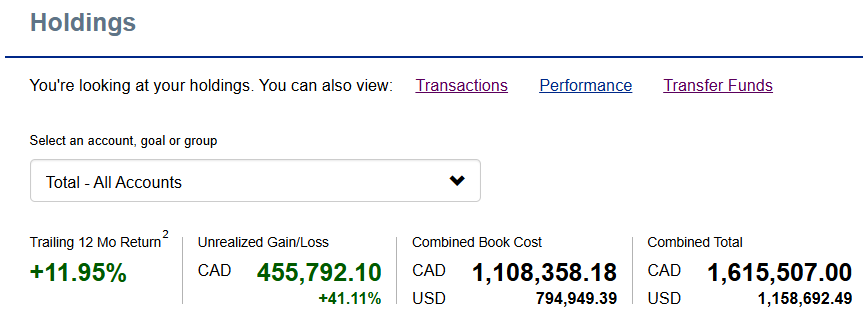

Q3 update - primary brokerage accounts were roughly flat at $1.6M over the past 3 months despite quick pullbacks in $csu.to and $tvk.to. Onwards and upwards.

A reminder from The Psychology of Money by Morgan Housel:

“The highest form of wealth is the ability to wake up every morning and say, ‘I can do whatever I want today.’ People want to become wealthier to make them happier. Happiness is a complicated subject because everyone’s different. But if there’s a common denominator in happiness—a universal fuel of joy—it’s that people want to control their lives. The ability to do what you want, when you want, with who you want, for as long as you want, is priceless. It is the highest dividend money pays.

Use money to gain control over your time, because not having control of your time is such a powerful and universal drag on happiness. The ability to do what you want, when you want, with who you want, for as long as you want to, pays the highest dividend that exists in finance.”

Did you just spend 15 mins of your time on Financial X, randomly reading people's opinions and anecdotes?

You just wasted 14.5 mins.

Better off focusing on reading (and re-reading) great books and financial papers.

"The vision of a bloodless, imminent, and seamless energy transition from fossil fuels to renewables and alternative energies has been laid bare as fallacious. Only the most ardent of idealogues still pedal this vision. In reality, we are entering into a period of energy diversification, not transition. We use more wood, coal, oil, and gas today to generate energy than at any point in history. The only fuel that we have truly transitioned away from over time is whale oil.

We have come to accept what we always knew from basic economics – “There are no solutions, only tradeoffs.” – There is no free lunch." /2

Today, while cleaning the house, I found an old notebook where I’d written down 10 things that took me a very long time to learn, and I thought, why not just quickly write a post about it in case someone else could benefit from it.

https://t.co/iuUdDvqgko

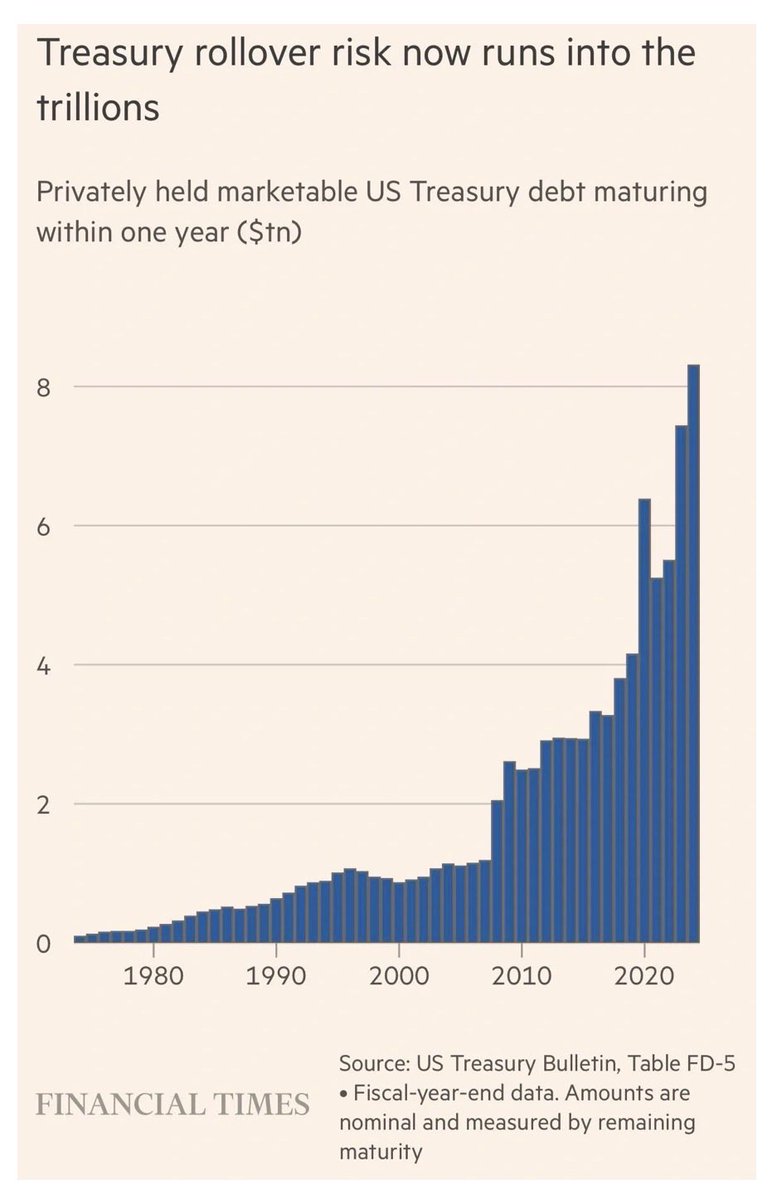

US FY2025 (ends Sept):

Revenue = $5.23T

Spending = $7.01T

Deficit = $1.78T

Interest expense already = $970B

National debt now ~$39T and climbing ~$1T every 6 months. Heading over $40T shortly.

33% of the debt (~$13T) matures & must be refinanced in the next 12 months.

With 10yr at 4.59% and 30yr at 5.13%, we’re looking at average interest on $40T+ debt heading toward 5%.

That = $2 TRILLION in annual interest.

Interest would become the #1 expense in the entire federal budget — bigger than:

- Social Security ($1.2T)

- Medicare + Medicaid ($1.2T)

- Defense ($900B)

Trump wants Defense up to $1.5T (+$600B).

Add that to rising interest and the deficit explodes from ~$1.7T → $3.3T.

$2T interest = 40% of all government revenue.

What household or company do you know that can survive paying 40% of its income just to credit card interest without going bankrupt?

1/ Cutting expenses? Elon tried with DOGE and even he couldn’t structurally bend the US budget. SS, Healthcare, Defense — all politically radioactive. With interest expense heading toward 40% of revenues and $2T+ deficits locked in, stabilization looks impossible.

2/ There’s only one cut with zero voter backlash: interest rates.

Zero rates = near-zero interest expense, breathing room on the deficit.

Reality: Governments choose self-preservation over solvency. Yield Curve Control (YCC) is coming. Negative real rates + debt monetization incoming.

Wildly bullish for Gold & precious metals miners. If you follow me, get ready to hear more about miners. 🚀