Silver $SLV isn't in a bubble like BofA are suggesting.

M2 money supply was $1.6T in 1980.

Today it's around $22.8T.

That's a 14x increase.

So adjusted for the dollars in existence (which is correct because silver is a monetary asset), silver at $62 represents ~1/10th of what the peak silver prices in 1980 were.

And silver demand today is far higher.

And we've in a structural deficit for 4 consecutive years.

But yes, silver prices are in a bubble.

@andrewjclare The Silver M2 Air remains one of the most balanced hardware designs in recent years. It's the sweet spot where thermal efficiency, chassis rigidity, and minimalist aesthetics actually align without the overkill of the Pro lineup. A proper modern classic. 💻✨

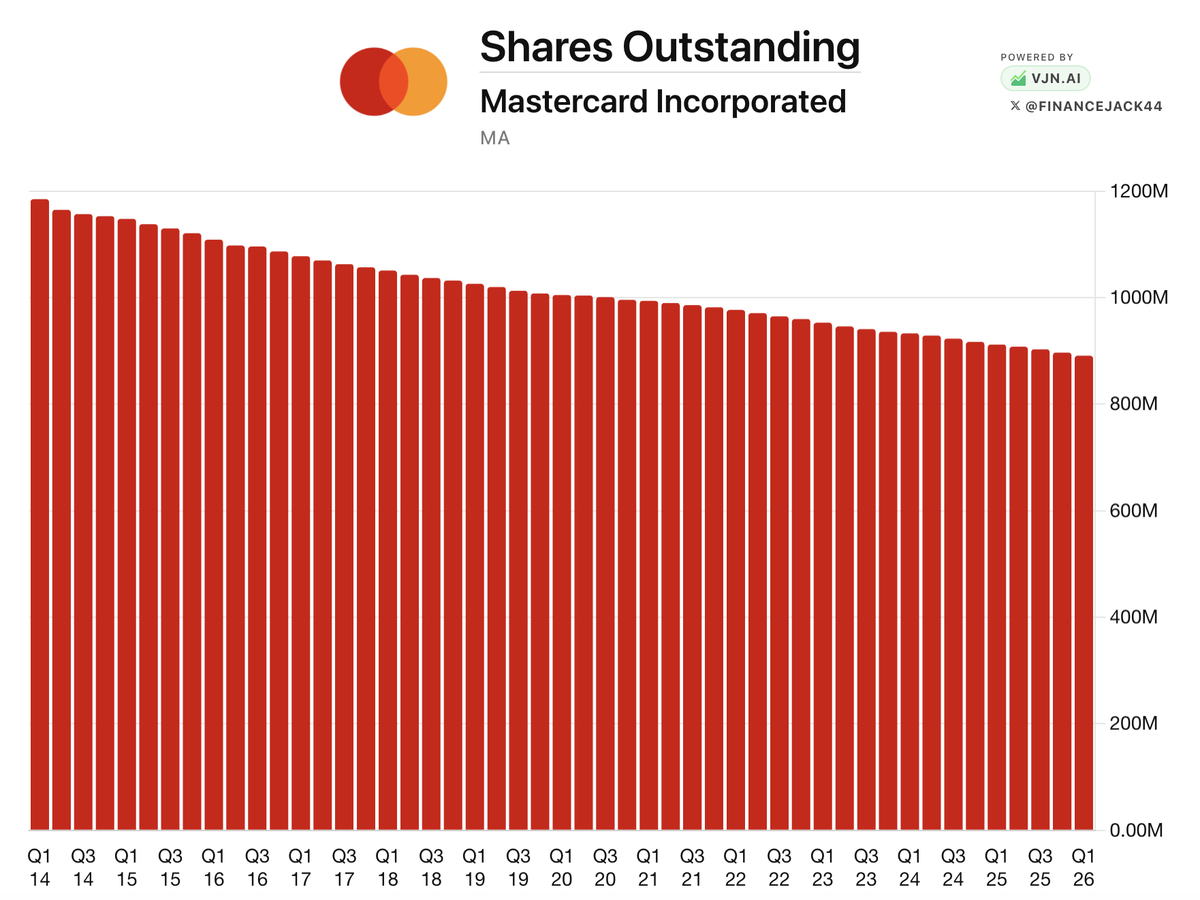

Buyback machines are some of the best stocks you can own. Every single quarter your ownership stake in the business increases without lifting a finger.

Here are 7 companies that have consistently reduced their share count:

1. $MA

What exactly is Jim Chanos saying that is so crazy?

He’s saying that when companies spend billions building AI infrastructure, the supplier books the revenue immediately while the customer depreciates the asset over many years. He’s saying that infrastructure booms can lead to overbuilding. He’s saying that future demand can sometimes get pulled into the present.

None of that strikes me as controversial. In fact, it strikes me as common sense. Long ago I raised the same concern when I first started studying the NeoCloud business model. The moment I saw companies raising huge amounts of capital to buy GPUs and rent them out, I immediately wondered whether we were watching years of future demand being compressed into a very short period of time (see my older posts).

That does not mean $NVDA is doomed, that AI is fake, or that the opportunity is not enormous. What it does mean is that investors should at least think about depreciation and the capex cycle. If you’re analyzing one of the largest infrastructure buildouts in modern history and those risks never cross your mind, you’re missing an important piece of the puzzle.

In fact, I would go a step further. If you do not have a solid understanding of depreciation, how it impacts earnings, and how it affects capital intensive businesses, I would argue you probably do not fully understand what you own. Depreciation is not some obscure accounting footnote. In many industries, it is a major factor between reported earnings and economic reality.

Every boom feels permanent while it is happening. Railroads, internet, teelcom, housing, etc all felt permanent. AI may very well be different, but I don’t think it is unreasonable to ask the question.

The funny thing is that Chanos is being treated like a heretic for pointing out a risk that has existed in almost every major infrastructure cycle in history. You can disagree with his conclusion, but the question itself is perfectly sensible imho.

🌹

Thoughts on $ADBE

$ADBE is one of the most fascinating stocks in the market today because it highlights one of the most important lessons in investing. It continues to execute at a high level. Revenue continues to grow, margins remain exceptional, free cash flow is enormous, and millions of customers still rely on $ADBE products every day. Yet despite all of that, the stock has struggled for years hitting all time lows.

This confuses many investors, especially newer investors. They look at the financial statements and see a business that appears healthy. Then they look at the stock price and assume the market must be making a mistake. After all, if the business is improving and the stock is falling, shouldn’t that create an even better opportunity?

Sometimes the answer is yes. Some of the greatest investments in history occurred because the market became too pessimistic about a business whose future remained bright. But it is important to remember that the market is not trying to value what a company earned previously or even currently. The market is trying to value what that company might earn in the future.

This is where the story becomes interesting. $ADBE looked cheaper at $500 than it did at $600. It looked cheaper at $400 than it did at $500. It looked cheaper at $300 than it did at $400. Many investors looked at the declining valuation and concluded that the opportunity was becoming more attractive. Yet the stock continued to fall because investors were not debating the current business. They were debating what the business might look like in the future.

For decades, $ADBE built one of the strongest moats in software. Photoshop, Illustrator, etc became the standard tools used by creative professionals around the world. Entire careers were built around learning Adobe’s products. Millions of designers, marketers, photographers, and video editors integrated $ADBE into their daily workflow, creating an ecosystem that appeared almost impossible to disrupt.

Then artificial intelligence arrived and changed the conversation. For the first time, images could be generated with a prompt. Videos could be created automatically. Design work that once required years of expertise could suddenly be performed by almost anyone. The question investors began asking was not whether $ADBE remained a great company today. The question was whether $ADBE moat would be as strong five or ten years from now as it was five or ten years ago.

That distinction is incredibly important because stocks are ultimately claims on future cash flows, not current cash flows. Imagine owning a toll bridge that earns $100 million per year. If someone announces that a second bridge will be built beside yours five years from now, the value of your bridge immediately changes even though today’s profits remain exactly the same. Nothing changed in the present, but something changed in the future.

This is why investing can be so difficult. The numbers investors see today often tell a very different story than the future investors are attempting to price. A business can appear healthy while its long term competitive position weakens. At the same time, a business can appear expensive while its future becomes far more valuable than most people realize (ie $PLTR). The market spends surprisingly little time pricing the present and an enormous amount of time attempting to price a future that has not yet happened.

This is also why one of the most dangerous phrases in investing is, “The stock is down but the fundamentals are improving.” Investors have said that about newspapers as the internet emerged, department stores as ecommerce gained share, and cable television as streaming began taking over. In many cases the current business remained healthy long after the future business had already started to deteriorate.

1/2 👇

Charlie Munger: "In my whole adult life, I've never hoarded cash waiting for better conditions. I've just invested in the best things I could find."

"Berkshire has excess cash. Quite a bit of excess cash. But it's not doing that because it thinks it knows how to time investments — [Warren Buffett] just can't find anything he can stand buying."

(Daily Journal AGM || 2022)

You aren't too bullish. Market is choking on the $200B capex headline. Look at Q1 numbers: AWS re-accelerated growth to 28% YoY (~150B run rate), backlog ballooned to $364B, Ads cracked $70B TTM run rate growing 24% YoY, and custom silicon hit a $20B run rate.

It's an asset-heavy moat feeding an ultra-high-margin cash printer. Long $AMZN.

This is the line that matters, so it is worth saying what it means. The 200-day held silver's entire bull for 14 months. Price never closed beneath it the whole way up. So losing it is the structural event, not just a stat.

But "on track for" is a wick, not a close. A line that held a bull for over a year does not break on a touch. It breaks when price closes beneath it, and the weekly close carries more weight than today's candle.

Wicks lie. Closes do not. Today is the test, not the verdict.

Same line we are watching on gold right now. We do not trade the headline. We trade the close.

8개월만에 이혼한 아모레퍼시픽 장녀의 결혼

아모레퍼시픽 서경배 회장의 장녀 서민정과 삼성 홍라희 여사의 조카인 홍정환은 2020년 10월 결혼함

서경배 회장은 결혼 후 사위 홍정환에게 아모레퍼시픽 주식 10만주를 증여했는데 가치로는 63억원 규모였음

그런데 두 사람은 결혼 8개월 만에 합의이혼했고 홍정환이 받았던 주식 10만주도 모두 반환함

불필요한 잡음 없이 받은거 돌려주고 깔끔하게 정리한 느낌이라 정산까지 쿨했던 이혼임

Pinduoduo doesn't own the products it sells. This means it doesn't have to invest capital in inventory and storage, which often plague the traditional retailers. They also leverage third-party logistic providers rather than spending billions on their own fleet. This allows them to scale with a fraction of the capex required by competitors.

Since Pinduoduo collects payments before it pays the suppliers, it benefits from negative working capital also known as a float. As the business grows, its float grows proportionally. The bigger the business becomes, the more capital it generates rather than consumes. This creates a virtuous cycle where growth funds itself and provides excess capital for strategic initiatives.

GLP and the Death of the China Premium

In 2017, when GLP was privatized in a roughly S$16 billion deal of the largest privatization in Asia ever, the logic looked almost irresistible.

The company sat at the intersection of everything investors then liked about China: booming e-commerce, rising consumption, scarce high-quality logistics assets, cheap and abundant capital, and global appetite for infrastructure-like assets with China growth attached.

GLP was not just a warehouse company. It was a bet on the China premium.

The bidding was intense. The winning consortium included some of the biggest names in Chinese capital: Hopu, Hillhouse, Vanke, Bank of China Group Investment, and GLP management. Each brought a different piece of the China story.

Hopu brought elite financial relationships.

Hillhouse brought new-economy investment credibility.

Vanke brought real-estate relevance and operating expertise.

Bank of China Group Investment brought state financial backing.

GLP management brought operational continuity.

On paper, it was the perfect China deal: scarce assets, powerful shareholders, structural growth, and financial engineering.

Almost a decade later, the same company tells a very different story.

The warehouses are still there. The trucks still move. Goods still need storage. GLP is not a fraud, nor is it an empty shell. That is what makes the case interesting.

The asset did not disappear.

The premium did.

Nearly every positive assumption behind the 2017 deal has weakened or reversed.

E-commerce did not vanish, but it matured. The old growth story has turned into brutal platform competition. Tenants are more cost-sensitive and have far more bargaining power.

Modern warehouse space was once scarce. Now it is oversupplied, with landlords competing for tenants.

Consumption was once the great engine. Today Chinese households are cautious. The property crash and lackluster employment damaged household wealth and confidence. Consumers are trading down.

Vanke once represented strategic synergy. Today it represents a shareholder that needs exit cash.

Hopu and Hillhouse once represented elite Chinese private capital. Today they represent the harder reality of China-focused private equity: weak DPI, difficult exits, succession questions, and political risk.

BoCGI once added institutional credibility. Today state financial institutions are more sensitive to real-estate exposure, capital efficiency, regulatory optics and liquidity.

Even political relationships have changed meaning. The same networks that once reassured investors now raise questions about political exposure and regulatory risk.

That is the deeper lesson of GLP.

China did not simply move from growth to low growth. It moved from premium to discount.

In 2017, investors paid for China optionality. They believed growth would solve most problems: debt, supply, execution, exits, and politics.

Today investors demand a discount for each of those same factors.

GLP still has value. The issue is that the market no longer values it using the assumptions of 2017.

GLP today is a complicated exit vehicle wrapped around real assets. Vanke needs balance-sheet relief. Hopu needs distributions. Hillhouse needs exits. Bank of China Group Investment needs to reduce complexity. The company may still list, but the market will ask a simple question: why should new investors pay a premium for an asset old investors are eager to leave?

The old China story was simple: get exposure, wait, and growth will carry you.

The new China story is harder: examine the debt, identify the exit, discount the politics, test the cash flow, and assume that sellers are not doing you a favor.

That is the China story now.

Not collapse everywhere.

Not opportunity everywhere.

Repricing everywhere.

GLP is the death of the China premium in one company: the same warehouses, the same country, the same asset class — but a completely different valuation world.

P4: MARGIN OF SAFETY 🛡️ Despite expecting double digit growth in the next few years, it trades at a forward P/E ~ 10x - 12x. For a company with its growth profile and high ROIC, this is a significant discount compared to western tech peers trading at ~25x - 30x.

Currently, PDD sits on a staggering $60 billion in cash, cash equivalents, and short term investments. With a market capitalization around 140 billion, that means 40% of the company's entire price is backed by cold hard cash. This means on a trailing basis, it trades at a EV/E of ~6.25x.

You are getting double-digit growth and an elite cash-printing engine at a steep structural discount.

$PDD thesis is simple: one of the most efficient, hyper-scaled, capital-light transaction engines in the world, yet it is currently priced by the market as a melting ice cube or a low-quality, cyclical retailer.

They currently operate two businesses