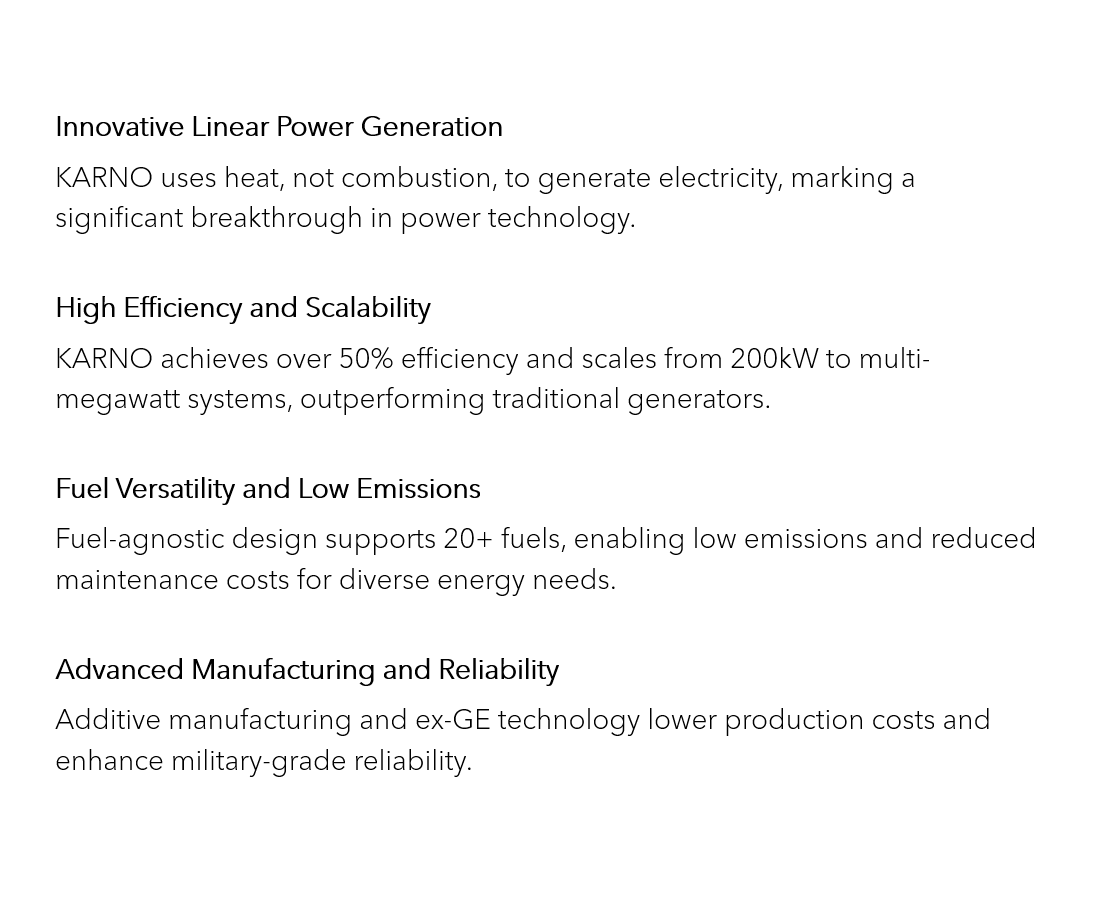

Below is my long thesis on Hyliion $HYLN

I'm personally invested in their KARNO project as I believe the next few years bode well for the company.

@Ssaasquatch you may want to have a look.

FYI: this is not investment advice.

If you have money, this is the time to lock into Bitcoin. Don't say I didn't do anything for you. For those aggressive buyers in the Project31, I see you... I see your hands.

lol the $5m cheque is after 4 years of bootstrapping TeamApt with his own money.

Part of why the investment came is they had done work for zenith bank and when “oga” asked around he got good reviews

$ABCL has been gaining strong momentum. If you missed the significant data release in May, you may be overlooking a key shift in AbCellera’s evolution from a pure technology platform into a company with growing clinical capabilities.

Here’s what $ABCL is signalling now 👇🏽

$ABCL has been gaining strong momentum. If you missed the significant data release in May, you may be overlooking a key shift in AbCellera’s evolution from a pure technology platform into a company with growing clinical capabilities.

Here’s what $ABCL is signalling now 👇🏽

$ABCL is often viewed through an outdated lens as a pandemic-era royalty play, but that narrative is shifting. Following its May 2026 Phase 1 data for ABCL635, the focus is no longer on whether its AI platform can discover molecules, it already has, but on whether it can translate those discoveries into clinically successful, high-value assets.

With over $655 million in liquidity, the company is well funded, yet the market assigns little value to its internal pipeline. The key catalyst is the Q3 2026 Phase 2 readout for ABCL635, which will test both its move into women’s health and its ability to generate meaningful returns from its own intellectual property.

$ABCL is often viewed through an outdated lens as a pandemic-era royalty play, but that narrative is shifting. Following its May 2026 Phase 1 data for ABCL635, the focus is no longer on whether its AI platform can discover molecules, it already has, but on whether it can translate those discoveries into clinically successful, high-value assets.

With over $655 million in liquidity, the company is well funded, yet the market assigns little value to its internal pipeline. The key catalyst is the Q3 2026 Phase 2 readout for ABCL635, which will test both its move into women’s health and its ability to generate meaningful returns from its own intellectual property.

I valued SpaceX for its IPO a few weeks ago, with minimal information and a promise to revisit the valuation, when the prospectus was made public. The prospectus is public, the offering price has been set and my update is up and running. https://t.co/zRjpD1C0wv

I recorded this analysis in late May, but the core thesis remains intact.

$HIVE is evolving into an AI infrastructure company with a unique ability to fund growth through its existing operations.

With a growing fleet of NVIDIA GPUs, expanding AI cloud services, and a balance sheet that avoids excessive debt and dilution, the company is building what could become a highly profitable second engine of growth.

If the market continues valuing HIVE primarily as a crypto stock, there may be a significant disconnect between the current share price and the company's long-term potential.

Here's why I'm paying close attention

Assessing $ADUR requires looking beyond traditional pre-revenue valuation metrics and focusing on the opportunity's risk-reward profile. The company is deliberately shifting from lower-margin testing services to a higher-margin global licensing model.

The downside appears relatively well supported by its patent portfolio and strong cash position, while the investment case on the upside depends on management successfully turning existing engagements with major industry players into recurring royalty revenue.

It is an attractive asymmetric opportunity where regulatory requirements help drive demand, its water-based chemistry provides a competitive advantage, and its asset-light business model creates significant potential for earnings growth.

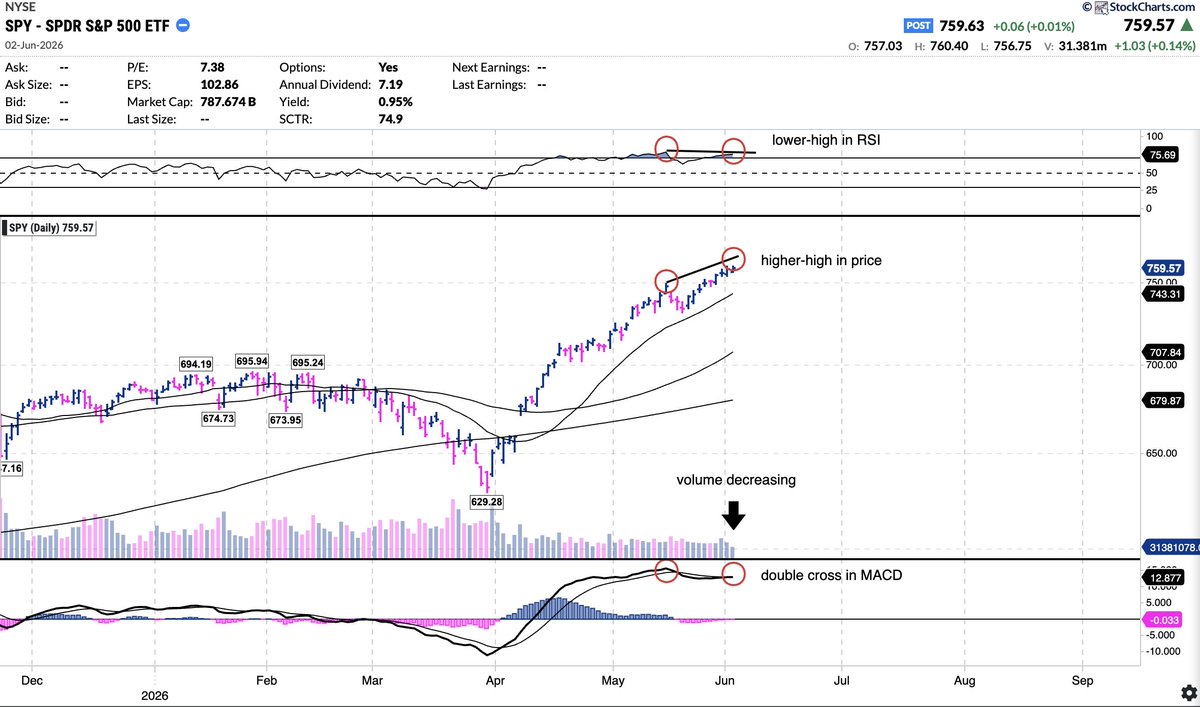

You NEED to listen to me right now.

We are in LATE-cycle territory for the overall markets / $SPY.

Bearish divergences are forming with EACH new marginal high.

VOLUME is drying up, candles are getting smaller. This is HESITATION from the bulls.

Momentum is starting to FADE.

Markets will STILL keep going up long-term, but SHORT-TERM, we're in the 8th - 9th inning.

I expect a 5% HEALTHY pull-back.

What should you do?!

1. Keep your AI-winners!!!! Trim 20% to lock-in GAINS, never sell fully. They are WINNERS for a reason

2. Look for CONTRARIAN buys. The stocks that have been LAGGING. They will go down LESS, or even outperform.

3. BALANCE your portfolio with AI leaders + AI laggards + defensives!!!!

All you need to do is SURVIVE, and you will be rewarded with the BIGGEST bull-run in history over the next 5 years.

- Keep companies and consider trimming 20% like $ARM, $NBIS, $MRVL, $MU, etc.

- Slowly positions in companies like $CRWV, etc.

- Build positions in lagging companies like $NOW, $NKE, etc.

- Build defensives like $WMT, etc.

Get ready to buy amazing companies like $AMZN, $GOOGL, and many many others soon.