Dowsure partners with the world's largest e-commerce platforms, top 10 global banks, and e-commerce merchants to connect all aspects of the e-commerce working capital business chain.

This includes risk analysis, liquidity provision, repayment mechanisms, and customer management.

By transforming e-commerce platform data points into a risk analysis system that is used by leading global banks, Dowsure provides the stringent risk management required to safeguard loans for institutional investors.

Website: https://t.co/N4mR0pNPm0

Three things have to happen for capital to meet a cash flow.

It has to be settled — the rules of who owes what need to resolve. It has to be cleared — the actual money has to move. It has to be priced — the rate has to come from somewhere.

For most of financial history, all three required intermediaries. A bank for settlement. A clearinghouse for clearing. An underwriter or rating agency for pricing. Each one added trust, latency, and a permission gate.

Dow Protocol does all three permissionlessly, against real-world cash flow.

Settlement is a smart contract. Clearing is a deduction from the flow itself. Pricing comes from the protocol's logic, applied uniformly to every participant.

This is not on-chain because on-chain is fashionable. It is on-chain because there is no other surface on which settlement, clearing, and pricing can happen for real cash flow without a gatekeeper sitting in the middle of all three.

PayFi has become a category everyone wants to be in.

Most of it is just two products glued together — a payment app on one side, a lending or yield product on the other, sharing a logo. The "fi" runs in a separate venue from the "pay."

That is not PayFi. That is fintech with adjacent rooms.

Real PayFi is the inverse. The finance happens inside the payment flow, not next to it. Yield comes from capital structurally embedded in how money is already moving — not parked beside it.

Once you draw the line that way, most "PayFi" projects fall out. What remains is a narrower question: where is there enough real, recurring payment flow that capital can actually live inside?

E-commerce disbursements are one of the few honest answers.

On-chain lending has been tried many times. Most of it has not ended well. Each protocol launched with real capital, real borrowers, and a real thesis. Each one ran into a version of the same problem.

The capital was on-chain. The repayment was not.

When a borrower agreed to repay a loan, that promise lived off-protocol. A spreadsheet, a wire transfer, a corporate treasury that may or may not still be solvent when the loan came due. When things went well, the protocol looked clean. When things went badly, the protocol had no recourse — because the cash that was supposed to come back was sitting in a place the protocol could not see, let alone touch.

That is not a protocol problem. That is the absence of a protocol on the side that matters most.

What e-commerce changes is the shape of the repayment source. The cash a merchant owes is not a future intention. It is a future disbursement — already triggered by sales that have already happened, sitting in a platform's settlement queue, on a schedule the platform has already committed to.

If a protocol can attach itself to that flow, repayment stops being a promise. It becomes a deduction the protocol observes and enforces.

This is the part on-chain lending has been missing. Not better borrowers. Not better underwriting. A repayment source that lives in the same structure as the loan itself.

The CLARITY Act is the most consequential development for on-chain credit in years.

The bill draws the line we've been operating on the right side of from day one: digital commodities and securities are not the same thing, and assets backed by verifiable, real-world cash flow shouldn't share a regulatory bucket with unsecured offshore paper.

E-commerce seller lending today still looks like a company problem.

One company sources the data. The same company underwrites, lends, services repayment, and warehouses the risk. Every piece of the flow stays inside one balance sheet. The yield it produces is private. The risk it takes is opaque. Capital that wants in has to either build the whole stack or stay out.

That is the version of this business that has existed for 20 years. It works. But it does not scale the way a protocol scales.

What changes when you put it on-chain is not the lending itself. It is the unbundling.

Platform data becomes a feed any underwriter can consume. Disbursement flow becomes a programmable settlement layer. Repayment becomes a deduction the protocol enforces, not a promise a company collects. Capital providers can underwrite directly against an observable flow, instead of buying exposure to a black-box loan book.

The merchant still gets financed. The yield still comes from real cash movement. But the structure underneath is no longer one company's balance sheet. It is a protocol that anyone with capital, data, or risk appetite can plug into.

Dowsure is the first lender running on this protocol. It is not the last.

That is what Dow Protocol is building toward — not a better lending company, but the layer that makes the next hundred possible.

A lender inside that flow is doing a different job.

Underwriting moves with platform data in real time. Repayment clears from the disbursement before it ever reaches the seller's bank. Control becomes structural — not collection.

This is what e-commerce seller lending should have looked like from the start. And it is what we are building at Dow Protocol.

Lending to e-commerce sellers looks like a credit problem.

It is actually a control problem.

The seller does not hold the money. The platforms do. Every lending decision in this space lives in that gap.

A traditional bank lending here is operating outside that gap.

It cannot read platform consoles. It cannot see account health, return rates, inventory turn. At repayment time, it has to ask the seller to wire money — money that may have been held that week, eaten by a reserve hike, or disbursed late.

This is why e-commerce seller lending has stayed underserved. Not because merchants are too small. Because the control point sits inside the platform's disbursement flow, most lenders are standing outside the door.

Clearer boundaries between user interfaces and regulated intermediation are helpful for the industry.

They make it easier to understand what different parts of the stack are actually doing, and where regulatory obligations should sit. That matters for builders, institutions, and users alike, especially as digital finance moves beyond trading into payment, settlement, and other transaction flows.

If onchain financial infrastructure is going to become more usable in practice, this kind of role clarity is part of the foundation.

STRONG staff statement from the SEC today laying out that “covered user interfaces” *do not* need to register as a broker-dealer when UIs—including self-custody wallet interfaces—display quotes and execution routes to the user, “selects one or more default trading venues,” charges a fixed fee based on objective factors, and other circumstances listed.

The DEF team is grateful to the SEC Crypto Task Force for this much-needed guidance, and for engaging with digital asset industry participants as they develop regulatory frameworks that enable and incentivize innovation.

We look forward to continued collaborations with the SEC, as we are hopeful this staff guidance can be codified into a durable rule or law.

The more important point here is not issuance itself, but whether digital money can fit into real payment flows.

That comes down to standards. If acceptance, messaging, reconciliation, and settlement can work within existing operations with less friction, new infrastructure becomes much easier for institutions and payment providers to use in practice. That is when it starts moving from concept to actual financial activity.

The ECB has signed agreements with three leading European standard setters to facilitate digital euro online payments.

By reusing existing standards, we can help private European payment solutions minimise costs and increase their geographical reach https://t.co/iktYHKCDz5

That is why this is not just about adding capital.

It is about getting operating data, cash movement, and repayment into the same structure.

Once that happens, the flow becomes much easier to work with.

E-commerce financing often gets described as a funding gap.

Often, the more challenging part is not the money itself.

It is whether the business can be read clearly enough for capital to price the flow with confidence.

Sales alone do not do that.

Revenue, refunds, disputes, settlement timing, and payout patterns all change how a merchant should be understood.

If those signals sit in different places, underwriting stays rough and control stays weak.

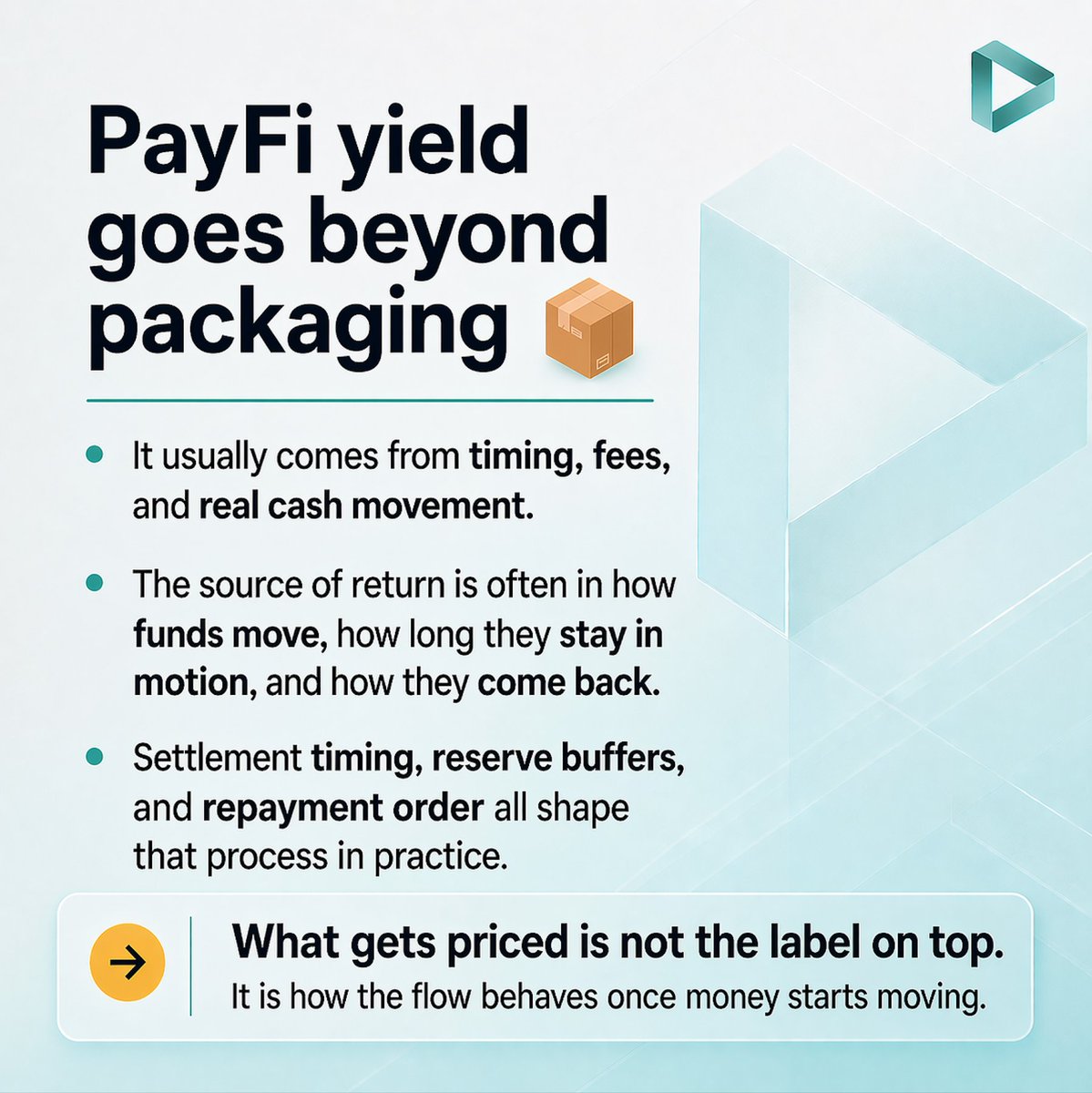

PayFi yield goes beyond packaging 📦

🔹 It usually comes from timing, fees, and real cash movement.

🔹 The source of return is often in how funds move, how long they stay in motion, and how they come back.

🔹 Settlement timing, reserve buffers, and repayment order all shape that process in practice.

What gets priced is not the label on top. It is how the flow behaves once money starts moving.

A useful reminder that payment friction is often structural.

If cross-border payment flows are still constrained by cost, speed, transparency, and interoperability, better packaging will not solve whether capital can actually work against the flow.

A flow does not become easier to finance because it sounds cleaner on the surface. It becomes easier to finance when the structure underneath actually works.

Cross-border payments remain costlier, slower, less accessible and more opaque than domestic payments. Limited interoperability is a key constraint, which public sector collaboration can overcome. Learn more in our #BISPaper: https://t.co/2UBtqgqGLg

Financial activity is no longer being shaped only through traditional bank balance sheets.

As more financing moves through non-bank channels, what matters is whether the underlying payment and settlement flows are clear enough to track, manage, and finance over time.

That becomes especially important in models where repayment depends on actual transaction behaviour and receivables, rather than a one-time credit decision.

How are non-bank financial institutions reshaping global banking?

Find out in our data story below, and discover more in our recent research: https://t.co/WChFWMio5r

#BISDataStories#BISStatistics#DataStories

Digital commerce is scaling fast 🌍

🔸 Global B2C ecommerce revenue is projected to reach $5.5T by 2027.

🔸 Cumulative global online payment fraud losses are expected to exceed $343B between 2023 and 2027.

Scale is growing.

That does not make payment flows easier to work with.

More commerce does not mean less friction. It means structure matters more, which is exactly where DowProtocol is focused.

What makes these flows interesting is not just volume.

It is the context behind them.

Revenue, transaction history, refunds, and disputes can make two similar-looking merchants very different in practice.

That delay in payments from E-Commerce platforms comes from:

- Settlement cycles

- Refund windows

- Disputes

That is part of what Dow Protocol is built around.