I'm not an analyst, but I work with some heavy hitters across the AI & crypto space...

And I need to talk about what they've just pulled off.

(Save this.)

Over the past few months, our PRO team has been on fire - with 5 calls sitting over +100% returns, and another 10 pushing gains of +20-90%.

I need to be somewhat neutral here and cover trades from both our AI and crypto analysts, otherwise they'll beat me with a stick - and I can't go through that.

(Not again.)

So let's look at two trades from each sector - starting with Nebius $NBIS.

This is the AI cloud company that almost nobody had heard of a few months ago...

But earlier in the year - while everyone was watching Amazon and Google - our PRO team spotted Nebius landing billions in deals with Microsoft, Meta, and Nvidia (who even took a stake in the company)...

They bought in → sent out a trade alert → the stock moved 177%.

Micron $MU, on the other hand, was almost the opposite kind of bet - boring, even.

Every AI system on earth runs on memory chips, and Micron is the last big maker still standing in the US.

While demand for its chips went vertical, the market kept pricing it like a sleepy commodity stock.

... until it didn't.

That one moved 168%.

Moving over to crypto, we have Hyperliquid $HYPE...

They recently flipped a switch that turned the billions of dollars sitting on its platform into real revenue for the people holding the token.

Our PRO team was in well before that became the thing everyone was posting about.

(That position moved 120%.)

And finally: Galaxy $GLXY - maybe my favorite of the four, because it's two trends in one ticker.

It holds a big stack of crypto on its books and runs trading and lending desks for major institutions.

On top of that, it's turning an old bitcoin mining site into an AI data center, with a billion dollars a year in rent already signed.

It's the slow burn of the group so far, but it still managed to move 34% while the majority of crypto assets have bled.

And those are just the four I chose to talk about.

The same team also called:

- SK Square +146%

- Infineon $IFNNY +113%

- Bloom Energy $BE +108%

- Credo $CRDO +93%

- Applied Optoelectronics $AAOI +83%

If you've never heard of half those names, that's kind of the point.

This is what the Milk Road PRO team does.

They're paid to stare at AI and crypto all day, find the names before the crowd does, and back them with their own money.

Unfortunately, by the time most of these assets show up in your feed, the chart has likely already run (and the easy part is over)...

Good news is:

You don't need to know our analysts personally, or pay thousands of dollars to look over their shoulder.

You can see every position they're holding right now, and the exact thinking behind each one, for a single dollar.

The link to start a 7-day $1 trial is in the first comment below. 👇

Most investors think memory stocks have peaked but they are completely wrong. (Save this).

Bernstein just dropped a research note that blew up in the memory world, and the number is staggering.

They now expect HBM4 pricing to rise from $16.6 per GB today to $37 per GB in 2027 more than a 2x increase driven entirely by what happens when Vera Rubin starts shipping in volume.

Here is why that matters.

A single Vera Rubin NVL72 rack, the unit that hyperscalers like Microsoft, Google and Amazon are ordering by the thousands carries 20.7 terabytes of HBM4 memory and 54 terabytes of LPDDR5X memory.

At today's prices, the memory bill for a single rack already exceeds $2 million and at Bernstein's 2027 price forecast, that same memory bill nearly doubles.

This is a direct transfer of wealth from the hyperscalers who buy the racks, to the three companies that make the memory inside them.

Jensen Huang himself just confirmed in Seoul that all three HBM vendors, SK Hynix, Samsung, and Micron have been qualified and are in full production, all racing to support Vera Rubin.

That is the first time all three have been simultaneously qualified for an Nvidia platform.

But the market share split matters enormously.

SK Hynix currently commands roughly 60% of HBM4 supply for Vera Rubin, Samsung around 30%, and Micron around 10%.

Micron has already sold out its entire 2026 HBM4 allocation under long term contracts and SK Hynix raised its HBM4 prices 70% in recent contract negotiations, and Nvidia will pass those costs directly to hyperscaler customers.

Memory now makes up 26% of the total Vera Rubin rack cost up from just 9% on the previous Grace Blackwell generation.

That is a 435% increase in the memory cost per rack in a single product cycle.

Milk road remains bullish on Micron and the memory trade, come join Milk Road Pro for our full breakdown of what the HBM4 repricing cycle and our entire AI thesis.

Link below!

The man who turned $225 million into $13.7 billion just took a 5.6% stake in Nebius (Save this).

Aschenbrenner is a 24 year old former OpenAI researcher who was fired in 2024, then published a 165-page essay called situational Awareness, the Decade Ahead laying out a decade-long AI thesis with more precision and depth than almost anyone in markets had attempted.

Then he built a fund that expressed that thesis directly, he started with roughly $225 million in disclosed equity holdings in late 2024.

By early 2026, the fund had grown to $13.7 billion in disclosed US equity exposure, a performance that, over a single year, outpaced Warren Buffett's long term compounded returns across decades.

His thesis is not complicated, but it is precise and he laid out a simple extrapolation, the largest AI training clusters have been growing at half an order of magnitude per year for a decade.

GPT-4 ran on a cluster of roughly 25,000 A100s, about $500 million worth of compute, drawing 10 megawatts of power.

Play that forward two years to 2024, a 100-megawatt cluster, 100,000 H100 equivalents, costing billions.

Forward two more years to right now, 2026: a gigawatt-scale cluster, a million H100 equivalents, costing tens of billions.

By 2028, 10 gigawatts, more power than most US states, hundreds of billions of dollars.

And by 2030, a trillion dollar cluster drawing 100 gigawatts over 20% of all US electricity production.

His conclusion is that the real bottleneck in the AI era is not algorithms but rather compute, power, and the infrastructure to run them at that scale.

Nebius is exactly that bet and the company reported Q1 2026 revenues of $399 million, up 684% year over year.

Cost of revenues as a percentage of total revenue improved from 49% to just 26%, showing that every dollar of additional revenue is flowing through at increasingly high margins as capacity reaches full utilization.

The company is guiding to $7 billion to $9 billion in annualized run-rate revenue for the full year 2026 up from $1.2 billion just 18 months ago.

The pipeline heading into 2026 is tracking toward $4 billion supported by contract durations that extended 50% in a single quarter as large enterprise customers commit to longer-term capacity agreements.

Nebius has signed a five-year, $17.4 billion AI infrastructure deal with Microsoft and the company has secured over 2 gigawatts of contracted power and is building nine new data centers including a 1.2 gigawatt AI factory in Pennsylvania.

Capacity is sold out and Aschenbrenner just filed to disclose a 5.6% stake, 12.4 million shares as a significant shareholder of record.

The man who built the most precise AI infrastructure thesis in public markets, who turned $225 million into $13.7 billion by betting on the physical backbone of AGI, looked at Nebius and bought enough shares to trigger a 13D filing.

Nebius is a core Milk Road position and our subscribers are up massively.

Come join Milk Road Pro and get the next call before everyone else figures it out. Link below/in bio.

$NBIS just broke above $200 for the first time in history.

And they just raised 2026 CapEx guidance to $20B-$25B. Up from the prior $16B-$20B range. They are not slowing down.

Their AI cloud revenue growth is up 841% YoY.

But most people still don't know the story behind it. Here it is:

Yandex was not just Russia's Google. Before the war it was also their Uber, their Instacart, their DoorDash, their Spotify. 25,000 employees. $30 billion valuation in November 2021. Founded in 1997, a year before Google.

Then the war started.

Over a thousand engineers left Russia. The top management fragmented. And Arkady Volozh, the founder, had to make a decision.

They cut everything. Sold the Russian assets. Started from scratch with a Dutch holding company and roughly 1,000 engineers who had spent years building one of the most advanced AI infrastructures in the world, including hundreds of megawatts of data centers and tens of thousands of GPUs. Yandex was one of Nvidia's largest customers before the AI boom even started.

They didn't know what they were going to build next. They just left.

Then at the end of 2022, ChatGPT happened. And they realized they were sitting on exactly the right team, the right infrastructure, and the right moment.

The NASDAQ listing story is wild on its own. Trading had been suspended for 2.5 years. Then on a Friday last October, NASDAQ called and said: congratulations, you're compliant again. You start trading Monday.

One day to prepare a press release. That's all they had.

Several weeks later they closed a $700 million PIPE with Nvidia, Accel, and dozens of venture and hedge funds. Over $2 billion in cash on the balance sheet. Zero debt. Rare for any company in this sector.

We called $NBIS early when it was trading at $108. Our call is now almost 100% up.

And $NBIS isn't the only. Our analysts were early to $AMD, early to $MU, early to $BE.

Don’t miss the next call, come join us for just a $1.

The link to join is below! (or in bio)

Jensen Huang has been publicly endorsing Nebius for months and today, Nebius proved he was right (Save this).

This morning Nebius reported Q1 2026 earnings and they were a full blown statement.

Revenue came in at $399 million, up 684% year over year, against a consensus estimate of $388 million.

Adjusted EPS came in at $2.11 against Wall Street's estimate of negative $0.78.

Adjusted EBITDA margin in the AI cloud business nearly doubled quarter on quarter to 45%.

Contracted capacity now exceeds 3.5 GW, surpassing their 3 GW target and they've raised guidance to more than 4 GW by year-end 2026.

Full year revenue guidance is $3.0–3.4 billion and full-year ARR guidance has been reaffirmed at $7–9 billion.

$6.3 billion in capital has been secured including convertible notes and a direct equity investment from Nvidia itself.

The growth acceleration is the part nobody expected.

Q4 2025 revenue grew 547% year over year while Q1 2026 grew 684% and that rate is accelerating.

Nebius went from $50.9 million in revenue one year ago to $399 million today.

Wall Street analysts currently project revenue growing from $530 million at year end 2025 to $9.7 billion by the end of 2027, nearly a 20x increase in two years.

The company is also executing aggressively on physical infrastructure.

Yesterday, Nebius announced it has secured 1.2 GW of power and land for a new owned AI factory in Pennsylvania bringing its total number of sites exceeding 100 MW to seven.

It also recently announced a 310 MW AI factory in Lappeenranta, Finland projected to be one of Europe's largest dedicated AI facilities and has supply agreements totaling over $40 billion with Microsoft and Meta.

The company plans to go from 7 operational data centers in 2025 to 16 by end of 2026 and this is what Jensen saw when he said "Nebius will take care of you."

The Milk Road Pro analysts have had Nebius on our radar since the early days, and it’s been one of the clearest pure play AI infrastructure stories in the public markets.

Today’s earnings just validated everything, and our position is now up massively since we first added it.

This is exactly why you should come join Milk Road Pro. Link below!

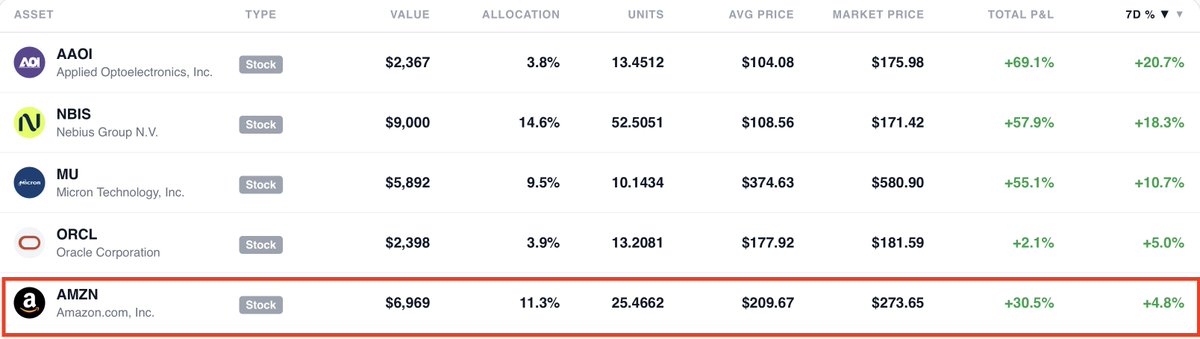

Amazon is still the most underrated stock in the Mag 7 and if you're sleeping on it, you're about to miss the next AWS moment (Save this).

Every few years, Amazon does something it has only done a handful of times in its history, it takes a capability it built for itself and opens it up to the world.

The first time it did this, it created AWS, a business now running at a $142 billion annual revenue rate, growing at 24% year over year, printing 35% operating margins, and projected by CEO Andy Jassy to hit $600 billion in annual revenue by 2036.

What started as Amazon's internal cloud became the backbone of the internet and today, it's doing it again, this time with logistics.

Amazon just launched Amazon Supply Chain Services opening its full freight, distribution, fulfillment, and parcel shipping network to any business on the planet.

And the early signups are P&G, 3M, Lands' End, and American Eagle Outfitters.

These are some of the most operationally sophisticated companies in the world, and they're handing Amazon the keys to their supply chains.

The proof of concept was already there.

Since 2006, independent sellers shipped more than 80 billion units through Fulfillment by Amazon and sellers using Amazon's end to end logistics see nearly 20% higher sales.

Amazon took that model, battle tested it across hundreds of thousands of businesses, and now it's offering it to the entire $1 trillion global 3PL market, a market projected to hit $2.1 trillion by 2032.

Now here's why the stock is still underrated, Amazon is trading at a

P/E of 32.7x on a market cap of $2.9T.

That multiple barely prices in what's already in the building, AWS re accelerating, advertising crossing $50 billion plus and gross margins expanding to 50% in 2025 and this doesn't price in ASCS at all.

This is a company that just opened a new enterprise logistics revenue line targeting a trillion dollar market, and the market is treating it like nothing happened.

The financials back the bull case hard, FY2025 revenue hit $716.9B , up

12.4% year over year. Q1 2026 came in at $181.5B in revenue with EPS of

$2.78, 74% above the consensus estimate.

Milk Road now see $810B in revenue for FY2026 and the earnings machine is not slowing down.

The capex spend $200B in 2026, looks scary on paper but it's the same bet Bezos made with AWS in the early 2000s. Build infrastructure nobody else can afford to replicate, then monetize it for decades.

Every dollar Amazon is spending on robotics, AI forecasting, and logistics density is making the same network it just opened up to enterprises cheaper and faster to operate.

That's operating leverage compounding in real time and this is exactly why Milk Road analysts remain bullish on Amazon.

AWS is accelerating into the AI supercycle and sitting on $244 billion in contracted backlog, ASCS is a multi year enterprise revenue unlock that is just getting started.

We've already started building a significant position and is up on it massively.

If you want to see exactly how we're sizing it, what we're buying, and our full thesis, come join us.

Link in below!

Leopold Aschenbrenner, the 24 year old who wrote a 165 page AGI manifesto, got it right on the money, and turned it into a $5.5 billion hedge fund.

And he's identifying the single most important milestone to watch for in all of AI.

The question is can AI automate AI research itself?

Here's why that question matters so much.

Right now, a few thousand human researchers at the frontier labs are driving all the progress.

They design experiments, write papers, propose architectural improvements, build the next generation of models and it's an incredibly small workforce doing incredibly high-leverage work.

If an AI system can do that job even partially, the feedback loop changes completely.

The AI makes algorithmic improvements, which produces more powerful AI, which makes better improvements, faster.

You go from linear progress to compounding returns and a decade of research could compress into a year.

Aschenbrenner says there's a "pretty reasonable chance" this happens within five years.

He's not alone, Anthropic says they're on track to fully automate AI R&D as soon as early 2027.

OpenAI has publicly targeted a fully autonomous AI researcher by March 2028 and Sam Altman has said a research intern level AI will exist before the end of this year.

If he's right, the next few years won't look like the last few years but they'll look like nothing we've seen before.

The future is bright!

Not trying to bring someone else's work down, the winners' video is excellent, but so are a dozen others I came across, and they're fully original, in line with the judging criteria Tars cited themselves. You really won't dish out the possibility of them rigging the rewards their own way?

Otherwise I am not trying to undermine anyones work, simply pointing out inconsistencies, and thanks for appreciating my work

@chainstellar@tarsprotocol@SuperteamEarn not hating, simply pointing out the distinct possibility of Tars giving the $3k + $10k grand prize to themselves.

Also, to quote Tars themselves on the judging criteria:

"Creativity: Originality and uniqueness of the content"

Ground-breaking Uptime Monitoring in Solana,

thanks to @UpRockCom

This video covers why & how Uprock changes the game.

& the 🧵below breaks down its next-level approach