It's almost TIME to buy BIGGER. But not yet.

Here's the advanced technical breakdown of what we will do together for $SPY and $QQQ.

My portfolio is DOWN -1% from the top.

We are SURVIVING and have reduced our volatility significantly together.

We are 40% in AI and 60% outside of AI (defensives, laggards, hedges, cash).

But the markets are getting to better levels very soon.

We plan to KEEP buying slowly and slowly every day.

No RUSH on our end.

Remember, if $SPY goes down -1%, I do NOT want to go down -5%, or -10%. My goal is to stay CLOSE to the $SPY and $QQQ during red days.

We stay STABLE during big red days. We OUTPERFORM during green days.

Let's go. 💪

@babyfolio I see the same thing within my big tech company. my org partners crossfunctionally with other business departments and they use chat bots everyday. Agentic AI is being pushed everywhere

For people out there citing Bank of America quotes now about selling.

Just remember:

They said $EWY/ KOSPI (SK Hynix/Samsung) was an extreme bubble back in March.

And blamed retail for the cause, then implied they should sell Korean memory equities: comparing it to the 2008 financial crisis, .com bubble, and Silver crash.

Then shortly after retail sold their longs, memory rallied to all time highs.

Institutions are not your friends.

Usually when an unusual flood of negative news, they need liquidity.

$MU GS: We now expect 2027 S/D for conventional DRAM, NAND, and HBM to be all tighter than 2026 and the tightness to extend into 2028, which should help the memory companies to see an elevated level of earnings power for at least the next few years.

This is a really interesting paper about stock performance.

If you bought $AMD at the close every day and sold at the open the next day, over decades you’d have gotten a whopping +4,555,517% return.

But if you bought at the open every day and sold at the close the same day, you’d have lost almost everything – down -99.94%.

This pattern holds across every major market globally. This just reiterates that time IN the market beats anything else.

Other examples:

$MU: overnight +138,330,342% – intraday -99.92%

$NVDA: overnight +221,715% – intraday -99.7%

Same stocks. Completely opposite outcomes depending on when you hold it, overnight risk premium pays, intra day trading doesn’t.

UBS global research just put numbers on AI data center power semis.

Here's a list of tickers they named specifically

> Leaders: Infineon $IFX (Buy), $TXN

> Incumbents: Renesas 6723.T, $ADI

> Power stages / VRM: Monolithic $MPWR, Vicor $VICR

> Wide band gap on the 800V shift: $NVTS, $STM, ROHM 6963.T, $ON

> Smaller / laggard exposure: $POWI , $DIOD, $AOSL

> PSU system level: Delta https://t.co/m1ww5mzgHD, Lite-On https://t.co/qN6lOAY0EA

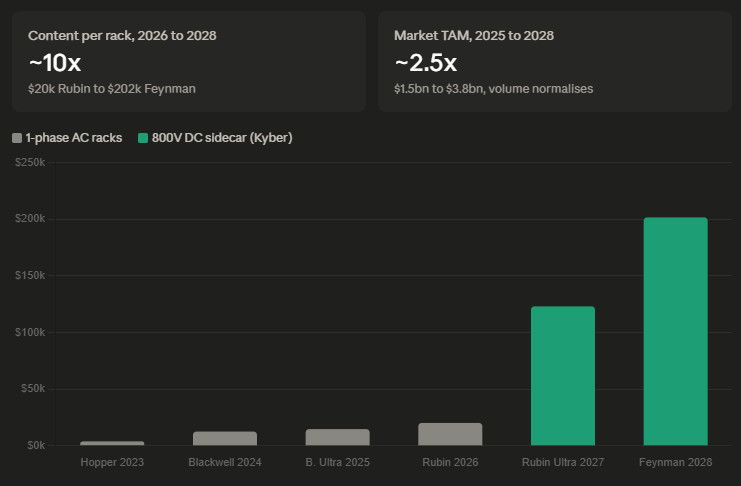

Content per rack is exploding:

Hopper 23': $3.9k

Blackwell 24': $12.6k

Rubin 26': $20.2k

Rubin Ultra 27': $123k

Feynman 28': $202k

50x (FIFTY) in 5 years. Driver is the 800V DC shift forcing GaN/SiC across the stack, not unit volume.

But UBS's own model implies 30GW+ of 2026 capacity adds vs 10-15GW consensus.

Infineon's guide alone implies 40GW+. That is double.

They predict the TAM $1.5BN 25' will jump to $3.8BN by 28'

So chat, are there any power-semi plays not listed that you recommend I take a look at?

$CRDO - Credo earnings are out of the way and the stock is forming a flag after breaking out of a 6-month base.

Under the hood, it's showing a lot of relative strength.

As AI clusters get larger, the need for faster connectivity only increases - and that's exactly where Credo plays.

I've just discovered that the $ELMT founder holds 36% of the company.

On June 3, $ELMT released a 13G/A revealing that CEO Peter Anania and his entities still hold 10,803,122 of 29,979,863 shares.

$ELMT makes refractory metals - tungsten, molybdenum, niobium, tantalum - and the RF/microwave systems that go into defense and semiconductors. Q1 revenue grew 20.7% to $56M on a record $113.3M backlog.

In April it priced just 8.6M shares at $14. Anania took 29% of the company to market. The rest was held by him and added by institutions.

Having this founder stake is crucial. That stake is $360M of founder-aligned stock marked to the share price every single day. With more than a third of the company's equity, the CEO's personal wealth rises and falls directly with the share price. They are highly incentivized to grow the business rather than just collect a salary.

A 36% lock also means the tradable float is far smaller than the 30M share count implies. That's the mechanical reason ELMT swings 18% on a single backlog print. Thin float cuts both ways.

So, you're not just buying refractory-metal exposure into a rising defense-capex cycle. You're buying it next to an owner-operator who floated the smallest slice he could and bet the rest on himself.

When a founder-led company bets on itself, I will always take interest.

When it acts as a key supplier for Defence, Semiconductors, Space, Rare earths,Nuclear fusion, etc, I buy.

$ELMT