Noah Holdings (NOAH K; 6686 HK), China's last independent scaled wealth manager: ~USD726m net cash vs ~USD 679m market cap; operating business for free, and a ~13% yield backed by 3 years of 100% payout. Is this a value trap or survivor?

Check our latest:

https://t.co/eq9BaZ1OJk

Tune in to our latest with veteran EM CIO Gary Dugan on why the Iran crisis is a ‘decade‑defining’ moment for EM flows. We dig into geopolitics, tech, and why forward‑looking, sector‑driven allocation is the only way to build resilient portfolios today. https://t.co/KsF6PQjZBi

Plover Bay (1523 HK), a HK-listed SD-WAN leader with zero debt, 79% ROE, 35% margins, and a 108% payout. The stock has quietly compounded to a USD 1.22bn market cap. With a proposed Nasdaq spinoff looming, can it unlock more value?

We break it down here:

https://t.co/tnpRSFJ5nS

Gas Malaysia (GASM.KL), a boring ~6% yielder with limited growth? As Malaysia gas subsidies unwind and market liberalization nears by 2030, this pipeline leader is quietly gearing up for new infrastructure plays and tailwinds.

Deep dive and KL insights:

https://t.co/ecHim5xieU

The recently IPO’d Softcare (https://t.co/n7ctwlKHOw), Africa’s largest diaper manufacturer, boasts robust local supply chains, demographic tailwinds, and solid financials. Does a +25% surge since listing leave room to run?

We break it down here: https://t.co/ky9d32YDBa

The recently IPO’d Softcare (https://t.co/n7ctwlKHOw), Africa’s largest diaper manufacturer, boasts robust local supply chains, demographic tailwinds, and solid financials. Does a +25% surge since listing leave room to run?

We break it down here: https://t.co/ky9d32YDBa

Our latest free article on the lynchpin of the solar industry: polysilicon. We argue that consolidation and rising EM demand set up the most efficient industry leaders to ride out overcapacity and cash in long term on converging supply and demand.

Link:

https://t.co/HZ6idrGfvZ

I have just published a long blog article, one of my better ones (I hope):

"Private Equity/Credit: The Bubble and its Implications"

Link in the appended tweet.

Special thanks & credit goes to Dan Rasmussen, whose excellent insights on private equity I leaned on heavily (@verdadcap), and integrated with my own work. I find Dan impressive and suggest you check out his work (he has many great interview on YouTube).

Cheers

LT3000

(7/7) The key takeaways are that trade conflict is much about tariffs as tech sovereignty, and financial markets can force US policy pivots. Gold shines regardless of tension/inflation. Non-US stocks offer value; EU is relatively inexpensive and Asia offers growth+rate cut room.

(1/7) Recent low volatility in markets has paved the way for vulnerability. Trump's vow for 100% duties on Chinese goods re-igniting full-blown trade war led markets to quickly adjust for renewed friction amidst global growth cooling off.

(6/7) TACO (Trump always changes opinion) principle still applies. China called rare earths a security response. Tones have softened over the weekend with Trump hinting at talks resuming. Sell-off has been contained so far except for the most speculative markets (i.e. crypto).

Indonesia's plastics industry may lack the shine of EM hotspots, but Panca Budi (PBID.JK) is a lean local leader with a grip on traditional markets and a distribution moat in this huge market. An undervalued powerhouse in a quietly booming industry?

Link:

https://t.co/R7Jj08qoHd

Amidst the blur of copious ceremonial toasts, a recent trip to Shandong unearthed a quietly compounding plywood manufacturer adeptly navigating overcapacity. Environmental tailwinds, rural reach, and capital discipline make this one worth watching. https://t.co/lyonMAlrsf

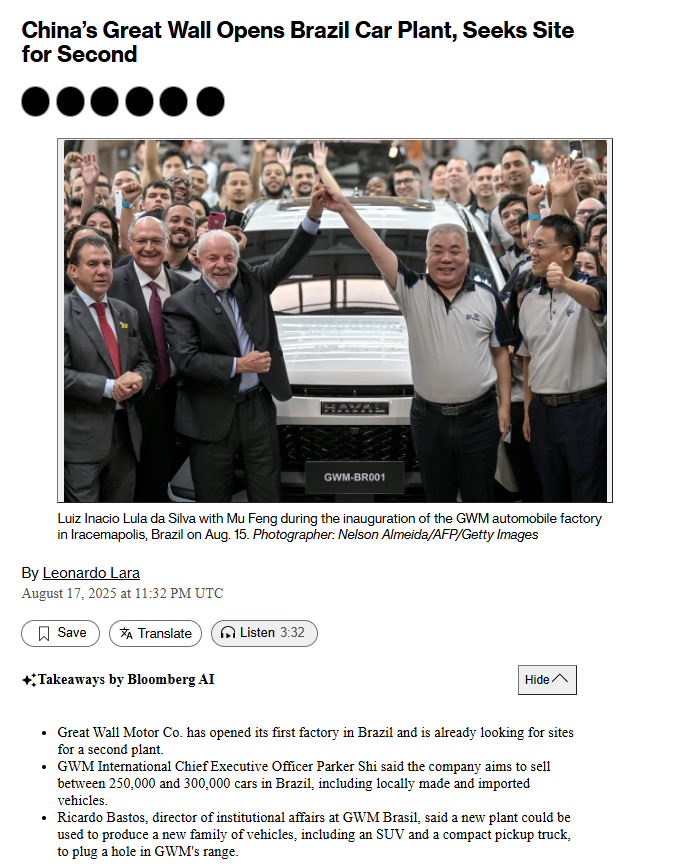

(5/5) Same strategy playing out in Uzbekistan, Indonesia, Malaysia. GWM is de-risking its global footprint and building tariff-resilient supply chains, boosting our long term confidence in the stock.

(1/5) Big news for Great Wall Motor (https://t.co/HgdSg6ohUV), which we initially bought due to robust Russia exports (search article in our Substack). Trade performed well short term but Russia sales have since slowed and stock went sideways. Why are we still bullish? 🧵

(4/5) Local production means GWM can export across LATAM while sidestepping rising tariffs on China-made vehicles. Brazil’s EV import duties will hit 35% by 2026.