The US should consider spectrum-sharing in the 4GHz band instead of clearing federal users entirely. Shared, flexible licensing could support 5G/6G innovation, protect government operations, reduce costs, and enable localized, AI-driven wireless networks through intelligent coexistence models. https://t.co/OGjZxC0V1n

$ASTS One of the most overlooked details in the AST SpaceMobile thesis is the company stating that BlueBird satellites can operate using four different frequencies simultaneously. I think that completely changes how investors should think about the network architecture. A lot of people originally assumed this would become an exclusive competitive advantage for AT&T and later Verizon, which is why many believed T-Mobile would never be allowed into the ecosystem. But I never really viewed AST as a traditional carrier relationship. I always viewed it more like a tower company. At the end of the day, while the technology is revolutionary, it is still infrastructure. Tower companies do not really care which carrier is paying to use the real estate as long as the infrastructure is monetized efficiently.

That is why I think the recent JV and AT&T’s move into nationwide 600 MHz spectrum may end up being far more important than most people realize. My current theory is that this could evolve into a roaming-style framework where AT&T utilizes Band 71 satellite coverage while leveraging portions of T-Mobile’s terrestrial infrastructure and ecosystem in exchange for T-Mobile joining the AST network. When you combine that idea with AST’s ability to support four frequencies simultaneously, the puzzle pieces start fitting together.

You could theoretically have Band 5 carrying AT&T traffic, Band 13 carrying Verizon traffic, Band 14 supporting FirstNet/public safety communications, and Band 71 extending rural and dead zone coverage for T-Mobile and potentially AT&T all on the same orbital infrastructure layer simultaneously. Maybe Band 12 eventually becomes part of that mix as well. I’m not entirely sure whether Band 13 and Band 14 would technically count as separate simultaneous frequencies from AST’s perspective since they are adjacent 700 MHz spectrum blocks, but the broader point remains the same. BlueBird appears capable of supporting multiple low-band partner spectrum allocations simultaneously.

If that is where this is heading, then the moat may not be exclusive access at all. The moat may actually be the orbital infrastructure itself, the spectrum relationships, the phased array technology, and AST’s ability to dynamically host multiple MNO spectrum bands on the same satellite network at the same time. In my opinion, that would ultimately be much bigger than a single exclusive carrier agreement because once the satellites are in orbit, every additional spectrum tenant dramatically improves the economics of the network.

However this all plays out, it has been amazing putting in the work over the years while so many naysayers called us clueless, only to watch how Farroff many of the so called experts really were.

Cheers Sp🅰️ceMob 🍻

PS I would love some input on what four frequencies you think will end up being the primary and why.

AT&T, T-Mobile and Verizon agree to create a satellite D2D joint venture to fill coverage dead zones and simplify integration with more satellite providers. But plenty of details are still lacking.

Read more on Light Reading: https://t.co/lsy0Hge0lU

SpaceX may only be doing $15-$16B in annual revenue today, while aiming for a $2T IPO, and most people will look at that and say, “That valuation makes no sense... it's overvalued.”

But to me, this company is still SIGNIFICANTLY undervalued.

SpaceX owns the launch system.

It owns the satellite network.

It owns Starlink.

It owns the path to orbital AI compute.

And with Starship, it will become the lowest-cost access to space in human history.

And honestly, this is why I think I’m going to become the first billionaire in my family tree.

Not because I got lucky... but because I saw this before almost anyone I knew did.

I did my homework.

I understood from day 1 that SpaceX wasn’t just launching rockets, it was building the operating system for space.

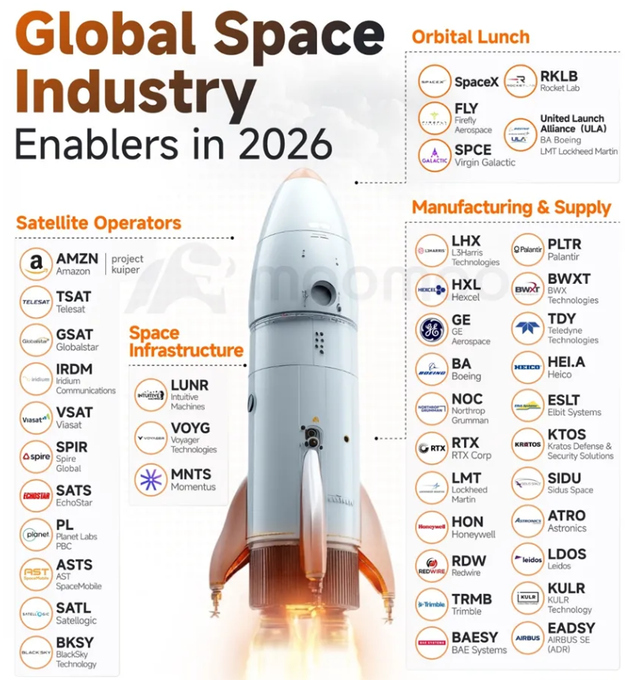

2026 WILL BE THE SUMMER OF SPACE

SpaceX now has a 92% implied chance of going public this summer which could become the forcing function for the space trade.

A rumored $2T valuation, Golden Dome & rising demand across launch, satellites & defense infrastructure are pushing investors to look beyond SpaceX & into the full space supply chain:

Orbital Launch (access to space)

• $FLY, $SPCE, $ULA add exposure across lunar, research & heavy-launch mission profiles

• SpaceX remains foundation of the ecosystem with Starship driving lower cost-per-kilogram economics & Golden Dome further validating the national-security demand layer

• $RKLB provides dedicated launch & integrated space services for small & mid-sized missions backed by its $805M SDA Tracking Layer contract, ~$1.9B backlog, Neutron roadmap & SHIELD eligibility

Satellite Operators (demand layer)

• $PL, $BKSY capture earth observation & defense intelligence demand

• $VSAT, $SPIR, $SATL, $TSAT support aviation, maritime, spectrum & specialized communications

• $AMZN Leo builds broadband & D2D layer with Globalstar spectrum, $AAPL satellite services and customers like Delta, AT&T, Vodafone & NASA

• $ASTS building space-based cellular broadband with carrier partnerships across AT&T, Verizon & Vodafone, $1.2B in contracted 2027 revenue & BlueBird constellation expansion

Space Infrastructure (on-orbit systems & services)

• $MNTS sits in orbital transport & in-space logistics

• $LUNR owns lunar & deep-space mission infrastructure

• $VOYG anchors commercial space station transition through Starlab backed by partners like $PLTR & Airbus

• $RDW supplies key space infrastructure components including solar arrays, payload facilities, robotics & in-space manufacturing systems

Manufacturing & Supply (industrial backbone)

• $KTOS, Anduril sit at intersection of autonomous defense, missile defense & space-enabled systems

• $BWXT brings nuclear exposure across space power, defense systems & broader nuclear renaissance

• $LMT, $NOC, $RTX, $BA anchor defense prime layer across spacecraft, launch systems & national-security platforms

• $LHX, $TDY, $HON supply sensors, avionics & mission-critical hardware needed across defense space programs

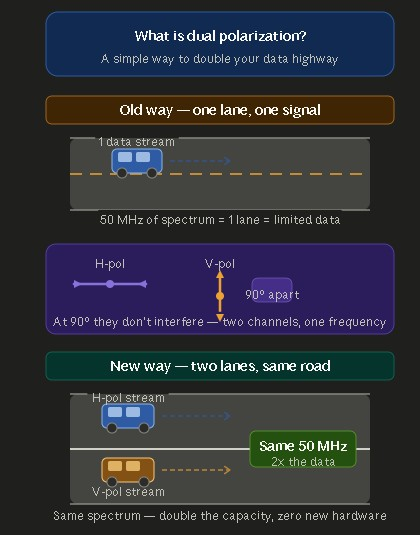

$ASTS: 🚨 AST SPACEMOBILE FILES NEW PATENT APPLICATION FOR POLARIZED-TRANSPARENT CHANNEL SWITCHING, POTENTIALLY BOOSTING DATA CAPACITY BY 3X TO 10X

AST SpaceMobile BlueBird satellites dual polarized phased array can transmit both horizontal and vertical radio frequency waves simultaneously, which creates two independent data channels within the same band of spectrum to an unmodified phone.

The benefits are:

1) Massive Boost in Spectral Efficiency

2) Constant Peak Signal Strength

3) Reduced Dropped Packet Latency

4) Improved Efficiency of the Phase Array

AI-optimization on a BlueBird satellite manages all the switching invisibly and seamlessly. Abel has referred to performance increases of 3x near term to potentially 10x longer term. Plainly, this means 50MHz of spectrum capacity when leveraged through an AST SpaceMobile BlueBird satellite can act like 150MHz up to 500MHz.

Starlink phased arrays feature circular polarization and are unable to do this optimization.

credit: @intalia51

PASSED: FCC Modernizes Satellite Spectrum Sharing Rules to Boost Broadband 🛰️

“With today’s decision, consumers could now see a 7X INCREASE in capacity for these high-speed, satellite offerings.” - Chairman @BrendanCarrFCC 🧵⬇️

$ASTS This SES possible partnership plus the FCC enabling SCS beyond land in international waters is sneaky big and makes me wonder. With AST’s current infrastructure the network could realistically reach close to 90% of maritime traffic. Most global shipping lanes sit within range of land based gateways.

Wonder how $VSAT is feeling 😳

Love seeing the small fish turn into big fish. Massive disruption happening right in front of our eyes.

Below you can see the SES infrastructure and AST Bluebird field of view. This setup should be able to cover most major shipping lanes.

🚨🚨 Blue Origin - FCC Docket SAT-LOA-20260310-00118

NASA submitted comments to the FCC regarding Blue Origin's "Project Sunrise" application to deploy approximately 51,600 satellites in Low Earth Orbit (LEO) at altitudes between 500 km and 1,800 km. While supporting commercial innovation, NASA emphasizes that the constellation's scale raises significant safety and sustainability concerns for its human spaceflight and science missions.

🔗 https://t.co/HYqsCT1Dov

How Space Data Centers Work?

Orbital AI superclusters running on unlimited solar power and natural vacuum cooling.

1. Orbital Deployment & Launch

Rockets and satellites delivering compute nodes into low-Earth orbit.

Tickers: $RKLB · $RDW · $LUNR · $PL

2. Power Systems (Solar + Energy Management)

Massive solar arrays harvesting constant sunlight with advanced power distribution.

Tickers: $NVDA · $GOOGL · $PL · $RKLB

3. Thermal & Cooling Management

Passive radiation cooling in the vacuum of space — no fans or chillers needed.

Tickers: $NVDA · $AMD · $HPE · $RDW

4. Compute Hardware & AI Integration

Radiation-hardened GPUs, TPUs, and onboard AI processing clusters.

Tickers: $NVDA · $AMD · $GOOGL · $HPE

5. Data Connectivity & Networking

Laser inter-satellite links and high-speed downlink to ground stations.

Tickers: $ASTS · $VSAT · $IRDM · $RKLB

Space data centers are floating AI superclusters — solving Earth’s power, cooling, and land limits by moving compute into orbit.

That’s why leaders in launch, hardware, and space infrastructure $NVDA, $RKLB, $ASTS, $GOOGL, SpaceX are positioned as the next wave of AI winners.