A weekly market discussion with DoubleLine's Macro Asset Allocation team recorded Friday afternoon for your Monday morning commute, or anytime in between.

Amid the ping pong of headlines over the U.S.-Iran conflict, a thin leadership of tech giants in May, @DLineCap's Eric Dhall and Ryan Kimmel note, drove the S&P 500 into new highs while bond yields eased, albeit to still elevated levels.

https://t.co/qjFzOfLYXG

May ISM Manufacturing PMI increased to 54.0 from 52.7 the previous month and 53.0 consensus, the highest reading since May 2022. Prices paid component showed upside pressure on input prices, with the component near a four-year high.

Rooting for peace but keeping it real: “The U.S. is negotiating with some more moderate people in Iran,” Eric Dhall says, “but the guys with the guns don’t necessarily agree with those moderates.”

https://t.co/qjFzOfMwNe

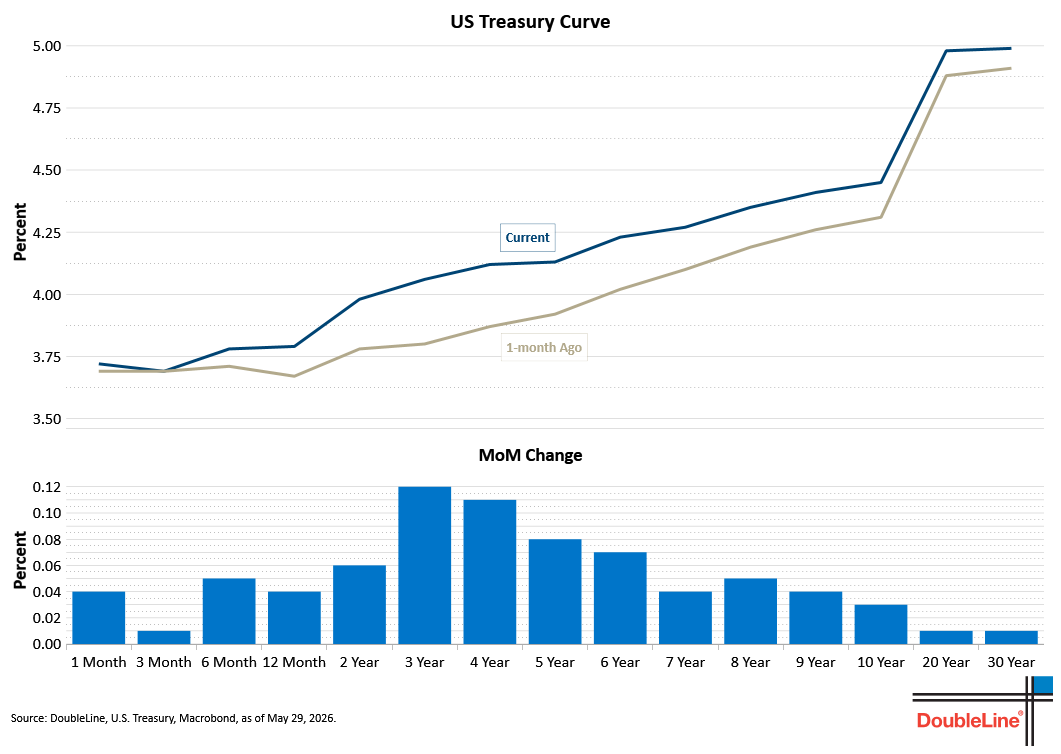

“At the long end of the curve, the premium owes less to inflation risk and more to fiscal issues, which is exacerbated by higher rates,” Ryan Kimmel says. “A negative feedback loop as interest costs on the U.S. debt become larger and larger.”

https://t.co/qjFzOfLYXG

Despite easing from mid-month, Treasury yields “remain elevated vs. the beginning of the month,” Eric Dhall observes. “There’s still a term premium there; investors are still concerned about inflation and budget deficits.”

👉https://t.co/qjFzOfLYXG

Rooting for peace but keeping it real: “The U.S. is negotiating with some more moderate people in Iran,” Eric Dhall says, “but the guys with the guns don’t necessarily agree with those moderates.”

https://t.co/qjFzOfMwNe

Olive Oyl-skinny market leadership: “With the S&P 500 trading 7% above its 50-day moving average,” Ryan Kimmel notes, “only 56% of stocks in the index are trading above their 50-day. This rally is driven by a select few large stocks.”

👉https://t.co/qjFzOfMwNe

“All these IPOs are planned for the next six months – OpenAI, Anthropic, SpaceX,” says Eric Dhall. “They’re all trying to rush to market while the animal spirits are abounding, and irrational exuberance is pressing any skepticism away.”

https://t.co/qjFzOfLYXG

The second estimate of Q1 GDP showed the economy grew by 1.6%QoQ annualized vs. 2.0% initial estimate, lower than 2.0% consensus.

Personal consumption revised to 1.4% from1.6%. Investment revised to 7.0% from 8.7%, equipment (+17.2%) and IP (+11.6%), residential (-6.2%).

Government spending unchanged at a strong 4.4%. Net exports detracted -1.3%, driven by a 21.1% surge in imports.

Real final sales to domestic purchasers strong at 2.4%.

Personal income was flat April vs. expectations of +0.4%MoM; wage income increased 0.2%MoM.

On a year-over-year basis, real wages & salaries growth turned negative at -0.2% and real disposable personal income -1.1%.

The PCE deflator for April was softer than expectations, +0.40%MoM vs. 0.5% consensus and 0.66% in March. The year-over-year pace rose to 3.8%, the fastest pace since May 2023.

Core PCE, +0.24%MoM vs. 0.3% consensus and 0.30% in March. Year-over-year core PCE increased 0.1% to 3.3%, the fastest rate since Nov 2023.

Core services PCE decelerated to 0.19%MoM. Core services ex housing (supercore) decelerated to 0.12%MoM.

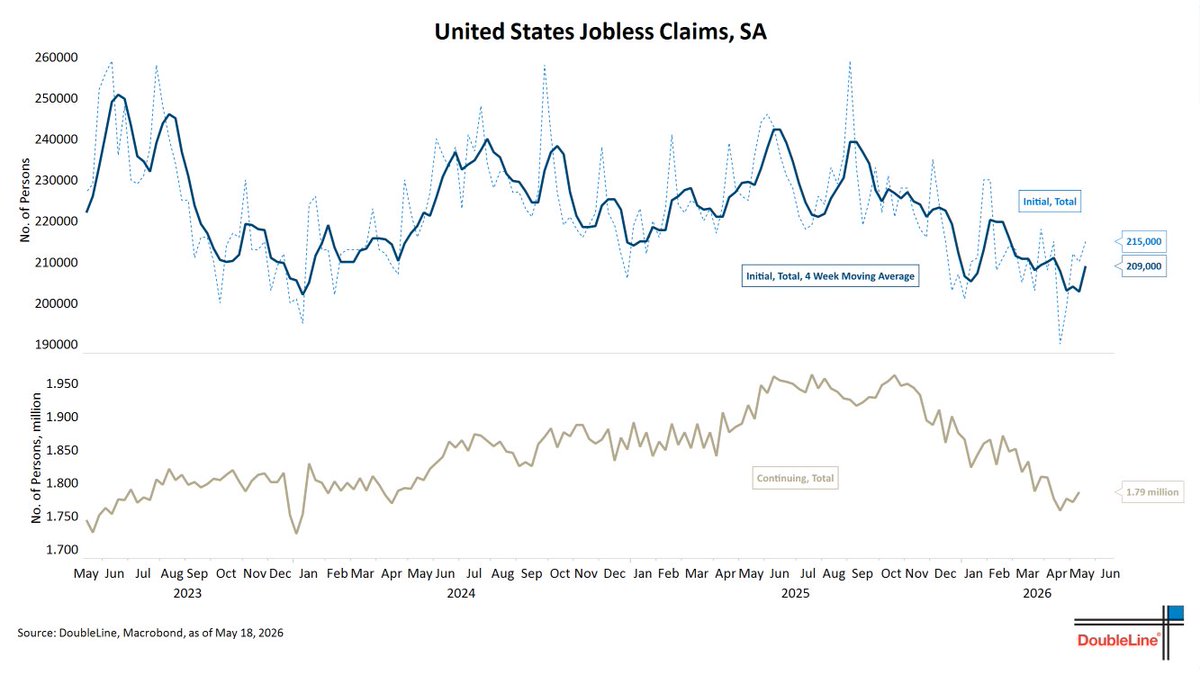

Initial jobless claims for the week of May 23rd rose 10k to 215k vs. 211k consensus. The 4-week moving average ticked up to 209k. Continuing claims increased 15k to 1,789k vs. 1,784k consensus. The data is not indicating an inflection higher in layoffs.

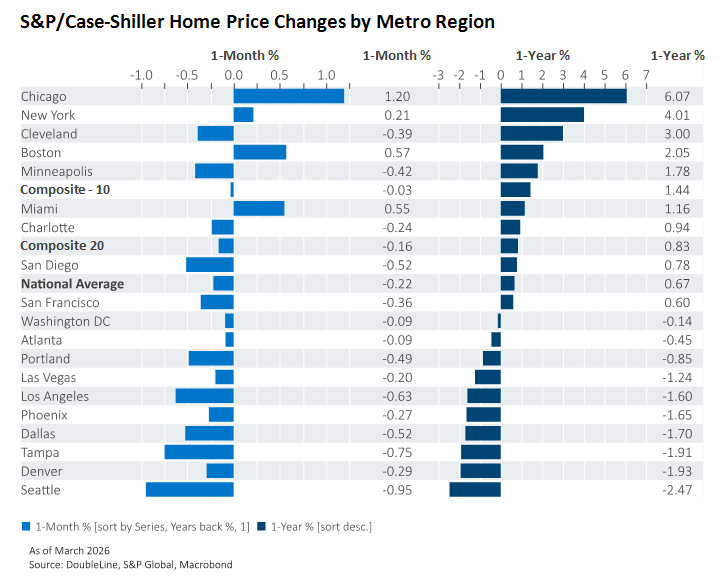

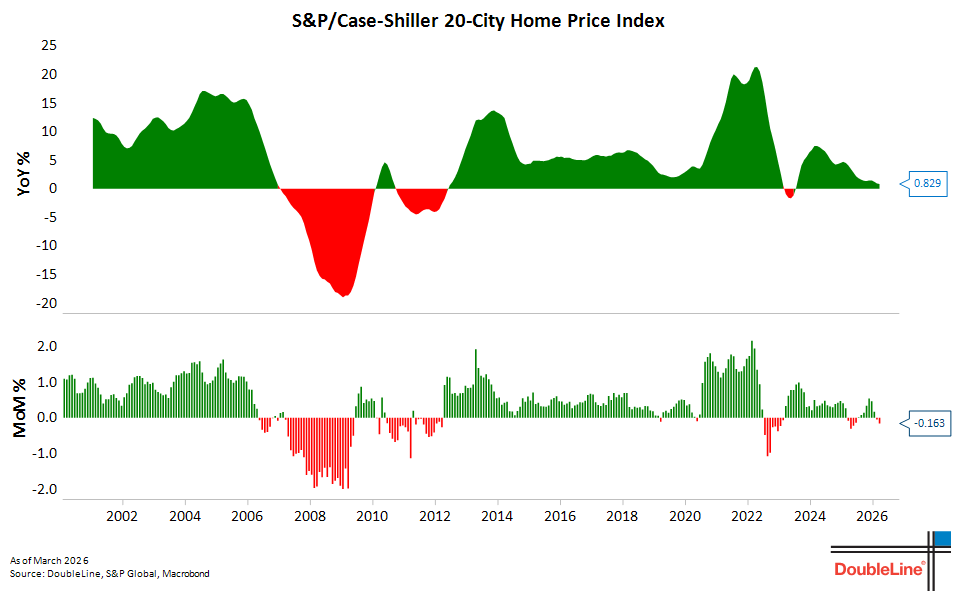

Home prices, as measured by the S&P Cotality Case-Shiller 20-city Composite, decreased 0.16%MoM in March vs. -0.10% consensus and -0.05% the previous month. The year-over-year pace decelerated to +0.83% NSA.

“The cost of living continues to be a first-order concern, with 57% of consumers spontaneously mentioning that high prices were eroding their personal finances, up from 50% last month. Lower-income consumers and those without college degrees posted particularly strong sentiment declines; these groups are more sensitive to increases in the cost of gas and other essentials.” – U.Mich.

University of Michigan consumer sentiment final release for May saw downward revisions, 44.8 vs. 48.2 consensus and 48.2 initially reported – a record low for the series.

University of Michigan consumer sentiment final release for May saw downward revisions, 44.8 vs. 48.2 consensus and 48.2 initially reported – a record low for the series.