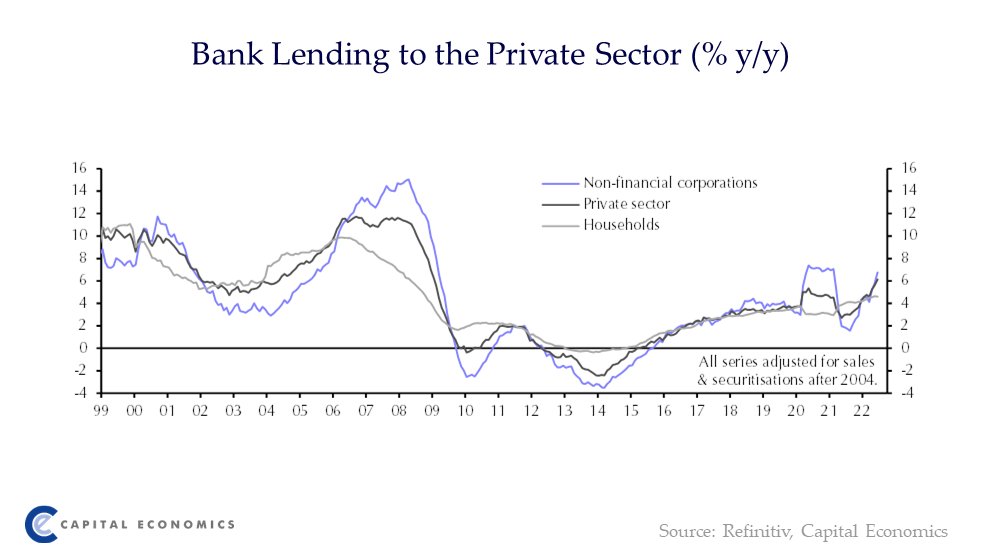

Bank lending growth accelerated further in June, but lenders expect the demand for loans to slow sharply in the coming months, adding to the reasons to expect the economy to fall into recession.

Read more here:

https://t.co/X3Blprll46

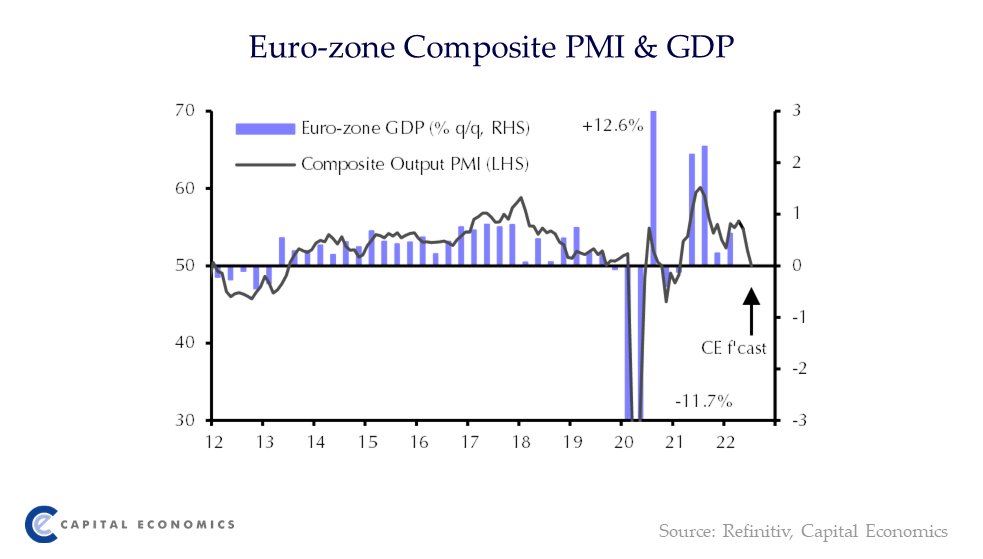

July’s flash PMIs suggest that the euro-zone is teetering on the brink of recession due to slumping demand and rising costs while inflationary pressures remain intense.

https://t.co/pCd9gjBxww

Final inflation data for June confirm that price pressures are very strong. Whether or not the ECB hikes by 50bp on Thursday, we think it will be the beginning of an aggressive 12 months of tightening.

Read more here: https://t.co/W57HALoBXj

Against that backdrop, the ECB is set to raise interest rates by 25bp next week, after which we expect it to step up the pace of tightening and take the deposit rate higher than investors currently anticipate.

Read the Weekly here:

https://t.co/OLqe3XZDKg

If the return of political instability in Italy leads to an early election, government bond spreads are likely to widen, whether or not the ECB agrees the details of the Transmission Protection Mechanism next week. https://t.co/wMfd6L4jQl