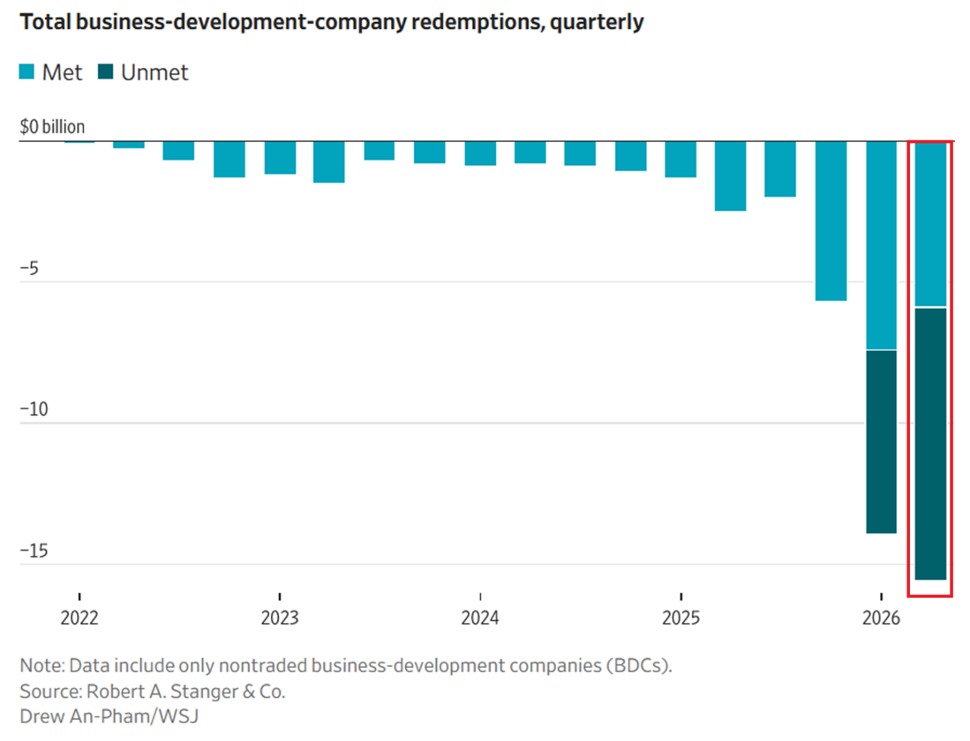

Stress in the US private credit market is intensifying:

Investors requested a record -$15.6 billion in redemptions from private credit funds in Q2 2026.

This marks the 3rd consecutive quarterly increase by a total of +$13 billion, or +500%.

Furthermore, just 38% of these requests were met, down from 53% in Q1 2026, leaving $9.7 billion in unmet redemptions, the largest backlog on record.

Blue Owl's flagship fund, Blue Owl Credit Income, was the most impacted at 19% of shares outstanding, with 14% unmet, the highest redemption rate among its large competitors.

This was followed by Apollo, at 16% requested with 11% unmet, and Ares, at 14% requested with 9% unmet.

Meanwhile, inflows into the private credit industry declined -75% since January to ~$500 million in May, the smallest monthly intake in at least 18 months.

The private credit crisis shows no signs of slowing.

🇨🇳 🇪🇺 🚗 Chinese cars have just crossed a symbolic threshold in Europe as for the first time, they accounted for more than one in ten new car purchases last month ⚠

➡️ This figure matters much more than it may seem because it points to a deeper shift in the balance of power within the European auto industry. For a long time, the Chinese threat was mostly framed as competition in fully electric vehicles. In reality, Chinese automakers are now attacking an even more strategic segment: hybrids and plug-in hybrids, exactly where a large part of European demand currently sits.

🇪🇺 European consumers are not yet fully ready to switch massively to electric vehicles because prices remain high, charging infrastructure is still imperfect, and many buyers still want the reassurance of a combustion engine. Chinese brands understood this very quickly and instead of pushing only electric cars, they are entering the market with hybrid SUVs that are well-equipped, modern, powerful and, above all, highly competitive on price.

⚠️ The issue becomes problematic for Volkswagen, Stellantis, Renault and BMW as they have long protected their margins through premiumisation, options, SUVs and brand strength. However, if a customer can buy a better-equipped Chinese model at a lower price than a comparable European vehicle, the pricing power of legacy manufacturers starts to weaken. Therefore, there is a direct pressure on prices and margins.

🤷♂️ Moreover, the EU tariffs introduced since 2024 mainly target fully electric vehicles made in China. Hybrids remain less affected, creating a window of opportunity for Chinese manufacturers. If Europe taxes electric cars, China accelerate on hybrids, and even if Brussels decides to extend tariffs, that will not solve everything, because several Chinese brands are already looking to manufacture directly in Europe.

China simply adapted its strategy and have found the right angle of attack 🚨

*Bloomberg link: https://t.co/nrxqHrlpLS

The market is dropping in response to the Fed's first meeting with Kevin Warsh as Fed Chair for one key reason:

We will have far less information going forward.

During the press conference today, Fed Chair Warsh announced that the Fed has "dropped" forward guidance.

He even hinted that the "dot plot" could be changed or eliminated along with all forms of Fed communication, such as the policy statement and press conferences.

In other words, the market will now have less Fed outlook which means more uncertainty.

On top of this, the five new "task forces" established by Warsh were said to have grand objectives with minimal guidance on what to expect.

As markets have repeatedly proven, uncertainty and volatility go hand-in-hand.

The new era of Fed policy will come with more volatility.

Market leverage in Asian markets is through the roof:

Assets under management (AUM) in leveraged South Korean and Taiwanese ETFs are up to a record $65 billion.

Since the start of 2026, total leveraged ETF AUM has surged +490%.

This comes as 16 new single-stock leveraged ETFs tied to Samsung and SK Hynix were launched in South Korea two weeks ago.

By comparison, AUM in US leveraged ETFs stands near a record ~$180 billion.

Meanwhile, the SK Hynix 2x long Leveraged ETF surged +50% on Monday despite a -7.7% decline in SK Hynix shares, posting a rare divergence.

This fund should have declined -15% under normal tracking conditions.

Other single-stock leveraged ETFs tracking SK Hynix ended the session within normal ranges.

Investors are taking on more leverage than at any point in history.

FUN FACT

THE ONTARIO TEACHERS’ PENSION PLAN INVESTED $300 MILLION INTO SPACEX IN 2019

THAT STAKE IS NOW WORTH $16 BILLION

NEARLY A 5,200% RETURN IN 7 YEARS

THIS MAY GO DOWN AS ONE OF THE BEST INVESTMENTS EVER MADE BY A CANADIAN PENSION FUND

🇨🇦🇨🇦🇨🇦

BREAKING: President Trump says the Trump Administration might buy equity stakes in US AI companies and that he will host a meeting with AI executives as soon as next week, per Reuters.

Imagine you spent 40 years doing the boring, responsible thing.

You opened a 401k at 23. You contributed every paycheck. You ignored the noise. You bought the index because Bogle told you to, because Buffett told you to, because every honest piece of financial advice for 30 years told you the index was the safest, most diversified, most rules-based way to own America.

The whole point was the rules.

The rules said: a company must trade for 12 months before joining the S&P 500. The rules said: it must show four consecutive quarters of GAAP profitability. The rules existed because in 1999 the index quietly bought a lot of stocks at the top, and pensioners paid the bill.

After the dot-com crash, S&P tightened the rules. Nasdaq tightened the rules. FTSE Russell tightened the rules.

For 23 years, those rules held.

Then SpaceX filed for IPO.

And the rules changed.

The S&P 500 waived the profitability requirement. Nasdaq cut its trading-history window from 90 days to 15. FTSE Russell cut its to 5.

Bloomberg Intelligence estimates the major index funds will absorb between 19% and 24% of SpaceX's float within six months. That's over $30 trillion of passive 401k and retirement money, mechanically buying a single newly public company at IPO valuations, because the rules said they had to.

Except the rules used to say they didn't.

Here's the thought exercise:

If you spend 40 years building a system designed to protect ordinary savers from buying overpriced stocks, and then you waive the protections the moment a sufficiently large stock asks you to, what was the system actually protecting?

Most of investing is about understanding what's a rule and what's a guideline.

A rule binds the rule-maker.

A guideline binds the saver.

You're allowed to find out which is which only after the fact.

AN “UNKNOWN” COMPANY ACCIDENTALLY SPENT $500 MILLION DOLLARS IN 1 SINGLE MONTH ON ANTHROPIC’S AI TOOLS AFTER FORGETTING TO SET LIMITS FOR THEIR EMPLOYEES

𝐓𝐡𝐫𝐞𝐞 𝐋𝐚𝐲𝐞𝐫𝐬. 𝐎𝐧𝐞 𝐂𝐨𝐦𝐩𝐨𝐮𝐧𝐝𝐢𝐧𝐠 𝐀𝐝𝐯𝐚𝐧𝐭𝐚𝐠𝐞. 𝐓𝐡𝐞 𝐈𝐑𝐄𝐍 𝐓𝐡𝐞𝐬𝐢𝐬.

There's been a lot happening at IREN recently.

Expansion across North America, Europe and Asia-Pacific.

The NVIDIA partnership.

The Mirantis acquisition.

New GPU deployments.

New customer discussions.

A growing global footprint.

Underneath all of it is a fairly simple view of where the world is heading, and a deliberate strategy for how we position IREN within it.

That strategy is built on three layers. Together, they compound into a structural advantage that gets harder to replicate every quarter we execute.

Layer 1: Physical infrastructure. Power, land, substations, data centers, cooling. The foundation that everything else sits on.

Layer 2: Compute infrastructure. The GPUs, servers and networking that go inside those buildings. Deployed at scale. Generating revenue. Building execution track record.

Layer 3: Software and operational capability. The orchestration, deployment tooling and enterprise expertise that makes the first two layers work harder for customers, and opens the door to a broader, higher-value market over time.

Layers 1 and 2 are where the overwhelming majority of IREN's value is being created today. Layer 3 is where that advantage compounds further over time, but only because Layers 1 and 2 are built, owned and controlled at scale by IREN, not subscale nor contracted from a third party.

Think of Amazon. They didn't win e-commerce by building a great website. They won it by controlling the fulfilment infrastructure at a scale nobody else could replicate. The foundation you don't control becomes the ceiling on your business.

That is exactly how we think about IREN. The physical infrastructure - the land, the power, the substations, the data centers - is owned and controlled by us. The compute deployed into it generates the revenue and execution track record. And the software, orchestration and enterprise capability we are more methodically building on top is what turns the total product into a vertically integrated AI Cloud platform that compounds over time and deepens into a competitive moat.

AI is still early. The bottleneck is increasingly physical. And we have spent eight years building the foundations.