🚨 $AAOI options flow, the whole story.

FinTwit is melting down over one $540K put bought today, calling it the smart-money bear signal.

So I pulled every print over $475k this week (June 15-June 18.) The tape is NOT bearish. It’s overwhelmingly BULLISH🟢 and the put everyone’s panicking about is a lottery ticket. 👀

Let me walk you through it. 🧵

LMAO, $sats liability is GONE. GONE! 😎

Just in 30 mins ago.

TLDR:

🔸$sats owe FCC $2.9 Billion.

🔸If Auction 113 raises ~$2.921 billion or more, EchoStar owes $0

It’s $3.1 Billion now 😎

Project out the rest of the spectrum echostar owns. Markets are pricing in ZERO 😂

Once in a blue moon, market hands you free money.

Do a simple search on $sats and the amount of attention is stock getting is minimal.

This is what you want.

When consensus agrees, you get out.

Why I went all in $SATS

Here’s the maths:

SpaceX IPO at $135

SpaceX S1 disclosed Echostar owns 261.8 million shares

🔸$135 X 261.8 million shares = $35 Billion

While echostar was worth less than $35 Billion yesterday

Question:

Do you really think that you can put a $135 limit order on ipo day to get the shares?

NO!! Hyperliquid premarket AT $180 already 😂

Your best chance is do a market order buy on $sats before spacex ipo if you are bullish on spaceX

Here is where it gets crazier:

FCC APPROVED deal $22.65 Billion Cash for selling low to mid-band spectrum to AT&T

🔸So that’s worth ZERO? or NOBODY FKING CARED LMAO

My valuation ex- spaceX:

Net cash after debt paydown

$8.5 billion

Remaining unsold spectrum

$10 billion

Core operating business

$10 billion

Total Ex-SpaceX $28.5 billion

🔸Value per share EX- SpaceX ~ $86 ( Conservative )

Now let’s go from crazier to NUTS:

Short interest is 31% !!!! WTF LMAO

But the issue is founder owns 50.5% stake and 86.8% voting rights.

So the short interest on the remaining whatever available float? What’s that? 60++++%???

Seldom market hands you free money. When it does, go all in.

____

P.S. I seldom write long thesis anymore. Why? The hardworking ones will be rewarded with their own DD. You make your own conviction rather than relying on me for customer support.

And what do you want more when I put my own $$ on the line? Who does this transparently? Action speak more than words.

Once in a while, I'll write. But don't count on me mansplaining often. It's better for you to build your own conviction.

New $IREN Deep Dive

Our new $IREN deep dive is finally live!

It's honestly the most comprehensive report we have ever released and something I'm firmly convinced will age like fine wine.

Even though it goes into great depth, it's written in a way that virtually every investor can understand. I purposefully went light on industry and finance jargon, and whenever I did use technical terms I made sure to explain them properly.

This time around I've also unlocked the entire first chapter for free Substack subscribers to read.

So if you're on the fence, I encourage you to read the first pages to get a sense of the depth and analytical quality you can expect from the rest of the deep dive.

I'm sure every $IREN shareholder, analyst, or investor curious about the company will derive great value from this deep dive.

I very much appreciate everyone's patience. This one took a while.

Enjoy! ✌️

https://t.co/HUkfni8Ltf

$IREN I think people are missing the bigger picture a bit here.

The NVDA rights only vest as 600k GPUs are actually deployed, so it’s not like IREN just handed away value upfront for nothing. NVIDIA only really benefits if IREN successfully scales.

And NVDA isn’t just some passive investor. They influence chip supply, deployment timelines, technical support, customer conversations, ecosystem credibility, and even financing confidence. That alignment can materially impact both the probability and pace of value creation.

Also worth thinking about the counterfactual. What is IREN worth without this level of NVIDIA alignment? The AI infra space has other players trying to scale into the ecosystem. Having NVIDIA strategically aligned potentially creates a real competitive advantage around access, execution speed, credibility, and customer acquisition.

Keeping 100% ownership of a slower, less certain path isn’t necessarily better than owning slightly less of a platform that scales much faster and more successfully.

So the real question isn’t just dilution in isolation, it’s whether partnering closely with NVIDIA meaningfully increases the odds of IREN becoming a top-tier AI infrastructure platform. I think it clearly does.

CONGRATS TO TEAM IREN!

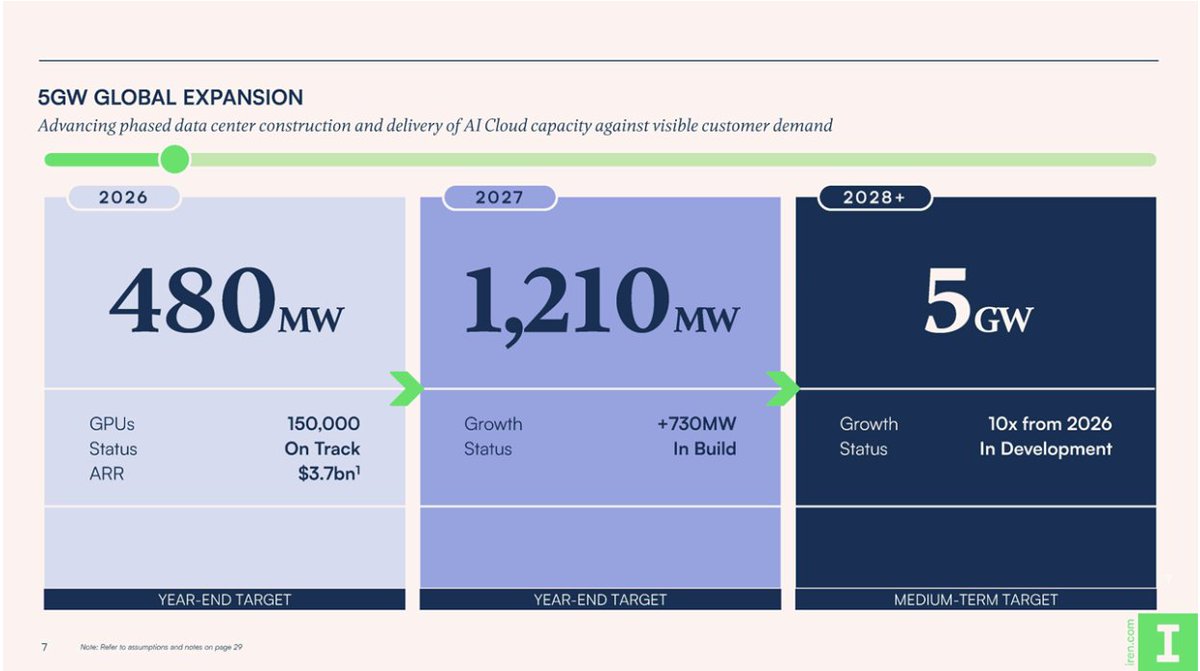

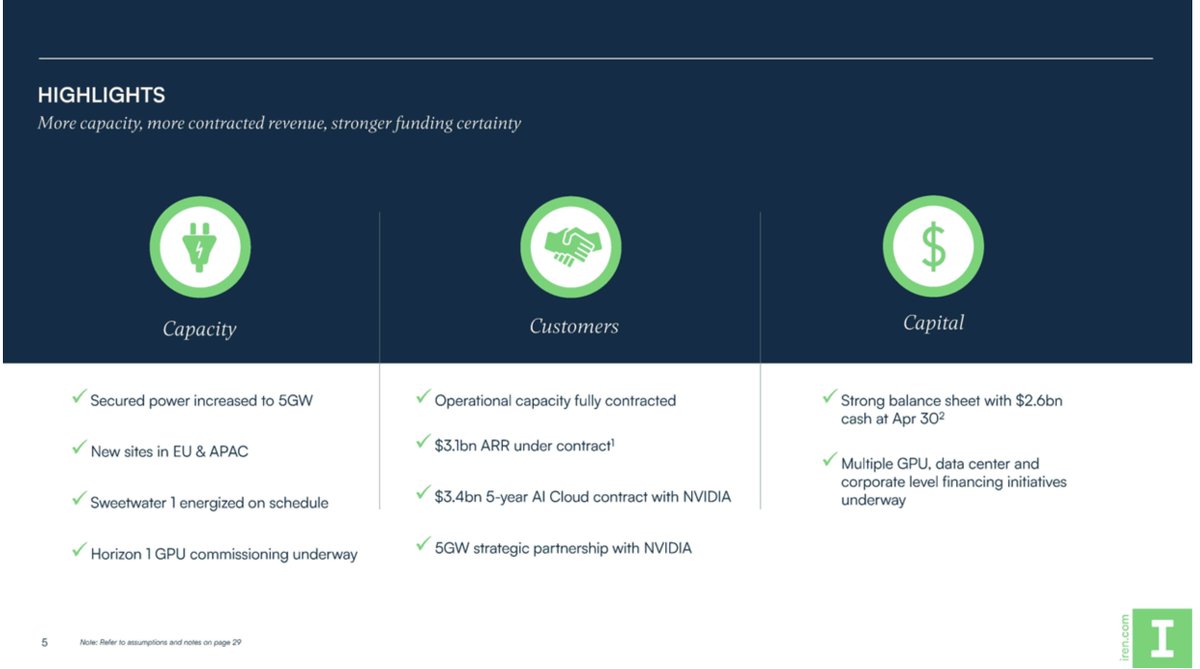

$IREN: First look at Q3 FY 2026 Earnings

Quick note - why is IREN giving back all it's gains from $72 -> $60? 1. CRWV had bad cost numbers and whole Neocloud sector is following it's 10% dump. 2. Reason I explain in takeaway 3.

Takeaway 1 - Nvidia Contract Economics

Nvidia 3.4B/5-year 60MW GPU compute contract with IREN for internal research usage.

- This is at 11.3m/MW which is 16% increase from 9.7m/MW MSFT contract. This is very meaningful top line increase given this is for air-cooled which means B300s. Much more profitable than MSFT contract and the topline IREN needs.

Takeaway 2 - Why is IREN Expanding Slower than Expected

Each GPU generation has greatly improve performance and economics. IREN has a "good" bias from the bitcoin mining days where it was a late move in order to have a fleet that was heavily skewed towards newer ASICs.

Technology moves very very fast in the beginning and AI GPUs are still considered early, IREN is trying to time where most of it's fleet is mid-stage GPU aka Vera Rubin or newer. Hence it's SW1 buildout is pushed out to 2027 so that it will be all Vera Rubins.

Yes, IREN is still scaling out it's DC buildout teams as this is all external and not contracted out like CRWV/NBIS. CRWV/NBIS for 2026/2027 capacity relies on 3rd parties and NBIS greenfield sites starts 2028. This is why IREN is full funded already for 2026 based on operational cashflow, existing cash on hand and has the Nvidia investment coming in later while NBIS still has 2026 funding needs even after the large convertible and Nvidia investment. Less aggressive but also less capital intensive.

CRWV/NBIS is your investment if you want to expand as fast as possible. IREN cares about unit economics and having a VR200 and newer generation fleet. IREN selects customer based on ability to get financing at best interest rate and has better rate on their convertibles than both NBIS's convertible and CRWV's corporate. Given corporate debt is apple or oranges but 9% on CRWV is meaningful enough to compare to IREN's 0% and 1.5% converibles and 6% GPU debt financing.

Takeaway 3 - Nvidia Option to Invest Instead of Immediate Investment

Market sees this the reason to sell $IREN back down from $72 -> $60. Whereas $CRWV and $NBIS got the money immeidately for shares at market price because they have 2026 unfunded needs, $IREN is fully funded for 2026 and would rather sell at above the market price. The way to negotiate this is to have the shares sold in the future at a premium at which the negotiations happen. Nvidia negotiations were happening today, they were happening when IREN was in the 40s so 70 is a significant premium. YtD relatively IREN at 70 is equivalent to $NBIS issuing shares to NVDA at 140.

IREN does not need the 2.1B in 2026, why dilute at $40? IREN will need cash in 2027 where it's buildout is going to accelerate so IREN is it then.

The important part is getting priority on Nvidia's delivery schedule. Nvidia does benefit by having the right to buy IREN stock through 2031 at $70 but everyone, everyone is paying alot to secure HBM which is on-chip with the GPU. This $70 call option for Nvidia is good for 600k GPUs.

Full Points

- 3.7B 2026 ARR runrate and 3.1B ARR already contracted. This means the Mackenzie GPUs are contracted! All the Prince George GPUs are contracted.

- New site in not only EU but APAC! Australia confirmed.

- 2.6B cash on hand. People can stop talking about the ATM for current liabilities out now. ATM is for future growth/deals/acquisitions.

- Will provide 3.4B of AI Cloud compute to Nvidia. Not counted in the 3.7B ARR so likely 2027. IREN is selling GPU compute to Nvidia internal teams!

- IREN secures 600k GPUs of Nvidia GPUs as part of partnership. Nvidia has right to buy $IREN at $70 as it delivers the GPUs to IREN, full $2.1B investment option upon delivery of 600k GPUs.

- 480MW by 2026, 1.21GW by 2027, 5GW by 2030. Nvidia GPU secured, power long secured, deals will come.

- H1 handoff in Q3 CY 2026 is kind of disappointing. Handoff will likely be early Q3 as burn-in already happening now. H2-4 will be handed off by this year is the important part. There must have been some snag in H1.

- Rest of Childress will be split among 100MW IT of liquid cooled H5-6 (likely extension for MSFT) and 250MW retrofit of air-cooled capacity.

- @FransBakker9812 spot on - First SW1 200MW IT will be in 2027 and be for VR.

- AI Revenue 33.6m is lower than expected as commissioning GPUs slower than expected. Will expect this to speed up as IREN ramps up their in-house team.

@realroseceline Thank you for sharing your thoughts. Please don’t mind the haters or people who constantly argue against everything. There’s always people who are bullish and those who are bearish. That’s what makes a market. Thank you for what you post and share. Please keep it up!

My $ETH strategy is pretty boring.

I try to accumulate when prices are below the mid point of this channel.

Don't wanna be the guy to let my wife or my future kids down.

Precisely my thought.

I went long GPZ last week because the narrative on private credit has been overly bearish when the story isn’t as simple, and the risk-reward is now more attractive.

Thanks for the confirmation!

@SouthernValue95

Fool me one, shame on you.

Fool me twice, shame on me.

Trump’s comments getting less and less “euphoric” reaction each time.

There needs to be a definitive resolution.

AND THE JAWBONE

Crude "only" fell ~$4.50/bbl on the latest Trump post, which is less than 1/3 of the pullback he got on Monday, and the rout was reversed much more quickly.

Oil market getting more numb to the nonsense.

Seven dogs stolen from their owners have gone viral after escaping their captors and making their way home

The group is believed to have travelled around 17 km together led by a corgi across highways and fields

How to buy $2,400,000 for $100,000

1. Buy 50 $ETH at $2,000 for $100,000

2. Stake the 50 $ETH

3. Earning 1 free $ETH per year In staking

4. Wait 10 years and you have 60 $ETH

5. In 10 years $ETH is now $40,000

6. You now have $2,400,000 and $400,000 of it was from staking $ETH