🗞️ RWA & Tokenization: daily digest. June 1st

📈 Total RWA value: $31.8B, +1.95% from 30d ago

📈 Total asset holders: 833.2K, 11.3% from 30d ago

1️⃣ Private credit has overtaken Treasuries as the largest non-stablecoin RWA segment

The total market is $34.5B, with 100%+ year-on-year growth, but its composition has shifted. Treasuries are still the most-cited category (BUIDL, BENJI, USDY dominate the brand narrative), but private credit – corporate loans, yield-bearing debt instruments, structured credit products – has absorbed more institutional capital by aggregate TVL.

2️⃣ GENIUS Act implementation: 47 days to the July 18 deadline. The Clarity Act is moving in parallel

What's still unresolved going into June:

→ Yield passthrough rules for retail stablecoin holders (the question banks are fighting hardest)

→ Tech company restrictions on issuance (the non-financial public company provision)

→ Stablecoin naming standards

→ House-Senate reconciliation on the CLARITY Act market structure bill, which runs parallel

3️⃣ @chainalysis: new Ethereum wallets are being created specifically to hold tokenized assets

After years of flat activity from 2022 to late 2024, the number of new Ethereum wallets created specifically to receive tokenized assets in the first six months of their existence spiked sharply through late 2025 and into 2026.

The interpretation: for a growing cohort of new on-chain participants, tokenized assets – not DeFi, not NFTs, not speculative crypto – are the reason to create a wallet. These wallets typically hold institutional-grade RWA products first, then diversify into other categories.

4️⃣ Only $2.47B of $34B in tokenized RWAs is actually composable in DeFi

The rest sits in institutional wallets behind compliance rails.

The BlackRock BUIDL – UniswapX integration from February 2026 is the clearest example of the gap starting to close: whitelisted accredited investors can now trade BUIDL around the clock on Ethereum. But the keyword is "whitelisted." You still can't take BUIDL and drop it into a Curve pool or use it as collateral in an ungated lending market.

DeFi lending still has a problem.

Most of it runs on overcollateralization because protocols can’t assess risk beyond what’s onchain.

ZKredit, co-built with @brevis_zk & @primus_labs, starts to change that 🧵 👇

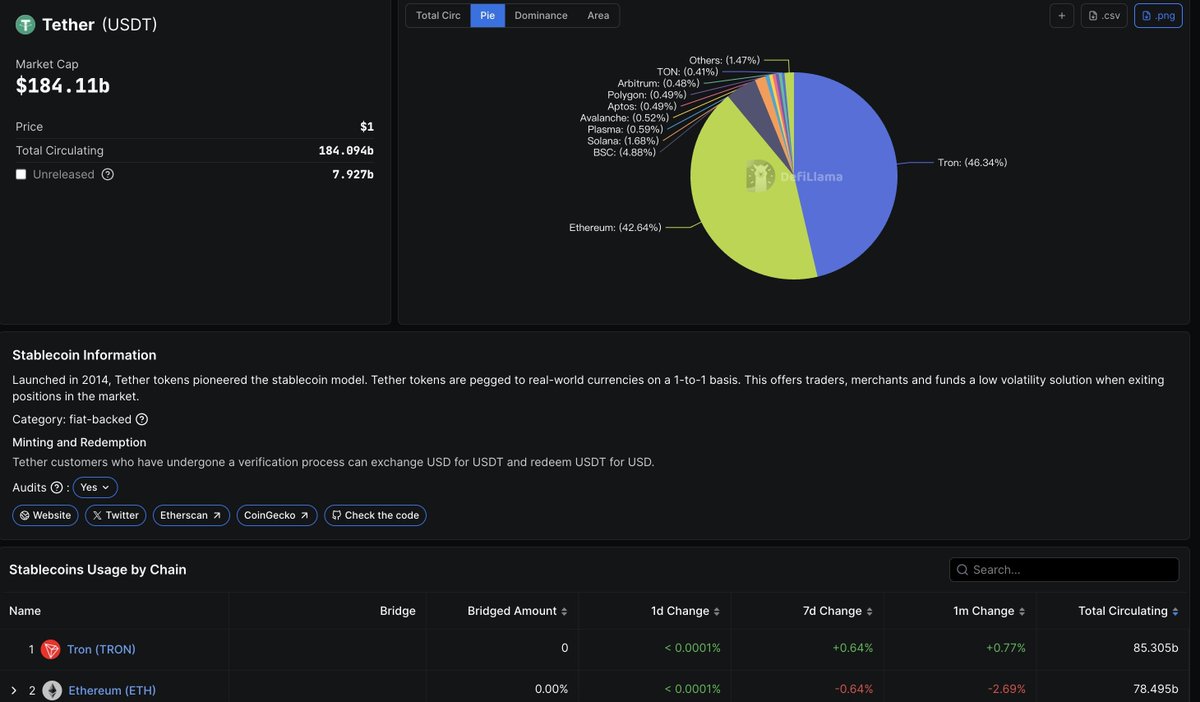

Tether just minted another $1B USDT on Tron, pushing its supply there to ~$85.3B, now well above Ethereum.

That tells you where the real stablecoin demand still lives: fast, cheap settlement rails. Tron might not win narratives, but it keeps winning dollar flow.

The way ZachXBT framed it has already sparked a wave of discussions and narrowed down the list of suspects 🌚 It has to be a team consistently profiting from privileged access to information about listings, liquidity routing, and launch timing.

So… who could it be? On @Polymarket, users have already compiled a shortlist of candidates, with @MeteoraAG currently at the top. The project sits at the core of Solana’s liquidity infrastructure and directly benefited from the memecoin supercycle. According to DeFiLlama, Meteora generated massive fees from concentrated liquidity pools tied to high-volatility launches. If insiders had early access to information about pool launches, incentive changes, or coordinated liquidity shifts, that would be a textbook case of internal data abuse. Add the broader narrative around Solana ecosystem insiders allegedly front-running retail during launch waves, and Zach’s description starts to look very precise.

But many believe it could also be @Pumpfun. Even amid the broader crypto market downturn, it remains one of the most profitable platforms thanks to token minting fees. The suspicions gain more weight when you recall that WIRED reported on a class-action lawsuit against https://t.co/aA5y1SLjp8 (filed in the Southern District of New York), describing the platform as having generated hundreds of millions in revenue according to third-party analyses, and highlighting claims that memecoin platforms structurally incentivize pump-and-dump dynamics involving insiders.

Cointelegraph also reported that a judge allowed new evidence in the https://t.co/aA5y1SLjp8 class-action case, allegedly including thousands of internal chat messages from a confidential informant. Plaintiffs claim coordinated schemes involving MEV infrastructure and preferential insider access. Again, allegations are not proof — but the pattern sounds familiar: internal communications, repeated advantage, and a long-term horizon.

As for Binance, MEXC, Upbit, and Coinbase, insider trading scandals on centralized exchanges aren’t hypothetical; they’ve already happened. Coinbase had a high-profile listing-related case in 2022. Binance has faced allegations of preferential treatment and opaque ties with market makers. But Zach tends to focus on fresh, underexposed misconduct rather than well-known regulatory sagas. And while calling them “one of crypto’s most profitable businesses” would be accurate, it wouldn’t be particularly surprising.

Hyperliquid and Jupiter seem less likely unless the angle involves internal order flow or validator-linked activity. Theoretically possible, but less aligned with the phrasing about “multiple employees over a prolonged period.”

Given the current narratives and Polymarket odds, I lean toward Meteora or https://t.co/aA5y1SLjp8 as structurally the most plausible targets. Both operate in environments where internal informational advantage can be quietly monetized at scale. And if Zach is hyping this investigation in advance – which he rarely does – the evidence is probably substantial.

Which project do you expect to see in Zach’s next investigation?

Gold and silver hit fresh ATHs: silver above ~$110/oz and gold near ~$5K 📈

This rally highlights renewed flight-to-safety demand amid rising macro risk, and we’re seeing it pressure risk assets, with BTC & alts trading softer in response.

Safe havens back in focus.

📆 Economic Calendar Update

Big week ahead!

⚡️ Jan 21: 🇺🇸 U.S. President Trump Speaks, 13:30 UTC

⚡️ Jan 22: 🇺🇸 GDP (Q3), 13:30 UTC

⚡️ Jan 22: 🇺🇸 Core PCE Price Index, 15:00 UTC