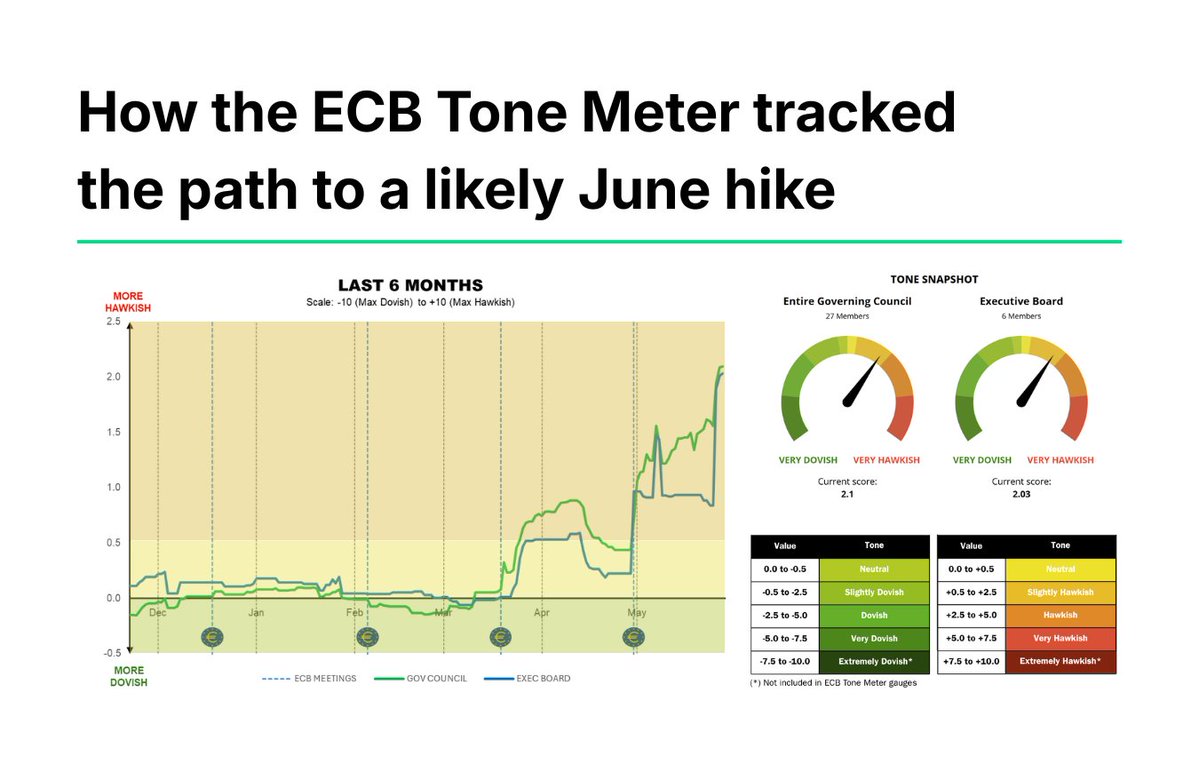

🧵 Storytime: This is how our #ECBToneMeter tracked the ECB’s gradual shift toward what now looks like a likely June rate hike.

When the Middle East war began, our tool (which measures the overall dovishness or hawkishness of recent ECB communication) was effectively neutral.

Before the conflict, ECB policymakers were in what many described as a “good place”:

▫️ Inflation near 2%

▫️ Inflation projections near 2%

▫️ Interest rates at 2%

Then the shock hit.

On February 28, in the outbreak of the war, our indices stood at:

▫️ Governing Council: -0.13 (neutral)

▫️ Executive Board: 0.00 (neutral)

⏳Just three days to go until what looks set to be the ECB’s next rate hike.

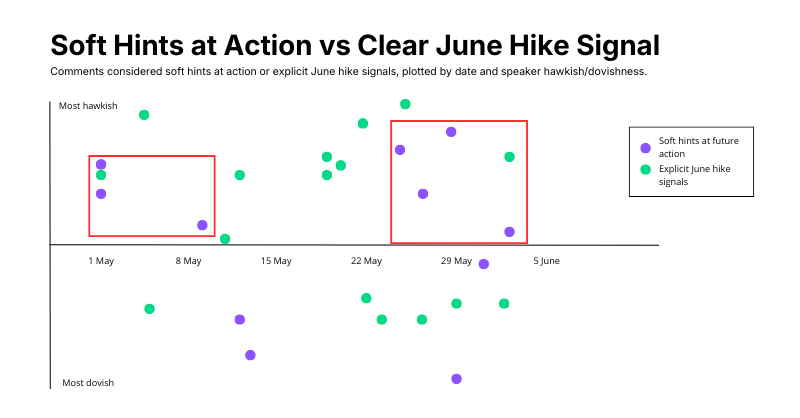

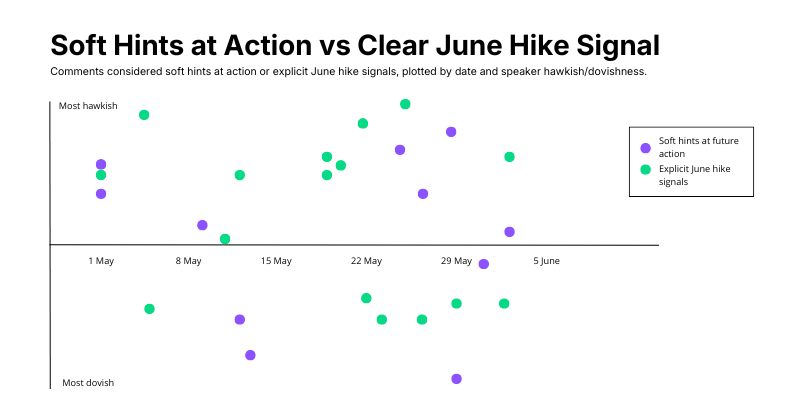

👀 Which policymakers have explicitly pointed to a June move?

🇧🇪 Wunsch: "[T]here is probably still a case for hiking [even if the US and Iran were to reach a peace deal], it's just a bit less strong." (3 June)

🇱🇹 Šimkus: "I think there is no need to surprise the markets and not make decisions. In my opinion, we have a 25bp interest rate increase in place." (2 June)

🇬🇷 Stournaras: "The most likely development is a rate hike in June." (27 May)

🇪🇺 Schnabel: "I think a rate hike in June will be needed." (26 May)

🇲🇹 Demarco: "In June we probably might need to hike." (22 May)

🇦🇹 Kocher: "[I]f we believe that 2% inflation is unattainable, then an interest rate hike is necessary." (19 May)

🇩🇪 Nagel: "There is a higher probability now that we are now away from the baseline scenario, and that means that maybe we have to do something." (19 May)

🇨🇾 Patsalides: "As things stand, things are worsening. So, things are pointing to a raise in interest rates." (11 May)

🇸🇰 Kažimír: "[P]olicy tightening is all but inevitable." (4 May)

More communication patterns ahead of the ECB’s June meeting in our #ECBCommentRecap ⬇️

3⃣ Some of the most hawkish policymakers never explicitly backed a June move, preferring more indirect signaling.

Not every hawk chose to prepare markets by openly calling for a June hike. Some like 🇮🇪 Gabriel Mahklouf instead emphasized readiness to act if needed, others like 🇪🇺 Frank Elderson suggested it was “increasingly unlikely” for the ECB to look through the energy shock, allowing markets to draw their own conclusions about the likely timing of the next move.

This insightful chart maps how ECB policymakers signaled a June rate hike:

🔹Explicit June hike signals came mainly from hawks, but support gradually broadened.

🔹Explicit signals became much more frequent in the second half of May.

🔹Some of the most hawkish policymakers never explicitly backed a June move, preferring more indirect signaling.

Let’s explain why 🧵

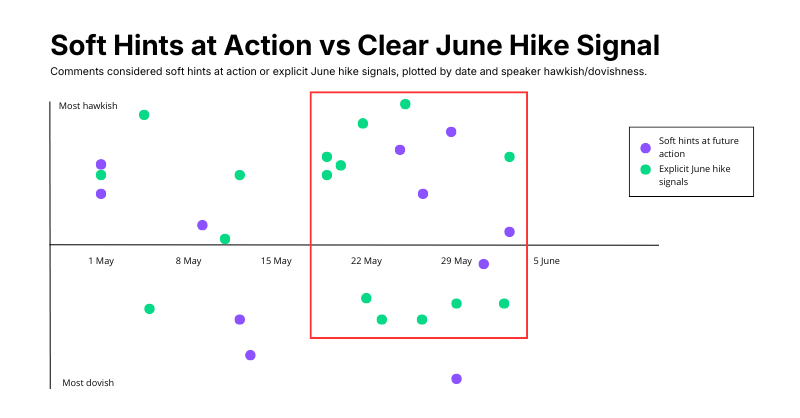

2⃣ Explicit signals became much more frequent in the second half of May.

While a few policymakers were already preparing markets for a June hike in early May, explicit references to a June move became markedly more common later in the month. This suggests the Governing Council's confidence in the case for a hike increased as fresh data and analysis became available ahead of the meeting.

Credibility is not a stockpile the ECB can simply spend by not hiking. It exists because markets and the public believe the ECB will react when its reaction function calls for it. If modest tightening is now warranted (as the entire GC seems to believe), not acting would consume the very credibility being invoked.

💡Interesting question ahead of next week’s ECB meeting: Will policymakers support a June hike partly to preserve the ECB’s credibility with markets?

These are the Governing Council members who have explicitly raised that argument:

🇧🇪 Wunsch: "At some point, we cannot let the market do all the lifting. We need to take a stance."

🇱🇹 Šimkus: "The ECB has credibility, and we will do what is needed to make sure inflation is at 2% in the medium term. That potentially requires a hike in June."

🇪🇺 Schnabel: "Markets reflect expectations about our policy, but they cannot do our job. If we judge that these expectations are appropriate, then eventually we will have to act. Otherwise there will be a disconnect between our actual reaction function and what markets believe our reaction function is."

🇬🇷 Stournaras: "For the credibility of the ECB and our reaction function, we will probably have to raise rates in June."

🇲🇹 Demarco: "In June we probably might need to hike … It’s about preserving credibility, we can’t be seen to be behind the curve."

🇫🇮 Rehn: Entering the adverse scenario could force the ECB to hike rates "for the sake of credibility."

🇱🇻 Kazāks: "Financial markets have tightened financing conditions, supporting policy transmission, but for sustained effects this needs to be reinforced by monetary policy."

🇦🇹 Kocher: "To some degree, ECB communication has contributed to the right perception of the situation. If you look at credit, you see tightening by markets, not by our decisions. But you cannot rely on that forever. If the shock is large enough and more persistent, ultimately the ECB has to take action."

🇪🇪 Müller: "[T]he tightening of financing conditions, which is necessary to counter price pressures, has taken place without direct intervention by the central bank. However, this so-called advance effect loses its power if central bank interest rates remain unchanged for a longer period of time."

More interesting patterns in ECB communication coming up in our #ECBCommentRecap in a few days.

@forexflowlive One could argue the ECB hasn’t hiked until now precisely because of the damage coming to an already weak economy. But even the Governing Council members quickest to worry about growth have now accepted the case for modest tightening.

💡 Why Pierre Wunsch would be better suited to opposition than to succeed Christine Lagarde

One news outlet recently floated his name as a possible candidate for the ECB presidency, and his frequent media presence lately smacks of positioning. But we believe his chances remain limited for many reasons:

🔹He does not solve an obvious European appointments puzzle and does nothing for gender balance

🔹Belgium, not a natural ECB presidency country, already had recent access to top European posts

🔹His Francophone profile complicates the post-Lagarde balance

🔹Paris, which he has criticized, is likely to distrust his fiscal/spread instincts

🔹Klaas Knot 🇳🇱 is the cleaner German fallback if Germany can’t have the presidency

🔹He is no consensus-builder in the Lagarde mold; more associated with dissent and model criticism

🔹His communication style is sharp rather than reassuring

We explain this in detail in our latest #ECBInsight

https://t.co/e3g4W2c5WG

‼️ Finland's Olli Rehn just said out loud what some at the ECB had only hinted at before: the ECB is preparing an insurance hike in June.

Several colleagues had already laid the groundwork, arguing that a hike could be needed to safeguard credibility and deliver the tightening markets had been expecting for some time.

Rehn said: "Against this backdrop, while inflation risks have increased, a rate increase in June would be an insurance one, but not due to entrenched inflationary pressures."

‼️ Finland's Olli Rehn just said out loud what some at the ECB had only hinted at before: the ECB is preparing an insurance hike in June.

Several colleagues had already laid the groundwork, arguing that a hike could be needed to safeguard credibility and deliver the tightening markets had been expecting for some time.

Rehn said: "Against this backdrop, while inflation risks have increased, a rate increase in June would be an insurance one, but not due to entrenched inflationary pressures."

By then, however, the backdrop had changed dramatically.

The Iran war had pushed inflation risks higher and raised stagflation concerns inside the ECB.

Vujčić’s later remarks reflected that shift in context:

🔹 April was described as a “live” meeting

🔹 energy inflation and pass-through risks became a key concern

🔹 but he also said rates could move in either direction depending on how growth and inflation evolved

However, as shown in our ECB Tone Meter, Vujčić kept his remarks conditional and cautious, making his tone less hawkish than the entire Governing Council’s.

🇪🇺 Today marks the end of Luis de Guindos’ term as ECB Vice President and the beginning of Boris Vujčić’s mandate as the ECB’s new nº2.

How did Vujčić’s tone compare...

🔹before his name emerged as a potential candidate for the vice presidency,

🔹during the race to succeed de Guindos

🔹and after his formal appointment?

We break it down in this #thread 👇🧵

In that context, Vujčić argued the ECB should react only to persistent inflation pressures — “either up or down” — rather than temporary deviations.

He also said that he did not “have a special scenario in mind for a rate cut or a rate hike” and described growth risks as broadly balanced.

He then went silent for almost three months, only reappearing when announced as the Eurogroup’s preferred candidate for ECB Vice President.

https://t.co/91E3IH6OMd