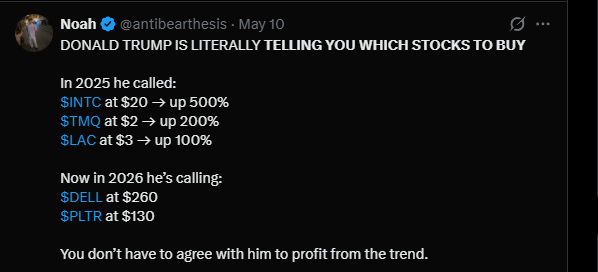

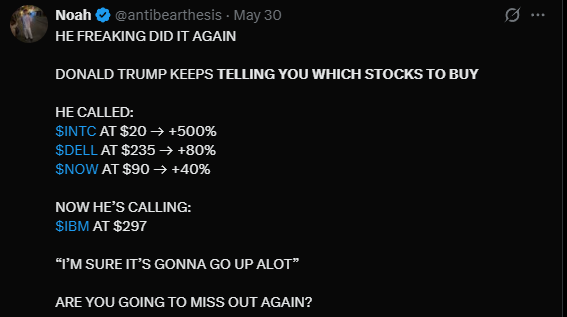

It’s genuinely scary how formulaic FinX has become over the years.

"Trump / Jensen / Aschenbrenner literally told you what to buy....

"I'll say this once: the following stocks will make you a millionaire in 5 years...."

The same names are being pumped again and again with zero explanation and no discussion of the risks involved.

Even the bots are following these patterns, herding their engagement farms, now with PAID subscribers.

Your bullshit radar is now more important than ever. If it isn't properly calibrated this will end in tears.

Recently started a new position into $CCJ.

I see Cameco as a picks and shovels winner in the nuclear energy bottleneck.

Some things I like:

- largest publicly traded uranium producer, could be a good way to position oneself if nuclear turns out to be the next super cycle after AI, especially considering the structural uranium shortage

- Westinghouse stake contribution, as a downstream asset, makes it more than just a mining stock but rather a nuclear services co

- many of its long term contracts were signed before the current uranium bull market so any spot price strength or new orders flow straight to $CCJ's margins

-management knows when to curtail production in response to tightening spot supply

@daniel_koss $CCJ

maybe the best Physical AI bottleneck play.

You need absurd amounts of reliable power. Nuclear is becoming the clean baseload answer, and Cameco gives you uranium + fuel services + a 49% stake in Westinghouse.

@ZekeHolyland בוא כל הבלוג שלך מלא בהפניות לחשבונות מסחר עצמאי בבתי השקעות, שמממנים יפה יפה את ה'פרישה המוקדמת' שלך, ברור שיהיה לך אינטרס שאנשים יפתחו חשבונות כאלה ולא ישקיעו בקופ"ג להשקעה... אף אחד לא מאמין לך זיקוש

All roads lead to Rolls-Royce $RYCEY.

I keep coming back to this name because I’m not sure the market has a clean mental bucket for it anymore.

It used to be a broken aerospace name with a post COVID recovery story and a repaired balance sheet. But that story feels too narrow now, because the same company is sitting in several strange places at once:

1. Trent engines on major widebody aircraft, where the real economics are the next 30 years of service.

2. mtu power systems, which suddenly look much more important in a world where hyperscale data centers need backup power and grid resilience.

3. Naval nuclear, where literally every UK nuclear submarine runs on RR reactors. Also Australia is putting £2.4bn into expanding Derby capacity for AUKUS. This is extreme sovereign dependency.

4. And then SMRs, where RR has the UK Wylfa contract and the Czech Temelín track with ČEZ. Still early, sure, and not risk free, but also not some PowerPoint nuclear startup with no industrial memory behind it (e.g $OKLO).

So you have aerospace, defense, nuclear, power systems and sovereign infrastructure bundled into one awkward ticker.

Last month CEO affirmed 2026 guidance and the stock barely moved. Maybe that’s fair after the huge run. But I still think this is one of the more unusual industrial setups in the market right now.

Fully exited $MA today.

Sad to see it go honestly... Mastercard is still a world-class business.

60% operating margins.

175 billion transactions a year.

A toll booth on the global economy.

But look at this chart.

$MA over the last year: -14%.

S&P 500 over the last year: +25%.

That's a 39% gap on a stock I was holding while the rest of my portfolio was ripping... I don't care how good a business is. If it's underperforming the index by nearly 40% over a year, that capital needs to be somewhere else.

Opportunity cost is real on this one - every pound sitting in $MA was a pound not compounding in $NVDA , $AVGO or $CAT

This is probably the hardest lesson in investing.

Letting go of a stock you love because the numbers aren't working - Your feelings don't make you money. The data does.

Never sell unless the thesis breaks? Sometimes the thesis is fine and the stock just isn't performing at all, even on a longer timeframe - That's enough.

Good company, wrong timing so my capital is redeployed elsewhere.

What's a stock you've held onto for too long?

The GFC was a credit/housing/banking crisis it was not "caused" by oil you fool. Also comparing today's $110 oil to 2008's $147 without accounting for inflation, wages, shale supply, SPR policy, USD strength, interest rates, bank leverage, credit spreads etc is just wild. So dumb and hysterical as usual.

Bought the $META ER panic. Still think Meta is one of the clearest AI application layer winners. It's an ad company, a very good one, and AI directly improves ads, recommendations, Reels, content creation, business messaging, and whatsapp monetization. Then there's the Zucc factor.

$ICL up over 7% in premarket.

The market may be done viewing this as just another fertilizer company.

A bromine chokepoint for the AI era deserves a much higher multiple.

Great post.

One note though, the current Dead Sea concession expires in 2030, and there's a new legal framework tha would increase the State of Israel's share f concession profits to about 50% from 35%, partly through higher royalties. It could be that this overhang prevents the stock from getting a premium multiple.

@aleabitoreddit The Bromine price surge is partly because $ICL has been producing less in the wake of the Iran-Israel war. They can't fully capture the spike if their own output is constrained.