June 2026 portfolio update

Increased my dollar cash position to almost 20%, mostly due to currency arbitrage and also to preper for increasing my position size in $SPGI $ISRG $MA $MSFT

Bought more $ISRG $MA and exited $NTDOY completely on the path to 14-15 holdings by year end.

End of June 2026 portfolio update.

My portfolio contains exceptional, world-class businesses. I avoid speculation, and instead focus on dominant companies with massive moats, high returns on capital, and long runways for growth.

This past month, I continued to add to Meta, Mastercard, S&P Global, and Brookfield. I've been searching for other dislocated opportunities, and may strike if I see something compelling.

I continue to remain very bullish on the portfolio.

If you haven't already, please subscribe to my Substack for deep dive equity research into my holdings (as well as other compounding machines), and highly relevant thematic trends shaping today's markets. Link here and in bio: https://t.co/u5CjOu8mrE

$GOOG

$META

$NVDA

$AMZN

$V

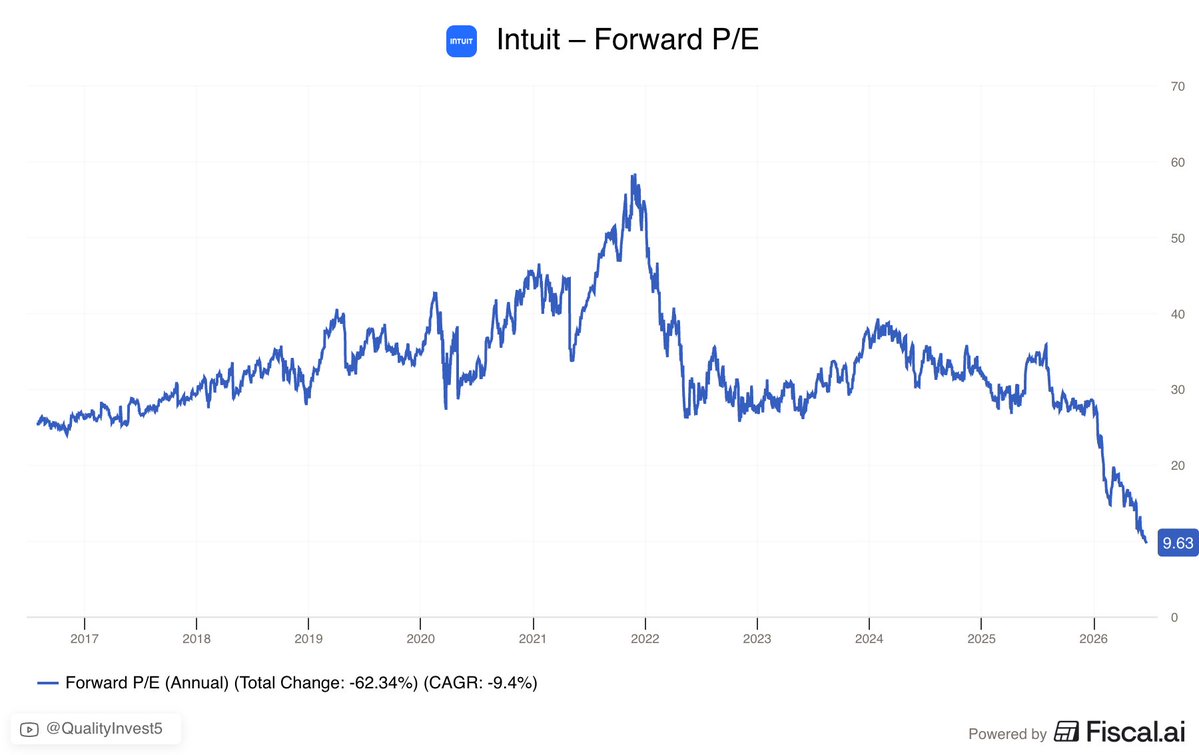

$SPGI

$UBER

$MA

$MSFT

$FICO

$ASML

$KLAC

$BN

Growth wasn't even all that bad on this segment (roughly 8% YoY)

The likely culprit for the spinoff is the margins being HALF of the rest of the business combined

This spinoff (although detracting from revenues) is margin accretive and thus a good move in my books.

$SPGI

$CPRT

Jay Adair was the successor of Willis Johnson, Copart's founder and first CEO. Johnson raised him professionally, and even became is father in-law. Although the return of a former CEO is usually a bad sign, Adair could bring back founder led, skin in the game thinking.

Jeff Liaw getting replaced with Jay Adair at $CPRT give me mixed feelings.

1) You usually don't replace the CEO with a former CEO unless there's a turnaround or something structurally negative is happening.

My guess is IAA is providing a better product and the gap is increasing.

2) Jay Adair has major skin in the game that Jeff Liaw didn't.

This is good thing, the majority of his wealth is in Copart and he's married to the founders daughter.

What will be interesting to see now is the capital allocation.

- Do they spend more to improve their services?

- Do they look to increase the buybacks?

- Do they look to acquire more land?

My gut tell me they are going to spend more to improve their services & competitive position but time will tel..

Quality compounders usually trades for perfection. True opportunities arise on those rare moments, which can come once in a decade or more, when the company faces big, but solvable problem. $CPRT could be in that special moment right now.

One of the problems with a business that has slowed growth is that you can never be 100% sure what caused it.

In $CPRT's case they noted that there was more drivers going without insurance and their customer's were losing marketshare in a temporarily pricing battle.

With Jeff Liaw stepping out of Copart and Jay Adair returning as CEO, it draws the accuracy of these claims into question.

Prior CEOs *usually* don't come back unless they feel like there is something that needs fixing.

So were the slower growth rates the result of what Jeff Liaw claimed or was it something else?

In the past few years competitor IAA/ $RBA has gained market share against Copart along signs that they improved their service.

The fear is that it is the service gap differential closing has driven carrier volume losses to IAA, not the factors previously mentioned.

It honestly reminds me a bit of Shantanu Narayen stepping down from $ADBE at a time their growth was slowing down, but they said it was temporary and self-inflected (primarily from freemium products delaying the monetization funnel).

It raised the question that if they believed their own explainations as to why the business wasn't growing more, why did they replace the CEO?

Jay Adair was involved in Copart since it's founded and was CEO from 2010 to 2024.

I view him becoming CEO again as a postive development because of his skills... but the fact that they needed him to come back is a negative.

Jeff Liaw CEO of $CPRT is stepping down and being replaced by Jay Adair

Jay was the prior the CEO and Jeff was the 3rd CEO in the company’s entire history.

(The first was the founder and Jay was there since the beginning too)

Honestly hard to interpret this, but unless it’s health related, it seems to give credence to the concern that the market share losses to Progressive weren’t entirely driven by insurer market dynamics

@JustTEEit@VividProwess only people who don't know shit about this conflict can say that. You think you know something about the middle east by watching your media, and you are a great war lord because you saw some war movies. The truth is they never hide their intentions, you just never tried to listen

Ackman views $MSFT as having an "impossible to disrupt" position in enterprise software. The base Microsoft 365 package has 450M users at a very low cost per seat, roughly $200 per customer. It would be nearly impossible for an enterprise to replace these various components with 3P vendors, even at twice the price.

Microsoft Copilot gives enterprise employees a secure way to access AI tools without putting the company at risk of extreme cloud computing bills or exposing proprietary data.

$SPGI is back under $400...

22x FCF for one of the strongest moats of all time growing earnings double digits and distributing all FCF back to shareholders.

Sounds like a deal to me.

Both $GOOGL and $MSFT were great contributors to my performance in the past 6 years. I bought the dips, went all in on $GOOGL on April 25 ,but sold $MSFT on August 25 when valuations got streched. Luckily, got a chance lately to re-enter $MSFT, and here i'm going all in again.

$CPRT Is genuinely one of my favorite companies which I own, but the market doesn't agree with me on that, and I'm down -30% on my position. This is the kind of positions you want the add on the way up, not down. I'll wait for next 1-2 quarters to decide about increasing my stake

$CPRT is down over 50% & I opened a position this week

Heres why:

1) Duopoly: Copart & IAA own 80% market combined

2) Asset Light Toll Booth: 37% operating margins

3) Owns most of its land. IAA doesn't.

4) Buybacks: $0 at the highs, $1.4B last quarter

5) Fortress balance sheet: zero debt, $4.2B net cash

6) Short term tech in cars is a tailwind since its cheaper to write off than to repair

7) Paying 18x earnings (ex-cash)

8) Downside's protected:

You could give a someone 50B and they can't get new salvage yards zoned near cities Copart's footprint is effectively impossible to replicate

The 3 risks I'm watching but are not thesis breakers:

1) Does IAA wins market share

2) If uninsured a structural change

3) If AV moves quicker than expected this decade

What am I missing?

Month 12: "Buffett & Munger Unscripted" by A.Morris.

No better way to end the year than listening to the masters on Berkshire annual meatings. This collection captures their raw, unscripted wisdom on capital allocation, avoiding stupidity, and finding quality businesses. 🎙️

Become a quality investor in one year. I’ve put together a reading list of 12 must-read investing books, one for each month. From economic moats to intrinsic value, these will transform how you think about businesses and how to analyze them🧵👇

#investingbooks#qualityinvesting

Month 11: "Where the Money Is" by Adam Seessel.

Value investing meets the digital age. Seessel updates classic valuation metrics for modern tech companies, explaining how to analyze the moats and intrinsic value of software and internet giants. A modern classic. 💻