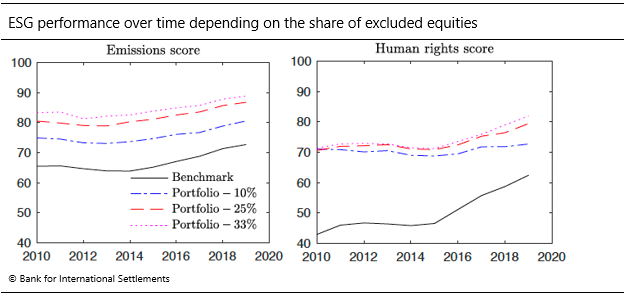

Deconstructing ESG scores into their granular components helps to devise more targeted equity investment strategies with better ESG and risk-return characteristics #ESG#SustainableInvesting https://t.co/Vfh9JF9mGr

The dots probably served a purpose post-GFC, in hammering home the seriousness with which the Fed meant what it said about staying at ZIRP for a long time.

But in framework where destination is supposed to trump path, they inevitably draw FOMC members back into a path discussion

@modestproposal1 At the 90% percentile (expenditure-weighted) inflation is 6.5% yoy - at the 75th percentile 3.8%. Median inflation is 1.8%. https://t.co/RtQuo5TBCt

Now that the #GreenSwanConference is over, what next? Luiz Pereira summarises the main takeaways of the discussions and passes the baton to Ignazio Visco from @bancaditalia@g20org ahead of #COP26@COP26 https://t.co/Yb5x1T1cp6

Carstens: Policymakers need to enable investors by enhancing market transparency and deterring greenwashing. If we want to avoid a green bubble, we need to act now #GreenSwanConference https://t.co/6Cka9ZTOJx

Carstens: We are seeing Green Swan events with greater frequency, therefore addressing these risks as soon as possible and in a coordinated fashion is the best course to preserve #FinancialStability#GreenSwanConference https://t.co/6Cka9ZTOJx

Carstens: the BIS’s Financial Stability Institute will deliver a dedicated portal, for training on climate risks in partnership with #COP26, and launch a Climate Training Alliance with the @NGFS_, IAIS and @SIFForum

https://t.co/6Cka9ZTOJx

Agustín Carstens: central banks recognise taking action against #ClimateChange is paramount, and this requires a significant amount of coordination across and within jurisdictions & sectors #GreenSwanConference https://t.co/6Cka9ZTOJx

Banks appear to price only the direct #CarbonEmissions of firms & not their broader carbon footprint. Further, the price of risk appears small relative to potential financial risks – such as the introduction of #CarbonTaxes#LoanPricing#ClimatePolicy https://t.co/CFWuKbBEPN

We find that the price of carbon risk was low considering the potential financial hit due to, say, a realistic level of #carbonprice. It also appeared to be based on a narrow scope of borrowers' emissions (scope 1). #climaterisk#sustainablefinance#carbonintensity

Check out my new working paper with my co-authors Frank Packer and Kathrin de Greiff on the pricing of #carbonrisk. Banks do charge a premium to borrowers with higher carbon emissions since the Paris Agreement - independent of the industry sector. But....https://t.co/mEx3fxitSV

Cities will play a key role in mitigating climate change. In this panel on greener cities at the #GreenSwanConference we will discuss ways to finance them. I am more than honoured to be part of this panel with fantastic experts. #climatefinance#cities#greenfinance#greenbonds

Everyone dreams of “greener cities”, but what are the challenges to achieving #SustainableCities and how can finance make this dream come true? This is just one of the many issues being discussed at the #GreenSwanConference next week https://t.co/RV3059Pogw

@PeterBofinger Bei Negativzinsen macht es wenig Sinn sich über den Verkauf von Staatsbeteiligungen zu finanzieren. Der Schuldenstand wird auch nur in der Statistik gesenkt. Die Nettoschulden bleiben gleich wenn man etwas verkauft. Und die Schuldenlast sinkt auch nicht bei Negativzinsen.