#Turkey credit under pressure amid oil-driven inflation and FX intervention, but widening spreads improving relative value

🇹🇷 → BUY: bonds -3.2%, reserves declining, but spreads ~100–130bps wide vs peers

At ~6.7% yield, risk/reward turning attractive despite macro headwinds

MENA credit mixed amid geopolitical risks. External vulnerabilities rising but dispersion in relative value is increasing

🇪🇬 🇯🇴 HOLD: resilient but near-term risks elevated

🇹🇷 BUY: spreads widened, RV more attractive

🇱🇧 HOLD: recovery story intact but risks persist

🇿🇲 🇺🇦 → SELL

Caribbean credit looks fully priced after the 2023–25 rally. Fiscal consolidation gains are largely reflected, leaving limited spread compression at current tight levels.🇧🇧 🇧🇸 HOLD solid fundamentals but balanced risk/reward 🇯🇲 SELL: low carry, structural constraints

🇹🇹 HOLD

#Turkey reserves remain elevated ($207bn) but gold-heavy composition tempers liquidity. Strong market access after €2bn deal at tightest spread in 15y; compelling relative value — we keep BUY.

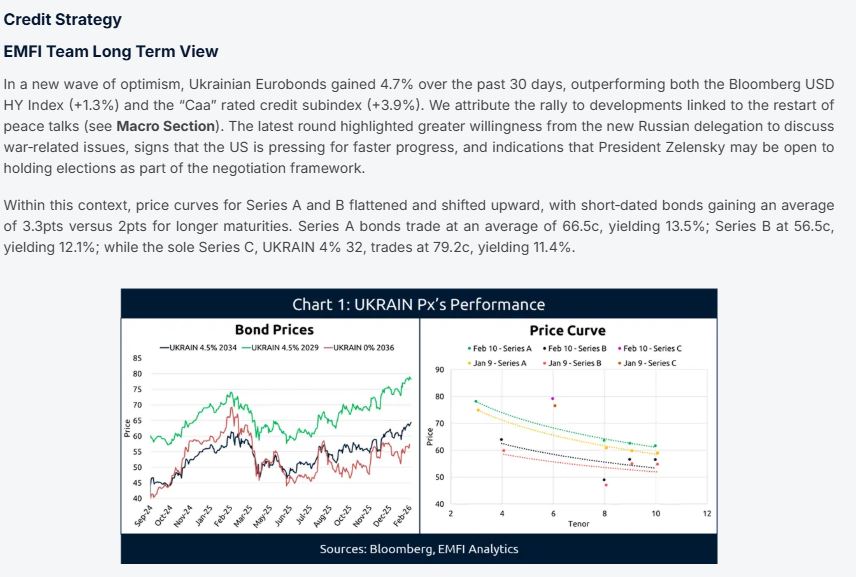

#Ukraine Eurobonds rallied ~4.7% MoM on renewed peace-talk optimism, with curves shifting higher and ratings stabilizing. Despite momentum, we see the conflict likely extending into 2026.

#Angola Eurobonds returned 1.9% MoM, outperforming peers as the curve tightened ~33bps. Solid refinancing plans and attractive carry keep Angola ~180bps wide to peers — we maintain BUY.

#Honduras Eurobonds outperformed MoM, HONDUR34 ~115c as political risk eased and IMF anchor holds. Coalition strength supports 2027 refinancing, but rich valuations keep us at HOLD

#Argentine Eurobonds delivered a solid +17.4% YTD in 2025, outperforming EM HY & LatAm peers despite election volatility. The curve has re-normalized: front end 8.3%, belly 9.7%, long end 9.7%. ARGENT ’35 trades 74.4c, +18.7% TR YTD.

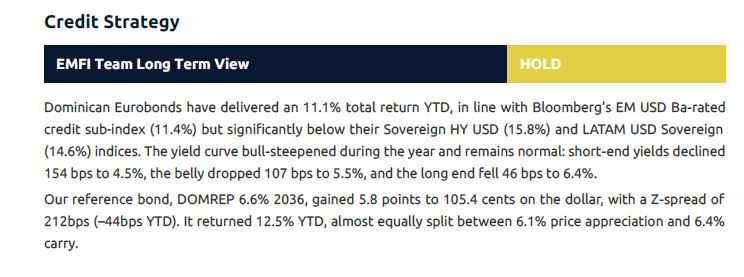

#DominicanRepublic

2026 Eurobond service is light at USD 1.9bn—~9% of revenues, 7% of exports, 14% of reserves. But broader external debt service rises sharply, with ratios of 43%/31%/66% of revs/exports/reserves (~30% higher vs 25), comparing unfavorably to peers.

#Venezuelan bonds rallied +16pts (+113%) in 25' to 27–34c; PDV gained +15pts (+139%) to 25–28c Prices now mirror the 2017/2019 optimism peaks. But at these levels, the trade turns binary. A true restructuring requires US sanctions relief + recognition of the governing authority

#Lebanon 2026 Lebanon faces another difficult year, with a fragile ceasefire and ongoing risk of renewed conflict undermining the prospects for meaningful economic and political reforms.

#costarica 2026, HOLD: The sovereign’s fundamentals remain strong, but current valuations already price in much of that strength, with bonds now trading at BB+-like levels.

#suriname 2026 Suriname completed a successful liability-management deal, issuing USD 1.5b to retire USD 420m and pre-fund USD 1.1bn in future payments. BUY: Despite trading rich to rating peers, we still see attractive carry supported by expectations of strong oil-driven growth

#jordan continues to show gradual fiscal progress and macro stability, but remains vulnerable to regional shocks and softer trade conditions.

With valuations tight and limited room for further spread compression, we stay HOLD, favoring the short-end (’27–’28s).

#Nigeria 2026 BUY: With room to compress vs peers and solid credit ratios, Nigeria’s curve still offers compelling value — combining high expected returns with attractive current yield across the curve

#Pakistan 2026 Outlook: Growth edges up to 3.2% but inflation rises to 12.2%. Military & IMF influence over policy strengthens amid high India/Afghanistan geopolitical risk. Tight valuations + limited upside → downgrade to SELL.

#Colombia 2026 Outlook: Elections loom with multiple congressional & presidential scenarios. A Cepeda win would raise fiscal/institutional concerns. . Current account gap widens to 4.1%. BUY: Attractive pricing outweighs fiscal risks.