The way Ethereum charges for gas is being rebuilt. EIP-2780 and EIP-8037 now flip state pricing to a simpler rule. You pay when the work happens instead of upfront with a refund later.

Also in this week's changes, transactions that run out of gas mid-setup land onchain and revert instead of disappearing.

Issue 009 covers all six revisions. Check it. 👇

https://t.co/wbpbS9UG8Z

In my opinion, Ethereum L1 revenue fees should stay low to foster growth. Tens of thousands of companies will set up shop over the next 2-3 years on some mix of Ethereum L1, L2s, and private permissioned EVMs like Besu chains which will be fully interoperable with L2s and L1s. Monetary premium will grow very large, "fee revenue" to L1 from so much activity will grow significant, staking and other locking away of ETH will reduce supply, and net burning of ETH under ultrasound conditions will further grow the value of ETH.

1/ Today, the Global Policy Strategy (GPS) team is publishing Ethereum Basics for Governments and Institutions, a non-technical primer to equip the leaders making policy and deployment decisions with an understanding of how Ethereum works, how it's governed, and how it compares with perceived alternatives.

Tomorrow, your path to Devcon 8 opens.

Your chance to join the Ethereum community in Mumbai is almost here, with GA tickets and additional discounts available for eligible attendees.

From privacy breakthroughs to AI agents and institutional rails, the Ethereum ecosystem keeps shipping.

Here are 22 things the ecosystem delivered over the past few weeks.

0/ @gnosis_ and partners introduced The Ethereum Economic Zone (@etheconomiczone), a framework to unify the L1 and L2s into a more composable system with better interoperability.

1/ @aztecnetwork Alpha went live, a feature-complete privacy stack built natively on Ethereum.

2/ @aave V4 was released with a new hub-and-spoke architecture with support for over 20 assets across three initial liquidity hubs.

3/ @PrivacyEthereum released Social Recovery SDK, a wallet recovery model where trusted guardians can help restore access if the owner loses their private key, replacing seed-phrase backups with programmable onchain policy.

4/ Post-quantum wallets launched on @Starknet. A path to quantum resistance without address changes or hard forks.

5/ The @ethereumfndn's Board released the EF Mandate. This document, which was first intended for EF members, reaffirms the promise of Ethereum, and the role of EF within this ecosystem.

6/ Private transfers are live on @Scroll_ZKP. You can now send funds privately onchain, advancing default user protections and confidentiality.

7/ @base introduced Batches Cohort 003. 12 teams were selected from 1,100+ building across AI, DeFi, payments, and prediction markets, pushing forward OnchainApps.

8/ @ethereumfndn launched pq.ethereum (dot) org. Supporting coordination and research in post-quantum cryptography. Two breakthrough papers progressing research on PQ, with input from Ethereum researchers, were also released.

9/ Stablecoins on Ethereum hit a new ATH. Supply surpasses $180B, up 150% in 3 years, with ~60% market share globally, reinforcing Ethereum’s role in stablecoins and DeFi.

10/ @Morpho launched Morpho Agents (beta), allowing users to integrate lending into apps via natural language using AI agents and accelerating the convergence of DeFi and AI.

11/ @thedaofund deployed $1M+ via an Ethereum Security quadratic funding round hosted by @Giveth, funding work to strengthen security across the ecosystem.

12/ Deposit time from L1 to L2s and exchanges can now be as low as 13 seconds due to the new Fast Confirmation Rule (FCR). This new industry standard can be adopted by the ecosystem over the next few months.

13/ @hinkal_protocol launched Hinkal Pay, end-to-end confidential payments where sender, receiver, and amounts remain private.

14/ @peerxyz launched Peer Verify, allowing users to prove their identity, in a privacy-preserving way via ZK proofs.

15/ @ensdomains integrated with PayPal, allowing users to send funds cross-border using ENS names instead of addresses.

16/ @AskVenice shipped verifiable end-to-end encrypted AI, introducing privacy systems that can be externally audited and proven.

17/ @safe released Safenet (beta), a pre-execution security layer for Safe wallets that runs before transactions execute onchain.

18/ @SiloFinance launched Silo V3 for safer lending markets in DeFi. The team rebuilt core assumption behind lending so collateral does not need to be sold to keep markets solvent.

19/ @coinbase announced x402, an initiative to establish the x402 protocol as a universal standard for AI-driven payments, is moving under the Linux Foundation to ensure vendor-neutral, community-governed oversight of the protocol.

20/ @zksync introduced The Cari Network, a new platform to bring tokenized deposits onchain, developed alongside five regional banks and powered by ZKsync’s Prividium.

21/ @EthCC completed their 9th annual event in Cannes with attendees from across the industry. @ETHGlobal hit a milestone with their 300th event following ETHCC, continuing to support builders across the global ecosystem.

Here's a glimpse of our last weekend.

A few of us gathered to discuss Ethereum ecosystem and the exciting direction it's heading towards.✨

We watched some good highlights from ETHConf and DappCon, and shared our perspectives over chai & snacks.

Thanks for joining us. 🌿

The Ethereum ecosystem has been evolving rapidly and it’s an exciting time.

We are seeing a maturing ecosystem that’s getting ready for the next big phase. ✨

And now is exactly the time to talk about what it means for all of us.

Join us this weekend in Bengaluru! 🌱

https://t.co/v05uzHmmin

ETH and the institutional adoption of Ethereum and its ecosystem on stage at @WebX_Asia – with @davwals and @fundstrat. Thanks for having us!

#WebX2026

This is the demand shift we've been building for. Real businesses choosing Ethereum L1+L2 gives you the barbell described in the article — neutral base, specialized edges. It's the model working as intended. But there's a step past settlement.

Many L2s anchored to one L1 still fragment: separate liquidity, separate state, connected only by async bridges. A common base isn't automatically one economy.

That's the layer EEZ works on — synchronous composability across L2s, so the edges transact as one economy instead of islands, while the base stays neutral and uncapturable.

Consolidation at the base is the setup; composability across the edges is the payoff.

- Robhinhood + Arbitrum plugged an L2 into Ethereum with ETH as native asset

- Credit Agricole launched a Euro stablecoin on Ethereum

- JPM now has $1bn+ of tokenized cash on Ethereum and L2s

- UBS built compliance tooling on Ethereum mainnet

Ethereum is the world computer.

Every Devcon arrives at a different moment for Ethereum.

This year, we gather in Mumbai to refocus on the principles that unite us, strengthen our shared purpose, and build toward what comes next.

Devcon 8 tickets are available on July 14, mark your calendar.

There's a general sentiment that crypto isn't at the cutting edge anymore and working in this industry doesn't confer the same learning benefits it used to

I think those people are working in the wrong niche of crypto. Crypto is still a place to be for formally verified software, zero knowledge & incentive design

1. formal verification software is big for AI as a reinforcement learning playground & as more secure code that can't be hacked by godlike LLMs. Crypto is leading the field (although we didn't invent it) because of how much safer funds can get with it. Building smart contracts in languages like lean are the frontier to be at now

2. Zero knowledge is key for enabling collaboration b/w people or entities that don't want to share their actual data. We are seeing this become more important where LLM models trained on data across corporates is better for all, but no one wants to share their actual data with competitors. improving models without revealing the data used to train it is the forefront for zk research & ai

3. Crypto is still very much one of the leaders in incentive design, internet coordination, micropayments, governance of online communities

Trading, defi, prediction markets are already mainstream so i haven't touched on those, even beyond those there's still a lot here that would get smart people into our space

There are ~8,500 physical nodes on the network of Ethereum validators according to this new study by @alexneumueller. Meanwhile, a 2024 paper recorded ~12,000 nodes on the network, and of those, ~7,000 validator nodes (Brown, Bautista-Gomez, 2024 https://t.co/1DGCFDnKAi). This shows the numbers are not diverging much over time.

Yet, there are ~4,000,000 potential "seats" for validators to join! This matters since 1 validator = 1 message sent on the network, every round of finalisation. In the worst case, 470x more messages sent than nodes on the network..

This is a very large overhead that currently stands in the way of achieving faster finality. Today's economic finality is achieved after ~15 minutes. This often means that capital cannot interoperate freely during these 15 minutes, or if it does, it must do so using more brittle assumptions, raising either cost of capital or risk.

(Sidenote: The Fast Confirmation Rule strikes in our view a good tradeoff between speed and security assumptions. https://t.co/jhoPRgtJu8)

Ideally, 1 validator = 1 node = 1 message. With 8,500 validators only, finality would be achieved within seconds, while preserving fidelity of the signal: Every unit of staking ETH would still be casting a vote on finality.

Thankfully, with the introduction of MaxEB, the number of validators peaked at ~1,100,000 in summer 2025, and has been trending down since, sitting at 880,000 validators today. This number must continue to lower if we are to achieve fast finality.

Job's not done 🫡

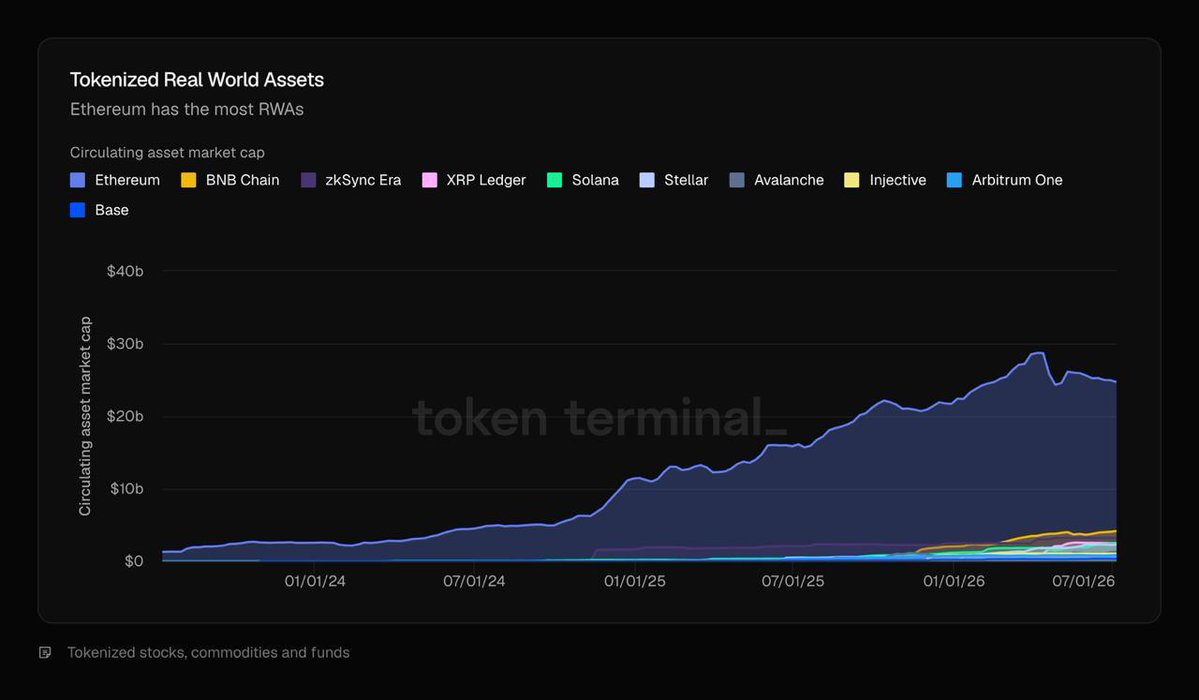

Ethereum L1 hosts ~$25B in tokenized assets.

More than any other public network, before even counting its growing L2 ecosystem.

That concentration of live assets, combined with Ethereum’s proven resilience, liquidity, and institutional ecosystem, is why the world’s largest banks and asset managers keep choosing Ethereum.

Banks:

→ JPMorgan

→ Bank of China

→ BNP Paribas

→ Crédit Agricole

→ Santander

→ UBS

→ Société Générale

→ Morgan Stanley

→ Standard Chartered

→ BNY

→ ANZ

→ European Investment Bank

→ ABN AMRO

Asset managers:

→ BlackRock

→ Fidelity

→ Amundi

→ UBS Asset Management

→ Franklin Templeton

→ Wellington

→ Apollo

→ New York Life

→ Hamilton Lane

→ Janus Henderson

→ Baillie Gifford

→ VanEck

→ WisdomTree

Bonds. Funds. Stablecoins. Deposits.

Onchain. Public. Permissionless.

Ethereum.

Ethereum’s next chapter is taking shape in Mumbai, and there’s nothing like being in the room when it happens.

Devcon 8 tickets launch July 14. Save the date.

See you in Mumbai. 🇮🇳

Open Standard launched Open USD. What does this mean for existing issuers like Tether and Circle?

Tether and Circle make money the simpler way. They hold your dollars, park them in T-bills, and keep the yield. All of it. Tether made over $10B in net profit in 2025 on roughly $186B in USDT liabilities. The business is making money by holding dollars.

Stablecoins can become a $10 trillion market. That’s about 30x from where the total market is today. But it doesn’t get there with the existing use case of financial speculation. The float only reaches that level if businesses use stablecoins for settlement or other use cases.

Who wins if stablecoins go to $10T?

It’s tempting to think current winners keep winning. They are embedded everywhere in the ecosystem. USDT and USDC together control close to 85% of a $320B stablecoin market. Surely they enjoy network effects with a very solid base. It's the base pair on every exchange, the quote asset on Hyperliquid, the thing every desk defaults to because everyone else defaults to it too.

But is that enough? Especially not if the use cases we are going after are beyond speculation. Here are a few reasons why:

1. Liquidity around a base pair is not because of some sworn loyalty. Capital is mercenary. Loyalties change when incentives change. Binance proved this with FDUSD. Zero fees on a handful of pairs in 2023 pushed FDUSD's BTC volume past USDT's within a year. Whoever controls the exchange controls which stablecoin gets called the base pair.

2. Moving between stablecoins keeps getting cheaper. USDT0, the LayerZero-based version of USDT, has already crossed $100B in cumulative cross-chain volume. The technical cost of switching which stablecoin you hold is heading toward zero, which means the "everyone already uses it" argument is a perpetually weakening one.

3. Users are being abstracted away from caring at all. If we are saying that businesses will use stablecoins, they can be abstracted away from users. Once the wallet or the app has control over the underlying asset, the end user just sees dollars.

The network-effect argument in favour of existing stablecoin issuers doesn’t hold in this environment.

Tether and Circle have created and proved that stablecoin businesses can be viable. That doesn’t guarantee continued success. On the contrary, competition will get more intense. Especially if we anticipate a 30x growth in the existing market. What’s already won is much smaller than what can be won.

Netscape created the mass browser category and held a 90% share by the mid-90s. Microsoft bundled Internet Explorer into Windows, cut exclusive deals with PC makers, and took the category over within a few years on distribution, not product quality. New category, then whoever already has scale and distribution absorbs it. The twist with OUSD is that its backers aren't the scrappy new entrants in that story, they're the incumbents. Visa, Mastercard, Stripe, and BlackRock are the distribution for a $10T base. If the bigger player usually wins, OUSD's own consortium may end up winning.

Consortiums have a terrible track record of their own. Diem, Facebook's stablecoin consortium, folded in 2022 and sold its assets to Silvergate for $182M after two and a half years of regulatory resistance, despite a regulator reportedly calling it the best-designed stablecoin project the US government had seen. Symbian, the OS alliance Nokia, Sony Ericsson, Motorola and others built to run as one shared platform, was still the most popular smartphone OS worldwide in 2010, then lost that position to Apple's iOS and Google's Android, two single-company platforms that could just move faster than a ten-member board. OUSD seems to be betting it dodges Diem's specific failure mode by staying out of the consumer-facing currency business entirely, positioning itself as infrastructure behind existing brands instead of a brand people are asked to trust directly.

What works for OUSD is that value distribution in stablecoins is lopsided toward issuers today, and that changes in one of two ways. Either existing issuers get forced to share it, or new issuers show up already built to share it.

We've already seen the first path. Circle spent years keeping all of USDC's reserve income. Then Hyperliquid built enough distribution that Circle had no real choice, USDC became Hyperliquid's "Aligned Quote Asset," and Hyperliquid now keeps up to 90% of the reserve income USDC generates there, an estimated $200M a year, funnelled into buying back HYPE.

OUSD is the second path. Same deal, offered to 140 partners on day one instead of being extracted from one issuer at a time.

Either way, the question is who actually captures the shared value once it's on the table, and that comes down to who holds these dollars. A processor that moves $10B a month but holds each dollar for eleven seconds has no float worth sharing. The yield only exists if someone holds a balance.

Riseworks, the payroll platform, is an example. It's processed $1.5B in lifetime payroll volume, more than half of that now settling in stablecoins. USDC is the dominant share of it. What matters is that workers paid through Riseworks, especially where the local currency is depreciating, don't withdraw the full balance right away. That uncollected float has been Circle and Tether's for free. Under a revenue-share model, it isn't anymore. Riseworks gets a share and can decide whether to pass anything on to the end user (of course, depending on regulations).

Plasma, a stablecoin chain that Tether and sister company Bitfinex are investors in, but don't run, holds around $890M in USDT today. At a rate close to its blended reserve yield, that's on the order of $35-45M a year in yield that doesn't flow back to the chain.

The same logic holds true for merchant banks and import-export businesses that hold working capital in USDC or USDT across settlement cycles lasting days or weeks. Anyone custodying stablecoin balances on someone else's behalf, long enough for it to matter, has been handing that yield to Tether or Circle for free.

So it’s about "who is holding stablecoins on someone else's behalf and earning nothing for it." That category, payroll platforms, remittance corridors, merchant banks, and neobanks, has been running on borrowed economics because there was never a structural reason it had to work that way.

Tether can keep making $10B a year for a while yet. That's not what we are focused on. What we want to see is the next $200M-a-year deal like Hyperliquid's become the standard term sheet, whether Tether and Circle end up writing it themselves or OUSD writes it for them.