$IREN

Holy declining exahash Batman!

Significant decline in exahash over the last 10 days or so - is IREN really disconnecting this many miners?

Rough math - 12.5 EH/s = ~200MW of capacity.

What is going on?!

👀

$IREN: The cloud market's dark horse

I bet most $IREN bulls are starting to get increasingly exhausted by the price action. I certainly am.

However, as long-term investors, we should see day-to-day price action as nothing more than noise.

$IREN is particularly "noisy," which makes it an especially difficult hold. Yet in times like these, it's important to step back and refocus on the company's fundamentals rather than let price action sway one's emotions.

And the way I see it, $IREN's competitive standing is rapidly improving.

I recently came across an interesting research report by Goldman Sachs that highlighted the discrepancy between planned data center capacity and realized capacity.

Out of the ~18 GW planned to be commissioned over the past 6 quarters, only about ~11 GW actually got built.

Not only is the gap between planned and realized capacity rapidly widening, but the rate at which new capacity is coming online has actually declined over the past couple of quarters.

Much of this discrepancy comes down to power continuing to be a major bottleneck.

As grids get more and more constrained with lead times reaching 5+ years, many developers are moving toward behind-the-meter (BTM) generation (on site power generation), circumventing the need for grid connectivity.

Yet that comes with its own set of problems and bottlenecks. The end result is an increasing amount of delays and outright project cancellations.

This industry backdrop plays directly into the hands of $IREN, which now has 5.8 GW of secured grid-connected power across global jurisdictions.

The only reason the industry is switching toward BTM is that it's the only option if you don't want to wait in multi-year queues to secure grid connections. But don't get it twisted, grid-connected power remains the preferred option.

$IREN is in a unique position to capitalize on this structural bottleneck and become one of the few cloud providers that can actually bring on 5+ GW of compute capacity over the coming years.

I'd even go as far as saying that this structural advantage is the primary reason the $NVDA partnership came to be.

While $NVDA undoubtedly remains king of the hill, even they face a real dilemma that could cause cracks in their growth trajectory.

On the supply side, they have to come to terms with the fact that the gap between planned and realized data center capacity is widening, while the trend of new capacity coming online is actually decelerating.

This is the issue I just flagged, and it could act as a potential growth bottleneck for $NVDA, since fewer builds means fewer GPU sales.

Layered on top of this is the demand side. It's perfectly clear that demand for $NVDA's AI hardware remains insatiable. However, when looking closer, it's also apparent that competition is increasing.

Pretty much every hyperscaler is working on their custom chips (TPU, Trainium, Maia, MTIA), and not exclusively for internal use cases anymore, but increasingly to service the compute needs of large AI labs. Anthropic alone has signed deals worth billions for Google TPU and AWS Trainium capacity.

Then you obviously have the likes of AMD and Cerebras directly competing against the AI giant, trying to claim market share.

Taken in aggregate, these two issues could gradually lead to a growth problem for $NVDA if not addressed.

This is exactly where $IREN comes in.

They've got the largest secured power portfolio of any neo-cloud at 5.8 GW and growing fast, they develop 100% of their data centers themselves, and they're not building competing silicon.

That makes them the most reliable demand outlet $NVDA can partner with at scale.

The Sweetwater partnership, positioning the 2 GW campus as a "flagship DSX deployment," isn't $NVDA doing $IREN a favor. It's $NVDA solving its two biggest problems at once.

I'm sure you know the popular saying that "history never repeats, but often rhymes." I think today's neo-cloud market is somewhat similar to the dot com era search engine war.

Back then, the front-runners leading the race were AltaVista, Excite, and Yahoo, while Google was a latecomer that ultimately came out on top.

Today, the vast majority of investors in this space are declaring either $CRWV or $NBIS the obvious winners in the race to become the next hyperscaler.

However, I believe the real dark horse that the mainstream doesn't give much credit to is $IREN.

I believe they have all the ingredients to leapfrog every competitor in a short amount of time, in large part due to their structural advantages and pursuing the right long-term strategy from the get go.

The asset-light model, which both $CRWV and $NBIS have been leaning into, doesn't work well in capital-intensive industries, at least not over the long run.

It's somewhat of an oxymoron, since it seems intuitive that one way to circumvent some of the CapEx burden is to outsource from colocation providers.

Yet that approach leaves you with less control, less flexibility, and ultimately higher costs in aggregate in the form of operating expenses (the landlord also has to earn $).

I studied the Bitcoin mining industry for years, and the asset-light model was once a popular strategy around the 2021 bull market. While it proved to be a strong growth lever, it ultimately ended up being a disaster for anyone who adopted it.

Companies like $MARA are the perfect example.

$MARA heavily adopted the asset-light model and grew to become the largest $BTC miner, yet ended up as one of the most unprofitable public miners of all, leading to significant value destruction for shareholders over time.

Once it became obvious that asset-light wasn't a sustainable strategy, $MARA tried to pivot away from it by increasing self-deployments. But developing infrastructure in-house is a much harder discipline to master, and you don't simply switch into it overnight.

$IREN ultimately won the mining race last cycle by doing the exact opposite of $MARA from the start.

They developed all of their data center infrastructure in-house, backed by a seemingly unlimited pipeline of secured power, which ended up making them the fastest growing and most profitable miner of all time.

While the cloud sector has significant differences from the mining industry, the primary drawbacks of the asset-light model carry over.

Over time, it will become obvious to Wall Street and the broader market that this strategy sounds great in theory, but in practice leads to a stack of operational issues and severe margin compression.

Out of the two current front-runners, $CRWV and $NBIS, I think Nebius will do better. They've at least started moving toward a more diversified mix of self-owned capacity rather than purely relying on hosted colocation, which is the right direction even if they're still early in that pivot.

That said, as the $MARA example showed, developing in-house gigawatt projects at scale is not something you learn overnight.

It's clear to me that a player like $IREN, which has been building this discipline from day one, has the most realistic pathway toward sustained, profitable growth in this space.

In my view, $IREN is the dark horse that will end up winning the race. Thus overthinking today’s price action wouldn't do me any favors.

Cheers guys, have a great weekend! ✌️

$IREN

AFR article covering the new 800MW datacenter site in South Australia.

"Roberts said Iren had started talking to potential customers including big US cloud services companies and large language model owners."

Anthropic anyone? 😎🔥

$IREN — The Enormous Significance of DSX Air That the Market Has Overlooked

Today there are two major pieces of news about IREN — one on the capital side and one on the technical side — both highly significant.

On the capital front, IREN completed the first investment-grade GPU financing with the highest public rating ever seen in the U.S. private market.

On the technical front, IREN is working with NVIDIA to build AI infrastructure compatible with NVIDIA DSX across its global data center network. The linked NVIDIA page carries a detailed report titled “NVIDIA DSX: Action Guide for Infrastructure Builders to Construct AI Factories.”

At the same time, following Jensen Huang’s comments at the Taipei GTC on CoreWeave (CRWV) and Nebius (NBIS), those two stocks traded higher in pre-market, while IREN’s stock remained weak.

There is also a more detailed technical update: “IREN and BE Networks Accelerate Deployment of Large-Scale AI Factory with NVIDIA DSX Air.” BE Networks is a leading software solutions provider specializing in hyper-automation, lifecycle management, and monitoring for next-generation GenAI, core data centers, and multi-vendor edge infrastructure.

From a forward-looking perspective, IREN’s progress today represents major strategic steps — especially its collaboration with BE Networks to use NVIDIA DSX Air to speed up large-scale AI factory deployment. This is concrete proof of strong execution. If CRWV and NBIS rallied today because they secured priority access to Vera Rubin, what IREN is doing is far more consequential.

Here’s a simple analogy:

Imagine Vera Rubin as a brand-new aircraft engine. CRWV and NBIS have won priority delivery of the next-generation jet engine. IREN, by contrast, is helping establish the manufacturing standards and production system for the next-generation aircraft.

What IREN is actually doing

It is building a complete testing, tuning, and mass-deployment system tailored for this new engine. Before large-scale production begins, the team is validating every aspect of the engine’s behavior — aerodynamics, structural integrity, vibration, and failure modes — inside a full digital twin environment. From there, it is creating repeatable, standardized deployment processes so that future massive clusters can be deployed and optimized in days instead of months.

Why does this matter more?

Securing a newly designed engine and knowing how to extract maximum performance from it while scaling that capability reliably are two entirely different orders of magnitude. Today IREN is using NVIDIA Blackwell Ultra GPUs to do exactly this work. The market has shown almost no awareness of its importance. Investors cheered for Vera Rubin, yet failed to notice that IREN and BE Networks are already using DSX Air to create a digital twin that simulates the future deployment of 50,000+ Blackwell Ultra GPU clusters.

The scope of testing goes far beyond the GPUs themselves. It covers the entire AI Factory stack:

Spectrum-X networking

NVLink networking

Storage systems

Orchestration platforms

Security architecture

Automated operations and maintenance workflows

Power and cooling integration validation

DSX was designed from the start for the Rubin era. Even though Vera Rubin has not yet entered volume production, the DSX Air testing system — built to enable rapid, large-scale deployment — is already running. The current validation work on Blackwell Ultra is not primarily about Blackwell itself. It is a full dress rehearsal for the Rubin era.

What truly needs to be validated, hardened, and refined in advance is not the GPU model. It is the construction methodology for future AI factories. In the DSX framework, several foundational principles will not change with new GPU generations: network topology principles, automated deployment methods, operations frameworks, and digital twin processes. The only things that will change are component-level variables — GPU models, switch types, rack power density, and cooling parameters.

The aviation industry offers an almost identical precedent. Boeing does not wait until the 787 enters full production before certifying its manufacturing system. It uses early prototypes to validate processes, supply chains, and assembly procedures. By the time the production aircraft arrives, the entire system is already mature — the plane is simply the final component inserted into an already-proven production line.

Viewed through this lens, CRWV and NBIS have secured priority delivery of the Rubin “aircraft.” Their advantage is being first in line to receive it. IREN is validating the production line for Rubin aircraft ahead of time.

Although the hardware being tested today is Blackwell Ultra, what DSX Air is really training are the engineering teams, automation capabilities, network design expertise, and large-scale cluster operations skills. These capabilities will transfer seamlessly to Rubin. The announcement’s reference to “simulating and validating 50,000+ Blackwell Ultra GPU deployment” carries meaning well beyond the literal words. If the goal were simply to deploy Blackwell, such an elaborate digital twin would not be necessary — Blackwell already exists and can be tested in real environments. Digital twins become essential when scale is enormous, costs are extremely high, and the next-generation architecture is about to arrive. That is precisely the situation in the Rubin era.

A more accurate way to understand it: DSX Air is not testing Blackwell Ultra — it is conducting an advance rehearsal for Rubin.

So why has the market shown almost no reaction to something this important, while giving all the applause to priority access for Vera Rubin?

Jensen Huang’s remarks at GTC actually told two completely different stories. From NVIDIA’s sales perspective, CoreWeave and Nebius represent classic “proof of demand.” To successfully launch Rubin, NVIDIA needs investors and customers to believe there are already committed buyers. That is why names like CoreWeave, Nebius, AWS, Microsoft, and Google naturally take center stage — they serve as visible evidence that “the product has already been sold.”

IREN plays a completely different role. It is working side-by-side with NVIDIA to design the next-generation super factory. This role is equally critical, but it belongs to a different stage of the value chain.From NVIDIA’s longer-term viewpoint, the real scarcity in the coming years will not be GPUs. It will be power, land, high-voltage grid connections, liquid cooling capacity, network deployment expertise, and the ability to deliver complete AI factories. These infrastructure elements have much longer lead times than chips. In the joint NVIDIA-IREN announcements, the repeated emphasis is not on GPUs but on power, land, data centers, and infrastructure operations. This shows that the partnership was never primarily about buying and selling GPUs — it has always been about jointly building the AI factory ecosystem.

IREN has now entered the verification and deployment phase of the NVIDIA DSX ecosystem. The significance of this step far exceeds what the market currently appreciates. The key insight is this: DSX Air and Vera Rubin were launched as part of the same system at the same time, not as products from two different eras.

Returning to the GTC on March 16, 2026, NVIDIA simultaneously announced three things: the Vera Rubin DSX Reference Design, the general availability of the Omniverse DSX Blueprint, and the launch of DSX Air. All three appeared together. This means DSX Air was never a “Blackwell-era tool.” From day one, it has been an integral part of the Rubin-era AI Factory architecture — an infrastructure validation platform prepared for Rubin, Rubin Ultra, and future generations.

Therefore, the fact that IREN is testing Blackwell Ultra today is not the important point. What matters is that it is validating a complete AI Factory deployment methodology that will apply to every future Rubin-series architecture. This methodology includes network topology, automated deployment, operations frameworks, and digital twin validation — capabilities that, once mature, will be reused across multiple generations. In short, IREN is not merely testing one generation of GPUs; it is validating in advance how AI factories should be built for the next ten years.

This also explains the sharply different market reactions. Priority access to Rubin is an immediately modelable story: first access means faster revenue and EPS growth, and analysts can plug the numbers into spreadsheets right away. DSX Air’s validation capabilities, by contrast, represent long-term, systemic, and industrial value that is much harder to translate into next year’s EPS. Capital markets naturally favor stories that can be quickly quantified, so they price Rubin priority first and react coolly to DSX Air.

From an industrial logic standpoint, however, IREN’s participation in DSX Air is far more consequential than “who gets Rubin first.” Rubin is one product generation. DSX Air is the factory methodology for all future generations. The former affects one year’s revenue; the latter shapes ten years of competitive advantage. The market will understand the former quickly and gradually catch up on the latter. IREN currently sits in the position that “requires time to be understood.”

IREN and NVIDIA are jointly defining the DSX architecture, jointly building 5GW-scale AI factories, jointly running digital twin validation, and jointly developing deployment processes. This level of collaboration is approaching the co-creation of industrial standards, not merely a priority supply arrangement. It represents a fundamentally deeper partnership than the priority delivery rights secured by CRWV and NBIS.

IREN consistently chooses to tackle the difficult challenges first. It focuses on the critical areas that enable the fastest possible compute capacity to come online — the very things that will ultimately give it real pricing power in the future — rather than waiting for others to decide who receives priority supply. This has always been its nature and the direct result of its long-term vision. That is where its greatest value lies.

$IREN’s new Innovation Officer

A few months ago, $IREN appointed John Gross as their new Chief Innovation Officer, a role in which he'll be pivotal to the development of the company's AI data centers.

The Wall Street Journal recently ran a piece on him that I think is worth commenting on.

Gross specializes in high-density & liquid cooling infrastructure, with over 20 years of experience in the space. That makes him a critical hire for $IREN, given their emphasis on designing & developing all data center infrastructure in-house.

What I particularly found interesting about the WSJ article is that it goes into Gross's approach and philosophy.

He comes across as a very hands-on guy and not some office dweller. He likes being on the ground where the actual liquid cooling tech is being installed and tested, working together with construction crews to fix problems that can't always be foreseen months in advance.

Great to see $IREN's CIO with this kind of attitude. Getting his hands dirty when he needs to and leaving his ego at the door. He's clearly all about pushing $IREN forward and getting things done.

He also pushes back pretty directly against the industry default, which has historically been very risk-averse.

He says the industry “loves innovation as long as it’s 10 years old”, which is pretty funny.

That risk-averse, slow mindset clearly doesn’t work in AI, where chip generations turn over every 12-18 months and thermal envelopes keep climbing.

This kind of attitude combined with $IREN's broader culture is what makes them a disruptive force in the industry that can really challenge the status quo.

Gross also called AI data center tech a bit of a poker game. You can't sit on the sideline waiting for the chip roadmap to be 100% clear, you have to read what's coming and place your bets early.

$IREN has clearly been great at this. Horizon was designed early last year to be future-proof for next-gen chips, more than a year before the official Rubin specs came out. Back then estimates were that Rubin would require densities of ~300 kW per rack, so $IREN's 200 kW design may have looked inadequate initially.

They were obviously proven right...

I know $IREN execs had a very tight relationship with $NVDA well before the official partnership was made public.

That kind of access gives you early visibility into where the industry is heading years in advance, and that's exactly where close ties to $NVDA pays dividends as it relates to developing next-gen infrastructure.

Gross also commented on $IREN's iterative improvement loop, where lessons from each build feed back into the next design cycle.

This reminds me very much of what David Shaw, $IREN's Chief Operating Officer, told me about a year ago when I visited the Childress site with @FransBakker9812 and a few other friends.

Shaw and the other ops execs really emphasized the same design and development philosophy of replication and continuous improvement.

Every individual new build is slightly different from the last as the team implements lessons learned from the previous one. That will mean Horizon 2 will have improvements over Horizon 1, Horizon 3 over Horizon 2, and so on.

The advantage of that approach is that it directly leads to faster, cheaper, and more robust builds, which is a critical trait when you're developing a gigawatt-scale data center portfolio.

This isn't something they started doing recently either. It has been part of the company's DNA since day one.

It only works because of $IREN's very flat hierarchy and very healthy work culture, which encourages every construction crew member to spot flaws or find better ways of doing things.

This is also how they managed to bring the development cost per MW of their air-cooled data center shells down from $750k/MW to $600k/MW.

Going forward this is going to be one of the key competitive differentiators.

While other neo-clouds heavily rely on a patchwork of developers across their data center pipeline, $IREN is the head contractor on 100% of their projects.

The amount of operational experience they'll accumulate as they rapidly scale will become unmatched and very difficult to catch up to.

I also must say, this WSJ article is a real win for $IREN on the IR and marketing front, and they deserve credit for setting it up.

The company's comms had undoubtedly been pretty weak leading up to the recent earnings call, but over the past 3 weeks they've gotten noticeably better imo.

From the CEO’s mega thread here on X that cleared up a lot of confusion to now this WSJ collab… these are real positive moves from the team and they're worth praising.

Overall the WSJ piece does a great job giving us good visibility into Gross himself and his role at $IREN, as well as the company's broader strategic positioning.

I really enjoyed going through it. Definitely worth a read.

https://t.co/l64Kd3IVIC

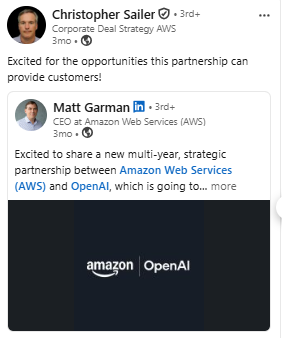

$IREN Hires Former AWS Executive Christopher Sailer

In his previous role in corporate deal strategy at AWS, he delivered on high-profile transactions such as the @awscloud x @AnthropicAI partnership, and a multi-year partnership with @OpenAI.

Welcome aboard @IREN_Ltd 🔥👏

IREN has entered into a $1.6bn purchase agreement with Dell for air-cooled Blackwell systems to support its previously announced 5-year, $3.4bn managed services AI cloud contract.

The systems are expected to be deployed across existing data centers at Childress, Texas, with commissioning targeted for early 2027.

Upon commissioning, the AI cloud contract is expected to increase IREN's annualized run-rate revenue (ARR) from $3.7bn to $4.4bn.

@danroberts0101, Co-Founder and Co-CEO of IREN commented:

“Securing capacity and accelerating commissioning are our top priorities in a market where time-to-compute is everything. Hyperscalers, enterprises and developers choose IREN as a partner because we own and control the full stack - the physical infrastructure, the compute, and the operational capability to deploy at scale.

Our relationship with Dell ensures access to hardware at the scale and speed the market demands. Every deployment we complete makes the next one faster, and that compounding execution advantage is what we are building.”

Learn more: https://t.co/xcg2XFO5b2

$IREN & Anthropic, Part II: The Greatest Catalyst Comes from Extreme Efficiency and Optimal Cost

The first part of this theme primarily analyzed the significance of IREN’s uniquely neutral positioning to Anthropic. This article is the second part, examining the fundamental factor truly driving the cooperation between the two sides.

Let me begin with the conclusion: IREN’s Sweetwater will become an essential site for Anthropic’s hyperscale training and inference operations, and NVIDIA is the most likely active facilitator behind this deal. The core force truly binding Anthropic and IREN together comes from exceptional efficiency and optimal cost — the most fundamental element that any company aspiring to become a top-tier enterprise simply cannot avoid. The cooperation between NVIDIA and IREN is aimed precisely at this element.

Among the creators of this advantage, IREN provides the optimal cost structure, the fastest response speed, the best operational management, and the most secure long-term electricity supply capacity. NVIDIA provides overall operational planning and maintenance, full-stack technological support for the DSX system, and jointly builds with IREN the flagship standard for DSX AI intelligent factories. The numerical embodiment of this standard is extreme efficiency. To use numbers as an analogy, the integrated flagship DSX system they are building could allow 1GW of electricity to generate the equivalent token output of 2GW or even 8GW. In today’s energy-constrained real world, this carries incomparable significance.

Maximum efficiency and optimal cost naturally become the first choice for the strongest models — the “brains.” They will become enhanced validations of each other’s greatest strengths: the strongest models become even stronger, producing higher output, thereby proving that this system of extreme efficiency and optimal cost can become a universally deployable standard. The AI intelligent factory standard led by NVIDIA and co-built with IREN, through deployment by Anthropic’s leading models, will radiate capability outward from the NVIDIA ecosystem to the four hyperscale companies currently cooperating with Anthropic. Through comparative advantages, these hyperscalers will be compelled to consider moving closer to NVIDIA’s AI intelligent factory model. Anthropic can therefore completely break free from the awkward dynamic of simultaneously cooperating and competing with the four hyperscalers, gaining far more strategic initiative. For Anthropic, this is the best possible path with no true alternative — increasing its autonomy while gaining a clear advantage in its competition with OpenAI.

At the same time, validation through top-tier model deployment creates top-down momentum that helps promote the flagship DSX intelligent factory standard itself.

Extreme efficiency and optimal cost are the universal keys to success for any enterprise. Using them as the analytical link connecting IREN, NVIDIA, and Anthropic is by far the most convincing explanation. Claims such as “someone’s girlfriend works as an executive at Anthropic, so he massively increased his IREN holdings” are merely street gossip and cannot serve as a basis for judgment.

A large part of Tesla’s success came from extreme cost efficiency. IREN became the only consistently profitable company in the Bitcoin mining industry for the same reason. Now, in the AI world, the role of IREN’s extreme cost advantage is even greater, and the difficulty is far higher. During the Bitcoin mining era, it was sufficient to secure grid power, establish peak-balancing agreements with utilities, choose remote locations, and maintain ample redundancy. The vertically integrated model of building data centers did not demonstrate particularly obvious importance or moat value in the Bitcoin business. But in the AI era — especially in the stage of AI intelligent factories under the DSX framework — full-process, vertically integrated control becomes enormously significant for achieving extreme cost efficiency.

NBIS’s recent forced decision to spend $2.6 billion turning to BE in search of power resources is the best possible illustration of IREN’s extreme cost advantage. On this point, @Enduciot1nvest has provided extremely detailed data analysis. After running the calculations, you realize how enormous the gap truly is. The capital markets have clearly made a major mistake: they have almost completely reversed the pricing of certainty versus extreme uncertainty.

As for optimal efficiency, there are two layers of meaning.

The first is the improvement brought by the design and integration of hardware infrastructure. This is exactly what NVIDIA, Dell, Lenovo, and IREN are jointly researching at IREN’s 60MW Childress site in Texas, and what will gradually be reflected in the flagship DSX intelligent factory to be established at IREN’s SW1 site.

The second layer of optimal efficiency is what IREN has consistently emphasized: what kind of data center it intends to build and operate. On this point, I will quote research material provided by Germany-based @IdeaLDeFi. His material strengthens and complements this article, and I appreciate his contribution. The italicized section below is quoted from his content:

At Sweetwater, what IREN and NVIDIA are building is not a data center custom-designed for one specific client, but a massive AI factory capable of hosting multiple enterprises simultaneously. It resembles a never-stopping digital racetrack: the infrastructure is provided by IREN, the compute engine is powered by NVIDIA’s DSX architecture, and who gets to use the racetrack depends entirely on demand at any given moment. Anthropic is merely one tenant, leasing part of the space to train Claude; at the same time, large corporations, banks, and research institutions are training their own medical AIs, financial models, or image generators in different sections of the same factory. All tenants share the same physical infrastructure while operating their software and data in completely isolated environments. This model is known as a multi-tenant compute factory.

The genius of this factory lies in the fact that it is itself a system capable of autonomous operation, autonomous measurement, and continuous optimization. IREN’s power and cooling systems must operate at full load 24 hours a day, meaning any compute vacancy is immediately filled. If Anthropic temporarily reduces demand after completing one stage of Claude training, the spare capacity is instantly absorbed by a bank’s risk models, a hospital’s medical imaging training, or an automaker’s autonomous driving systems. Compute is never wasted, and utilization remains close to the theoretical limit at all times. Meanwhile, Mirantis’s software layer ensures complete data isolation between all tenants. Even if a bank’s workloads and Anthropic’s workloads run on the same batch of NVIDIA superchips, they can never access each other’s data. Every client enters the factory with its own models, software, and data, without any points of contact between them.

For Anthropic, the scalability enabled by this model is nearly decisive. If it wants to catch up with Google or Microsoft, building its own data centers, power systems, and cooling infrastructure would require hundreds of billions of dollars in investment. But inside IREN’s factory, this infrastructure is already deployed in advance. Anthropic only needs to continue extending new NVIDIA racks into adjacent machine halls in order to scale training without shutting the system down. If tomorrow it decides to train a new model twice the size of Claude 4, it does not need to wait for a new campus to be constructed, nor does it need downtime testing. NVIDIA’s DSX architecture can use digital twin technology to simulate the thermal, electrical, and networking changes brought by expansion before deployment, allowing the entire factory to remain stable during scaling.

In a sense, IREN resembles the world’s most advanced skyscraper: it provides the foundation, electricity, cooling, and structural framework; NVIDIA provides the top-tier office equipment and technological systems; and Anthropic becomes the flagship tenant occupying the top floors, performing its model “magic” within it. Other enterprises occupy their own floors in the same building, training their own models and running their own applications without overlap. Automotive companies train autonomous driving systems, banks train financial models, research institutions run medical simulations, and some enterprises even directly deploy open-source models such as Llama or Mistral. All of this occurs simultaneously within the same factory, without interference.

Once you connect all of these elements together, you realize the true nature of this AI factory: it is not built for any single company, but for the entire AI era. It is a digital racetrack that is always running, always expanding, and always optimizing — and Anthropic is merely one race car pushing the track to its limit. The true protagonist is the infrastructure itself: a platform capable of hosting countless models, countless enterprises, and countless future possibilities.

Excellent. He emphasized the enormous appeal and capability of the never-shutting-down digital racetrack jointly built by IREN and NVIDIA. If you understand IREN, you will know that this vision of a multi-tenant compute factory has always been $IREN’s ambition. I even believe the implementation of this function represents IREN influencing NVIDIA. It opens up an even broader development space for extreme efficiency. Achieving this truly requires the coordinated operation of multiple top-tier enterprises; it goes far beyond the narrow technical meaning of merely designing and assembling server racks.

Now let us return to the theme of this article: what does this mean for Anthropic? What additional value can this kind of environment bring to NVIDIA, IREN, and Anthropic?

For the NVIDIA–IREN intelligent factory system:

Anthropic occupies a unique position. It is the “flagship race car” that pushes the entire racetrack to its limits. Its existence creates a structural driving force for the factory itself: the scale of its training workloads, the complexity of its models, and its extreme requirements for network latency and thermal management continuously force IREN and NVIDIA to raise the standards of the factory. Anthropic’s training tasks themselves become stress tests for the factory — the driving force behind continuous upgrades of the entire system. In a system where not a single second of compute downtime is tolerated, every tenant can obtain exactly what they need inside the isolated environments created by Mirantis, all while achieving maximum efficiency.

Although there is no overlap whatsoever at the data layer between tenants, a kind of “physical-layer resonance” still exists. This resonance is not information sharing, but mutual reinforcement at the infrastructure layer.

When a bank trains risk models, it fills the temporary compute vacancies left unused by Anthropic, allowing the factory to remain fully loaded. When a hospital trains medical imaging models, it keeps IREN’s power systems operating under stable thermal loads. When an automotive company trains autonomous driving models, it continuously validates NVIDIA’s network architecture under high-concurrency conditions. None of these activities are related to Anthropic’s business, yet invisibly they make the entire factory more reliable, more efficient, and more mature.

And it is precisely within such a continuously “polished” environment that Anthropic trains Claude. What it enjoys is an infrastructure that is always fully loaded, always stable, and always optimized — and the maturity of this infrastructure comes precisely from the existence of those other tenants that have nothing to do with it. There is no direct cooperation between them, yet they form a remarkable kind of “infrastructure symbiosis.”

For Anthropic:

First, it no longer needs to worry about infrastructure; it only needs to focus on the models themselves.

Second, its training environment becomes stronger, more stable, and more efficient because of the presence of other tenants. This is a form of “passive benefit.”

Third, within the ecosystem established inside this factory, it gains enormous additional advantages. The larger this ecosystem becomes, the better its training conditions become and the greater its returns become.

What truly changes inside an AI factory operating within the same physical campus is the relationship between compute resources themselves. Traditional cloud systems depend on public internet transmission, where model invocation is an expensive, slow, and friction-filled API request. But inside the factory, all models, databases, and inference engines are placed on the same high-speed interconnected backplane. APIs are no longer “network requests”; they become “internal process calls.” Latency falls from milliseconds to microseconds. Data no longer crosses borders, no longer requires encryption, and no longer incurs bandwidth fees. All computation is completed within the campus intranet, as naturally as scheduling different threads within the same machine. This physical proximity eliminates the resistance created by “data gravity,” transforming tasks that once required multiple network hops into local calls.

Once the distance between models is compressed to this degree, business logic undergoes a qualitative transformation. In the past, banks needed to package, encrypt, and upload internal data, call Claude’s API, wait for results, and then hand them back to internal risk-control models for processing. Under the factory model, however, the bank’s risk-control models and Claude’s inference replicas function as though installed on the same motherboard. A trigger from the database can directly invoke Claude’s real-time analysis, whose output is then returned within milliseconds to the risk-control system for final decision-making. The entire chain becomes a computational assembly line, automatically orchestrated into a continuous sequence of actions, as though all components were simply different modules of the same software.

Anthropic never touches the bank’s data. It merely deploys Claude’s inference clusters into certain cabinets within the campus, while other tenants access these replicas through internal high-speed gateways. All traffic flows within physically isolated intranet environments, never leaving the campus and never passing through public internet encryption. For the first time, enterprises can simultaneously possess the security of private deployment and access to the world’s most advanced models, without having to make painful trade-offs between the two.

And for Anthropic, the significance of this system extends far beyond merely “selling models.” It is no longer simply a provider of application programming interfaces. Instead, it becomes the intelligent foundation layer of the factory itself — an “intelligence source” that all tenants can invoke at any time. Claude’s role here resembles electricity or water: an always-available production resource capable of real-time response and extraordinary efficiency due to physical proximity. As more and more enterprises embed their business logic into this internal compute assembly line, Anthropic’s models become foundational intelligent components of the entire campus, deeply integrated into the computational pathways of every enterprise.

When inference evolves from a “consumer product” into a “means of production,” and when collaboration between models becomes automatically orchestrated within millisecond-level timeframes, the speed at which enterprises build applications becomes the new competitive frontier. Since everyone effectively “lives in the same building,” a new form of homogeneous compute collaboration may emerge in the future. For example, an autonomous driving company could invoke Claude’s inference capabilities through the factory’s ultra-high-speed internal network, or a bank could perform model fine-tuning directly within the factory, leveraging the underlying data-flow architecture validated by Anthropic. This geographic proximity — where physical distance is compressed into millisecond-level latency — creates a “compute ecosystem park” effect.

For Anthropic, this means its growth speed, model iteration capability, training cost structure, and scalability will all be amplified by this ecosystem. It does not need to depend on other tenants, yet it benefits from their existence. It does not need to cooperate directly with them, yet the compute ecosystem park effect greatly increases its own value.

The situation described above is the best real-world illustration of what Daniel referred to in his long essay on “three layers of structure and a continuously compounding advantage”: resources become locked in, customers become bound, operational records become entrenched, supply chains become occupied, and the industry landscape becomes rapidly fixed into place within a short period of time.

Once such a system emerges, its competitiveness becomes extraordinarily powerful. It represents the integration of multiple layers of excellence. The improvement in efficiency and output is no longer several isolated points operating in parallel, but the coordinated collaboration of an entire industrial cluster. Every participant in the process is elevated dramatically.

At this point, it can be said that multiple logical threads have completed mutual validation. Under the guiding principles of extreme efficiency and optimal cost, it becomes only natural for top-tier enterprises to come together, because they will reinforce and strengthen one another. This is jointly determined by three major forces: the limitations of social resources, the efficiency principles driving industry development, and the pursuit of capital returns through cost control.

Please stay tuned for Part III — How IREN and Anthropic May Ultimately Cooperate.

𝐓𝐡𝐫𝐞𝐞 𝐋𝐚𝐲𝐞𝐫𝐬. 𝐎𝐧𝐞 𝐂𝐨𝐦𝐩𝐨𝐮𝐧𝐝𝐢𝐧𝐠 𝐀𝐝𝐯𝐚𝐧𝐭𝐚𝐠𝐞. 𝐓𝐡𝐞 𝐈𝐑𝐄𝐍 𝐓𝐡𝐞𝐬𝐢𝐬.

There's been a lot happening at IREN recently.

Expansion across North America, Europe and Asia-Pacific.

The NVIDIA partnership.

The Mirantis acquisition.

New GPU deployments.

New customer discussions.

A growing global footprint.

Underneath all of it is a fairly simple view of where the world is heading, and a deliberate strategy for how we position IREN within it.

That strategy is built on three layers. Together, they compound into a structural advantage that gets harder to replicate every quarter we execute.

Layer 1: Physical infrastructure. Power, land, substations, data centers, cooling. The foundation that everything else sits on.

Layer 2: Compute infrastructure. The GPUs, servers and networking that go inside those buildings. Deployed at scale. Generating revenue. Building execution track record.

Layer 3: Software and operational capability. The orchestration, deployment tooling and enterprise expertise that makes the first two layers work harder for customers, and opens the door to a broader, higher-value market over time.

Layers 1 and 2 are where the overwhelming majority of IREN's value is being created today. Layer 3 is where that advantage compounds further over time, but only because Layers 1 and 2 are built, owned and controlled at scale by IREN, not subscale nor contracted from a third party.

Think of Amazon. They didn't win e-commerce by building a great website. They won it by controlling the fulfilment infrastructure at a scale nobody else could replicate. The foundation you don't control becomes the ceiling on your business.

That is exactly how we think about IREN. The physical infrastructure - the land, the power, the substations, the data centers - is owned and controlled by us. The compute deployed into it generates the revenue and execution track record. And the software, orchestration and enterprise capability we are more methodically building on top is what turns the total product into a vertically integrated AI Cloud platform that compounds over time and deepens into a competitive moat.

AI is still early. The bottleneck is increasingly physical. And we have spent eight years building the foundations.

$IREN

Needham hosted IREN last week....

These are some takeaways:

"For 2027 capacity, negotiations are underway with hyperscalers and frontier labs."

"Australia APC grid connection approvals nearing completion."

👀

$IREN & Anthropic: The Strategic Inevitability of a Partnership — and IREN’s Emerging Pricing Power

A:

According to the latest data, Anthropic’s compute supply is nowhere close to keeping up with its revenue growth. Dario Amodei confirmed that during the first half of 2026, the company experienced an 80x surge in revenue demand. Anthropic’s annualized revenue has now surpassed $30 billion, and the number of enterprise customers spending more than $1 million per year has grown beyond 500 — then doubled to over 1,000 within just two months.

Anthropic is currently paying xAI $15 billion per year for compute capacity under a contract that lasts until May 2029.

At the same time, Anthropic has signed multi-gigawatt TPU agreements with Google and Broadcom, with deployments expected to begin in 2027. Before this, the company had already diversified across AWS, Azure, NVIDIA GPUs, and other hardware platforms, reflecting a strategy of “matching different workloads with the most suitable chips.”

But if you look closely, Anthropic’s compute structure is filled with hidden risks and strategic poison pills.

On the surface, its four major compute supply lines appear “diversified.” In reality, the structure is extremely fragile. Every supplier involved has both the motivation and the ability to weaken — or even seriously damage — Anthropic.

Amazon is Anthropic’s largest shareholder and may provide up to 5GW of AWS compute capacity, while simultaneously competing directly with Claude through Bedrock. Every time Anthropic trains Claude, it is effectively strengthening AWS’s own competitive position.

Google provides multi-gigawatt TPU capacity, yet Gemini is one of Anthropic’s most direct rivals. Training Claude on Google’s TPUs potentially exposes model architecture and data access patterns, creating real strategic intelligence risks.

Microsoft Azure is another major compute provider, but Microsoft is deeply tied to OpenAI — Anthropic’s number one competitor. Training Claude on Azure essentially means subsidizing a rival’s infrastructure ecosystem.

Then there is xAI: both a competitor and a supplier holding a contract that can be terminated at any time. Elon Musk only needs to issue a 90-day notice to cut off the supply.

There is something deeply ironic about this whole situation. Colossus 1 is essentially a stranded asset after Musk shifted his main compute focus toward the Blackwell-powered Colossus 2. Letting Anthropic use part of that capacity is almost like casually giving Dario Amodei a drink of water to ease his desperation.

It makes Dario look like the pitiful bell-ringer Quasimodo — standing under the blazing sun while being whipped — yet still willing to pay $15 billion just to drink that water. The image feels almost humiliating in its desperation.

Put together, these four supply lines lead to one unavoidable conclusion:

Anthropic’s core compute infrastructure is entirely dependent on platforms controlled by direct competitors. This is not “multi-cloud redundancy.” It is a situation where every supply route runs through hostile territory.

B:

Now look at what IREN brings to the table:

5GW of secured global power capacity, with expansion still ongoing

Multiple gigawatt-scale sites powered directly by the grid and supported by green energy

A strategic partnership with NVIDIA to build what may become the world’s premier DSX flagship AI factory

No model business — IREN develops no AI models and does not compete with Anthropic

No strategic investment entanglements — IREN neither owns Anthropic equity nor is owned by Anthropic now.

No public cloud competition — IREN does not operate a hyperscale cloud platform and does not compete with Claude’s API business

A pure infrastructure identity: power + data centers + GPU operations + software orchestration

For Anthropic, IREN is the only truly neutral large-scale compute provider in the market.

There are five major dimensions that make IREN’s advantages almost irresistible to Anthropic — like a highly addictive drug.

Dimension One

Anthropic’s dependence on competitor-controlled compute creates a form of “replacement-cost pricing trap.”

Every unit of compute purchased from rivals comes with hidden costs:

exposure to strategic intelligence risks,

the possibility of service reductions,

weakened leverage during financing negotiations,

and potential regulatory scrutiny over “competitor-controlled training infrastructure.”

These costs may not appear on financial statements, but they are very real.

IREN’s neutral compute infrastructure eliminates these risks. Looking at the extremely expensive deal Anthropic signed with SpaceX/xAI — despite the obvious competitive toxicity — proves that Anthropic is willing to pay enormous premiums for compute access when under pressure.

Dimension Two

At the physical infrastructure level, Sweetwater’s 2GW scale creates a form of real-world irreplaceability.

Globally, there may be only one provider capable of delivering a single-site, gigawatt-scale, liquid-cooled, fully powered, DSX-certified facility by 2027–2028.

Anthropic simply has no credible “we can go elsewhere” bargaining position.

Dimension Three

Anthropic’s growth rate is dramatically faster than the timeline required to build compute infrastructure.

This mismatch between quarterly competitive pressure and multi-year infrastructure construction cycles means Anthropic cannot afford to wait. It must lock in the next 3–5 years of capacity as quickly as possible.

Again, the image of Dario as Quasimodo under the scorching sun feels strangely accurate.

Data centers are his water. Water. Water.

Dimension Four

The pressure from competing with OpenAI is so intense that Anthropic is already willing to accept terms from someone like Elon Musk.

So when a provider like IREN appears — offering enormous, high-quality capacity combined with NVIDIA-backed DSX flagship AI factory architecture — the attraction becomes overwhelming.

And if DSX significantly boosts compute efficiency, then 2GW inside a DSX environment may effectively deliver the output equivalent of 4GW or even 8GW elsewhere.

Dimension Five

IREN’s 5GW global data center pipeline stretches across the United States, Europe, and the Asia-Pacific region:

further expansion at Sweetwater,

new capacity at Kiowa,

the 490MW Nostrum project in Spain with additional gigawatt-scale development reserves,

and future Australian projects.

This physical infrastructure pipeline aligns perfectly with Anthropic’s two most urgent strategic needs over the next three years:

European regulatory compliance

Global expansion

The EU AI Act, GDPR, and data sovereignty requirements are increasingly forcing frontier AI companies to deploy local compute infrastructure inside Europe.

Anthropic can no longer rely entirely on U.S.-based cloud providers for cross-border hosting. It needs trusted, regulated infrastructure physically located within the EU.

Nostrum’s 490MW platform provides an immediate European compliance gateway, while Sweetwater serves as the primary U.S. training hub. Together, they naturally form an integrated cross-regional compute strategy.

Even more importantly, Anthropic’s future expansion into Asia-Pacific will also require local infrastructure nodes, and IREN’s Australian projects provide a future foothold there as well.

In other words, Anthropic’s entire globalization roadmap could potentially be completed through IREN’s infrastructure pipeline alone.

Taking all of this together, the potential partnership between IREN and Anthropic is no longer about “who chooses whom.”

Logically, it increasingly feels inevitable.

In fact, I believe the discussion has already shifted toward a different issue entirely:

Pricing power.

Under these conditions, IREN may gain rare leverage over contract structure negotiations, including:

higher upfront prepayment requirements,

stronger take-or-pay commitments,

dual-index pricing tied to both inflation and chip upgrades,

control over future expansion capacity options,

and even the possibility of exchanging capacity discounts for Anthropic equity participation.

Where does this bargaining power come from?

IREN’s neutrality itself carries enormous premium value for Anthropic.

That neutrality can be systematically priced into contracts.

Time pressure strengthens IREN’s leverage.

Anthropic is simultaneously squeezed by exploding demand and brutal competitive pressure.

IREN holds overwhelming advantages in data center quality, power availability, security, and stability.

IREN can satisfy three strategic needs at once:

U.S. training, European compliance, and future Asia-Pacific expansion.

This dramatically narrows Anthropic’s alternatives.

With a secured 5GW global infrastructure pipeline — and future expansion beyond that — IREN may become Anthropic’s only truly dependable global compute sovereignty provider.

That creates extraordinary leverage over both pricing and contract structure.

Finally, this may also explain why IREN no longer appears interested in signing traditional presale-style agreements like CRWV and NBIS.

With advantages like these, preselling its power capacity too early would effectively mean selling itself cheaply.

So even if IREN and Anthropic do eventually sign a deal, I believe we are likely to see a completely different kind of partnership structure — one that could reshape industry expectations.

This is my first article exploring the potential IREN & Anthropic relationship.

I plan to continue the discussion later when time allows. There are still many important topics worth analyzing, including how such a partnership might actually work in practice, NVIDIA’s potential role, and much more.

Please stay tuned.

And lastly, I’ve been extremely busy recently and haven’t had the energy to reply to everyone’s comments. Thank you for your understanding and support.

This is another pricing-power breadcrumb

If a three generations old GPU is still getting pricier, the bottleneck is alive and kicking

That supports the core thesis that AI infra owners may have more pricing power than the market assumes because customers are buying certainty and throughput

For $IREN specifically, it is bullish in a second order way. It suggests the market for compute is still tight enough that even older fleets retain value. That increases the value of any ready and energized capacity

Investigating $IREN's Q1 Revenue Miss

Working off @_Sgr_A_Star is a financial sleuthing we can uncover how IREN's PG (Prince George) ramp is going.

While PG's GPUs were ordered in Fall 2025, they arrived into Q1 2026. By end of Q1 2026, all but 1200 GB300s of had arrived. This is quite late compared to the order time and delayed arrival ate into slack time for burn-in and commissioning, after which they could generate revenue.

Although IREN was at 33.6m AI revenue, their RPO showed 300m ARR run rate which is 75m per quarter from PG. With all GPUs besides 1200 GB300s arriving at Prince George, we can expected 500m ARR by end of Q2 and assuming a linear ramp of burn-in and commissioning which means Q2 AI Revenue will be ~100m.

Q3 will be H1 handover which combined with PG will be 1B ARR for Q3. However ARR is the yearly run-rate. If H1 handover is in July and finished commissioning and burn in at end of July then only 500m ARR * 2/3 months / 4 quarters-per-year will be showed in Q3. Thus for Q3, we can expect 83m from H1 and 125m from PG for a total of 208m Q3 2026 revenue.

Q4 2025 Revenue: 17.4m

Q1 2026 Revenue: 33.6m

Q2 2026 Revenue: 100m

Q3 2026 Revenue: 208m

Why is revenue so low compared to ARR? Even for other Neoclouds that had higher priority on Nvidia GPU deliveries, ARR is much higher than revenue. Compare these 2026 ARR forecast for each Neocloud and their Q1 2026 quarterly revenue:

$CRWV | 18B-19B ARR | 2B

$NBIS | 7-9B ARR | 399m

$IREN 3.7B ARR | 33.6m

What's apparent is that the earlier you are in your ramp, the father you are from your ARR target because the growth is doubling every quarter. All these companies will see more than double revenue growth in H2 2026 because GPUs are back-staggered for all these Neoclouds as real GB300 ramp is H2 2026. IREN's ramp has been painful as it has been hardest hit by HBM shortgages but with Nvidia full partnership, 2027 look to get better.

IREN is a late mover in expanding their fleet but the advantage is that more of their fleet will B300/GB300s or newer compared to H100/H200 for competitors.

Blackrock Increases $IREN Position by 604.94%

On May 13, 2026 - BlackRock, Inc. filed a 13F-HR form disclosing ownership of 4,457,120 shares of IREN Limited (US: $IREN ) valued at $152,790,074 USD as of March 31, 2026.

The entity filed a previous 13F-HR on February 12, 2026 disclosing 632,268 shares of IREN Limited.

This represents a change in shares of 604.94% during the quarter. The current value of the position is $252,094,707 USD.

https://t.co/VUq9eB4222

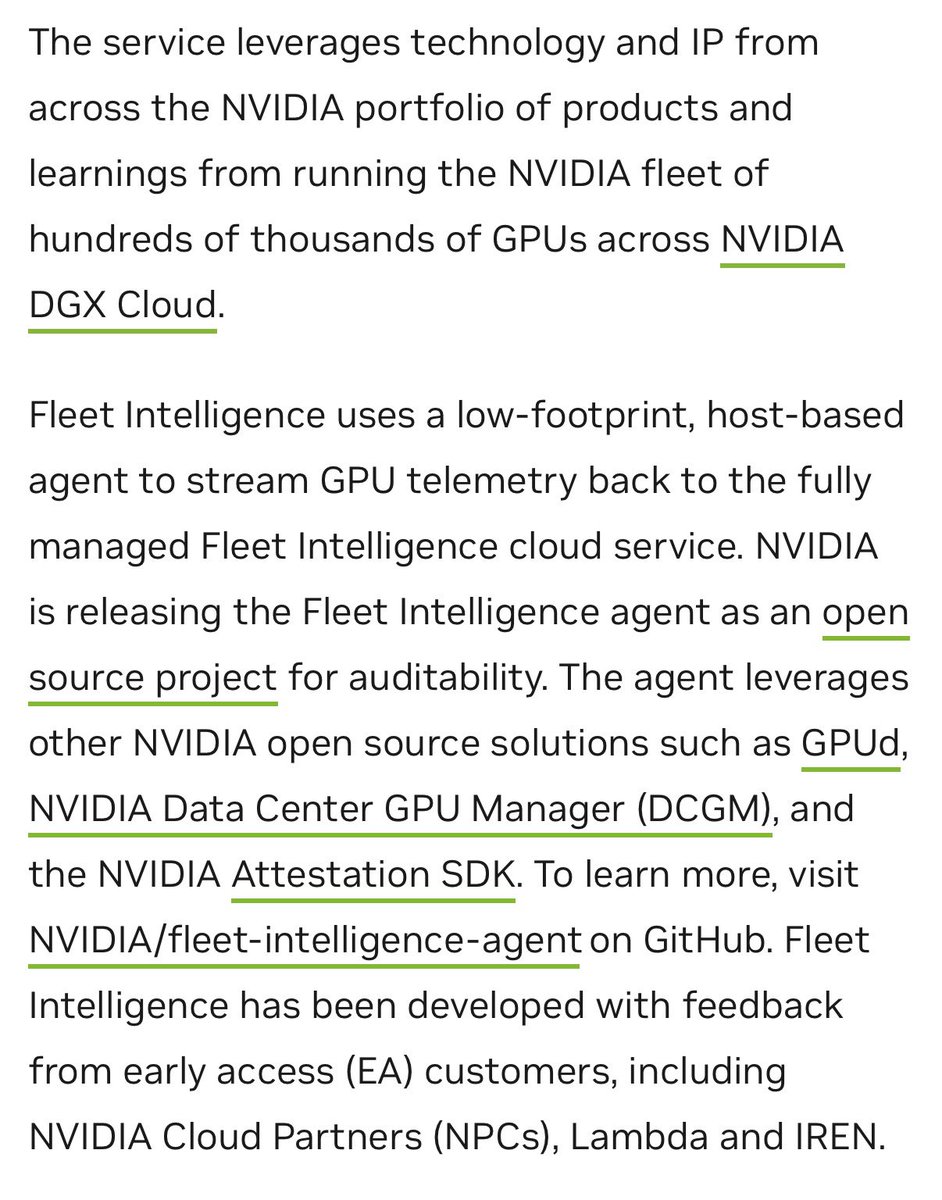

$IREN is an early access partner for NVIDIA’s new Fleet Intelligence

Fully managed cloud service delivering deep visibility and intelligence through hundreds of thousands of GPUs across Nvidia DGX Cloud

With a strong foundation in place, it is now up to accretive funding and delivery