The Lads return for the market melt-up with two special guests! @goodalexander & @santiagoroel join the pod! 🫡

🚨 OUT NOW on @YouTube & @Spotify!

In Ep #93 we cover:

📈 Crazy Market Action!

👀 Are We In Alt Season?

💊 @pumpdotfun ICO

🏦 Treasury Companies

🍝 Pasta of the Month & More!

Full links below!

Ppl saying that pump selling spot at .004 and then buying it back at .006 is dumb are missing the new mathematics of the blockchain paradigm

The selling of spot at a discount to fair value to a diversified field of investors creates community growth and shared common prosperity

The price-insensitive buying of spot using fees creates core fundamental value in a tax efficient and harmonious way

If $500m of the Pump ICO was filled onchain then there was probably another $500m <> $1.5 billion in demand on exchange that didn’t fill and another $300m+ onchain that didn’t fill.

Estimate $2 billion+ in demand today on Pump.

I just qualified for NFT Holder airdrop on @tradedotfun_!

💎 6666 $TRADE tokens

💰 75% of fees are used to buy back $TRADE

🔥 Trade Memes, Perps & Yield all in one

Claim yours at https://t.co/SIlTes38Nc 📈

We're entering a new era.

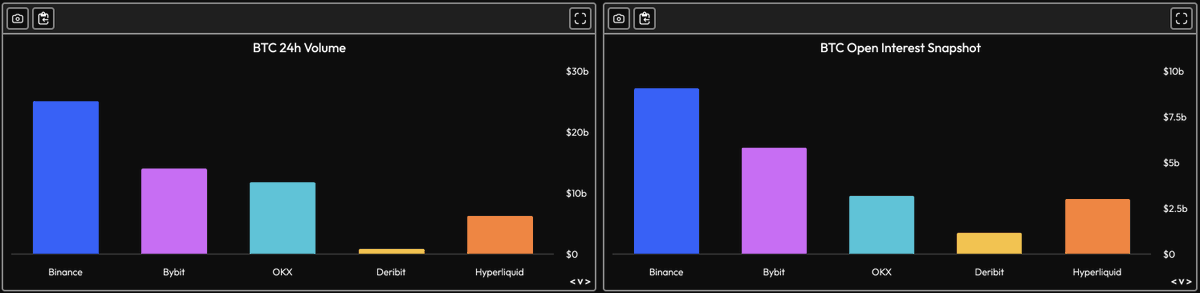

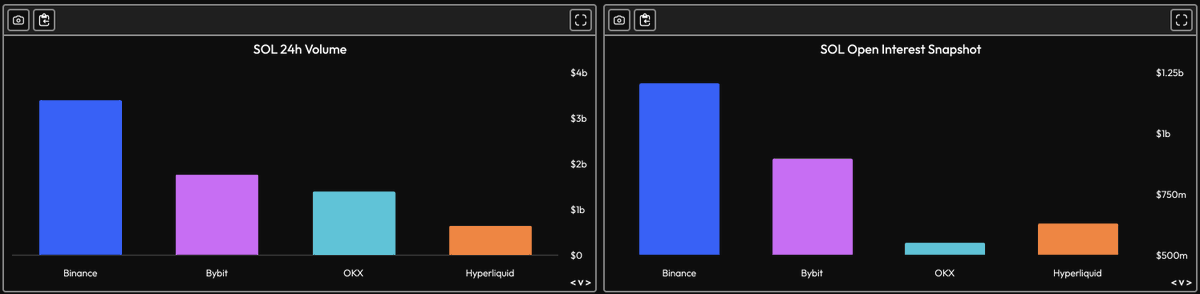

There are a few criteria in crypto markets that cannot easily be faked. Open Interest reigns supreme.

Hyperliquid has transcended the universe of Perp DEXs and has retained its spot in the world of centralized exchanges.

Hyperliquid = HyperCore + HyperEVM.

One piece of user feedback since HyperEVM’s alpha launch was to more intuitively communicate how the HyperEVM fits into the larger context of Hyperliquid. To this effect, the native pieces of the Hyperliquid execution state have been organized under one umbrella term: HyperCore.

HyperCore consists of performant native components: order book perp and spot DEX, staking, oracles, multi-sig, etc. HyperEVM is a general purpose world-computer, allowing builders to deploy code that interacts with both HyperEVM and HyperCore. Together, they form one global, composable state on Hyperliquid, secured by the state-of-the-art HyperBFT consensus algorithm. Importantly, any interaction across the Core/EVM boundary is part of execution itself. There is one unified state, with no need for bridging, proofs, or trusted signers.

HyperEVM offers builders a familiar interface to plug into the most powerful permissionless financial system in crypto. Let's walk through some concrete examples.

A project XYZ deploys an ERC20 contract on the HyperEVM using standard EVM tooling. They deploy a corresponding spot asset XYZ permissionlessly in the HyperCore ticker auction. Once the XYZ HyperCore token and HyperEVM contract are linked, users can seamlessly transfer their XYZ balance to HyperCore for order book trading. Two key improvements compared to CEX listings:

1) The entire process is permissionless. No behind-the-scenes negotiations for preferential treatment. Hyperliquid is a neutral platform for finance.

2) There is no bridging risk between HyperCore and HyperEVM. On the other hand, CEXs need to manage deposits and withdrawals through wallets that could be hacked. HyperCore and HyperEVM are one unified state.

Trading and building on the same chain is a 10x product improvement over CEXs.

Let's go further. A lending protocol sets up a pool contract that accepts XYZ as collateral and lends out another token ABC to the borrower. To determine the liquidation threshold, the lending smart contract can read XYZ/ABC prices directly from the HyperCore order books using a "read precompile." For a Solidity developer, this is as simple as calling a built-in function.

Suppose the borrower's position requires liquidation. The lending smart contract can send orders directly swapping XYZ and ABC on the HyperCore order books using a "write precompile." Again, this is a simple built-in function in Solidity. In a few lines of code, the lending protocol has implemented protocolized liquidations similar to how perps function on HyperCore. A theme of the HyperEVM is to abstract away the deep liquidity on HyperCore as a building block for arbitrary user applications.

As these interactions become available on mainnet HyperEVM, I look forward to seeing the innovative ways that builders leverage these primitives to reinvent finance. These examples only scratch the surface of what is possible.

Hyperliquid.

How to manage risk (a thread)

Lesson 1: Understand your total portfolio max drawdown

Take every exposure you have, convert it into a total return series and understand its

A. Peak to trough drawdown

B. Session level drawdown (overnight being the most relevant one in stocks, as you can’t sell overnight)

C. Daily

D. Monthly Drawdowns

Do this agnostic to any factor

Over the past 1 year, and past 10 years. Many of the instruments you have in your portfolio will not have 10 year price histories. To deal with this, put your return matrices up and find a list of proxy instruments. For example, with Hyperliquid which has a short history - XRP could be a good proxy instrument because it has a long history (back to 2015).

Key question to ask: would it be possible for me to lose more than I am willing to lose. You should assume because markets tend to break simulated values. As a back of envelope assume

Max Of (3x your 1 year max loss, 1.5x your 10 year max loss)

Important point: you need to strip out any edge your strategies have when computing this. It needs to be instrument level losses not backtest level losses

Your KPI is what % of your max drawdown you make every month. Sharpe ratio is a meaningless metric because it does not measure something real (the probability you scream into the abyss and go get a job as an accountant)

Lesson 2: Understand your key market beta exposures

The following are canonical exposures.

Tradfi:

S&P 500 (SPY)

Russell 2000 (IWM)

Nasdaq (QQQ)

Oil (USO)

Gold (GLD)

China (FXI)

Europe (VGK)

Dollar Index (DXY)

Treasuries (IEF)

Crypto:

ETH

BTC

(Top 50 alts ex ETH BTC)

Most strategies do not have explicit market timing strategies for these market betas. Therefore risks should be cut to zero. Generally the best way to do this is with futures instruments as they have cheap financing costs and low balance sheet intensity.

Simple rule: know all your risks and hedge it if you don’t

Lesson 3: Understand Your key factor exposures.

[ less important]

The following are canonical factor exposures:

Momentum

Value

Growth

Carry

These are in practice much harder to capture — you can use ETFs like MTUM for S&P 500 factor momentum but in practice what this factor actually means is that your entire strategy is top blasting everything. This is complicated as many times you are taking deliberate factor risk as in trend strategies

Good measures:

Average price Z score of everything in your portfolio that ISNT part of a trend strategy

Average (price to earnings) or equivalent for everything that isnt part of a value strategy

Average revenue (or fee) growth rate for everything that isn’t part of a growth strategy

Average Yield of your portfolio (chances are if you are spitting off mid teens yield by default then you have carry factor risk)

In crypto trend factors tend to unwind with the broader market because everyone does them and therefore contain hidden risk. In FX, this is true of yield strategies where “carry” is the dominant form of degeneracy

Lesson 4: Using Implied rather than realized volatility based sizing AND/or have explicit sizing parameters for different market sessions

When possible you should pull down options data for the securities you hold to predict their volatility. This is obviously the case around earnings but in more subtle situations it’s quite useful, especially around elections. One way to size is

(Implied vol / 12 month realized vol) * 3 year max drawdown = assumed max drawdown per instrument

Set instrument level max drawdowns. If implied volatility is not available then the instrument probably isn’t liquid which brings us to the next point

Lesson 5: Assume progressively higher cost impact in illiquid conditions (illiquidity risk)

Never assume you can sell more than 1% of the daily volume in 1 day without material price impact. If the market becomes illiquid you might own 10% of the day’s volume and that could take 10 days to sell etc etc. To avoid liquidity risk never own more than 1% of a day’s volume and if you do assume your instrument max drawdown is 2x higher for every 1% when modeling max loss (a bit punitive but trust me … yea actually I don’t even want to get into how I know this)

Lesson 6: “What is the one thing that could blow me up” / qualitative risk mgmt

All of the above is qualitative and not forward looking. At any given time we have hidden factor exposures. For example, right now anyone who is long USDCAD has Trump related tariff risks that aren’t cleanly captured in historical realized volatility because the news cycle is changing too quickly. Similarly if you ask most traders “what’s the one thing that could kill me” they usually know.

If you have a USDCAD position unrelated to your view on Trumpian tariffs then it is worth considering how to remove or reduce that risk through appealingly priced relative value trades (for example Mexican equities vs US peers etc). Most historical blow ups are actually not particularly surprising on a multi week timeframe - i.e. during the taper tantrum everyone knew it could be a problem w rate sensiitive asset for quite a while before it hit. Same story with COVID risks.

Lesson 7: clear apriori identification of risk limits in the above framework for deliberate exposures

Given a bet, what is the bet. How much am I willing to lose. How do I cut the market exposure. Can I get out of the trade if it goes against me/ do I need to size down. What could kill me

Write this down or track it somewhere

Lesson 8: have meta cognition on when you are doing this well or not

If you read this and your reactions is “Lol yea right I’m not doin all that” or “Sir this is a Wendy’s” chances are you should just cut all your risk by 1/3 or you probably shouldn’t have taken risk to begin with. Remember Wendy’s menu items are deliberately not high priced - so if treating the market as a Wendy’s you should not size like you’re going to the Ritz

I also know nobody is going to do all this and am fully aware of the futility of posting it so you don’t need to remind me of it

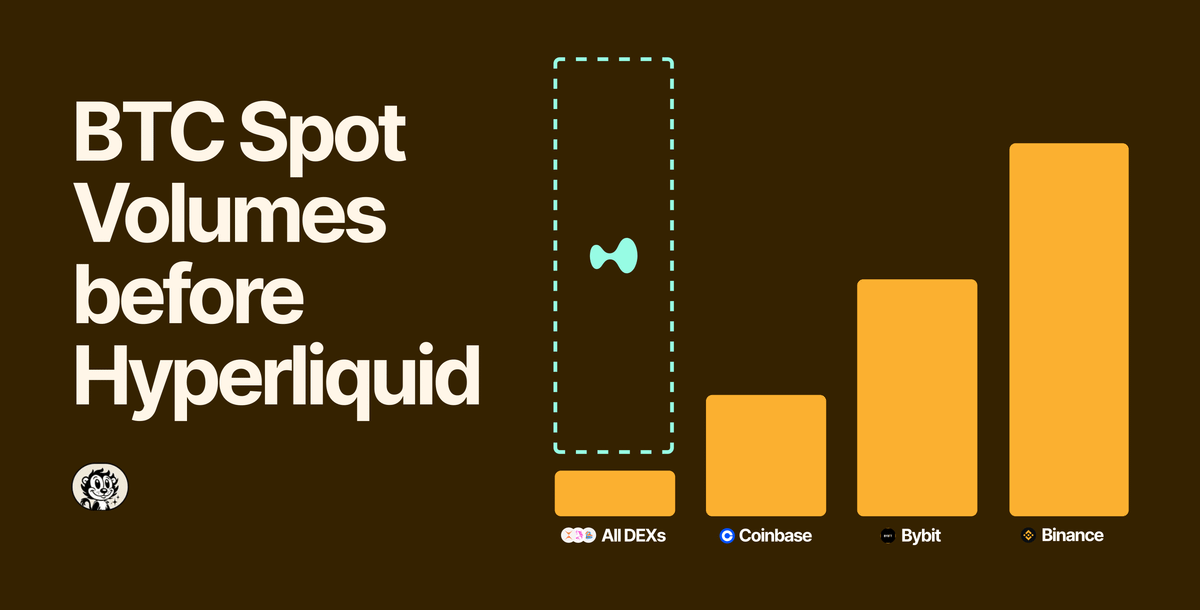

Welcome, BTC. To Hyperliquid.

This is an important step as Hyperliquid continues its dominance as an on-chain trading venue, growing beyond perps. Now, you can trade BTC on a high performance spot orderbook. Soon, you'll be able to do even more with the EVM.