Thanks to @Share_Talk for publishing this brief #EPP article… perhaps a more expansive write up is needed on what to expect for the next steps of MESH and the way in which Energy infrastructure projects like these accrue market value on their derisking journey.

In response to EnergyPathways’ #EPP new corporate investor presentation, SP Angel has produced a comprehensive research note outlining the sheer scale and value proposition of the MESH Project for investors.

The MESH project is expected to be Britain's largest integrated energy storage project and will bolster Britain's energy security and lower consumer bills. Designated a project of "national significance" by the UK Government, MESH combines compressed air electrical storage ("CAES") with natural gas and hydrogen storage. Located in the Irish Sea and connected into Barrow-in-Furness, the project utilises large-scale subsea storage, designed to store energy in a highly cost-effective manner. Its licence area has the potential to support the construction of up to 60 sub-surface salt caverns.

Link to New Corporate Presentation: https://t.co/Ls5NWUTsSv

Link to Research Note: https://t.co/J3wVO1bQf9

#EPP #MESH #EnergyTransition #CleanEnergy #EnergyStorage #GasStorage #LDES #CAES @energygovuk

In Glasgow yesterday, EnergyPathways #EPP CEO, Ben Clube signed the gas storage licence for the company’s flagship MESH project in the Irish Sea and onshore at Barrow-in-Furness.

The storage licence (the offer to award was announced last week), spans a substantial offshore area in the Irish Sea, that could support the construction of up to 60 large-scale, sub-surface salt storage caverns with potential for multi-terawatt hour energy storage, subject to consents and financing.

#MESH #EnergyTransition #LDES #CAES #GasStorage @energygovuk@NSTAuthority

1️⃣ #EPP MESH Project is A Giant Among Giants … should be £100m+ MC for a start

🛢️Gas production:

Marram is fully appraised gas low CO2 Emission field approximately 46bcf of gas ~ 460 million therms, worth over £500 million (Gas prices currently at £1.2/therm)

🛢️Gas Storage:

MESH also boasts a gas storage capacity of 50BCF to 60BCF (500m to 600m therms), potentially tripling to 150 BCF with the addition of Knox and Lowry assets.

This is an impressive capacity of around 500 million to 600 million therms. Equivalent to 15 TWh to 20TWh, that is well over 2/3 of the UK storage capacity

🇬🇧 This positions it as the largest gas storage facility in the UK.

✅ Gas Storage Licence now granted

🔋Green Hydrogen:

With a hydrogen storage capacity of 2.8 TWh (expandable to 8.4TWh), MESH dwarfs other projects.

How will they do it:

💨 Harness the surplus wind energy

🔋Turn it into Hydrogen

🔋Store it

✅ Use it as green source of energy when it’s needed

🔋Capacity to store 2.8TWh hydrogen

❎ Company is looking to triple that capacity to 8.4TWh.

⛽️ Hydrogen: 20,000 tonnes/year ≈ 20,000,000 kg/year

⛰️ Graphite: 60,000 tonnes/year

💴 Use of benchmark price assumptions:

Hydrogen: cost ranges of £3-£5/kg for green hydrogen by ~2030.

Graphite: Recent UK/Europe natural graphite price around US$1,425/tonne (≈ £1,150/tonne at rough conversion)

💴 Revenue Estimate:

⛽️ Hydrogen:

If we assume selling price = £4/kg (mid-range estimate)

20,000,000 kg × £4/kg = £80,000,000 per annum

⛰️ Graphite:

60,000 tonnes × £1,150/tonne = £69,000,000 per annum

Combined Revenue Estimate

£80m (Hydrogen) + £69m (Graphite) = £149 million per annum

2️⃣ Funding

💴 #EPP has signed an MoU with a corner stone Fund to finance MESH at multiples the current SP alongside

🤝 EPP are also in discussion with a FTSE100 for the provision of project Debt finance

💷 EPP has also access to £15m Debt/ATM facility

All of the above will ensure minimal dilution & funding for the MESH project without the need to Gov funding or tax payers money. Although discussion are ongoing & at pace, nothing is very guaranteed until it is all signed up.

3️⃣Comparison Vs peers:

Comparisons with other gas storage projects underscore MESH’s potential. For instance;

🪫BP’s recent partnership with a Spanish company involves a 25 MW project (200 GWh), making MESH 75 times larger

💷 Star Energy’s 10 BCF facility was valued at £340 million in 2007 (£642 million today).

💷 #KIST acquired a gas storage asset with a capacity of 17 million therms for £25 million in the summer of 2024. MESH has a capacity of 500m to 600m therms) that is 28 to 35 times bigger.

🧮This valuation suggests that MESH, with its capacity of 500/600 million therms 28/35 times larger, gives MESH a value at approximately £700m to £875m.

4️⃣Revenue Potential:

💷 Centrica’s Rough field which is equivalent to the size of MESH(50 bcf capacity) generates approximately £312 million in annual revenue.

💷 MESH could generate £320m a year from the gas storage alone, and around £360m from Hydrogen, combined this could be a mouth watering £680m a year.

❎ If the company triples the storage capacity, it could yields 2 billion annually from gas and hydrogen combined.

Add to the above a Combined Revenue Estimate

£80m (Hydrogen) + £69m (Graphite) = £149 million per annum

5️⃣BOD:

Under Ben’s Leadership FAR reached a market capitalization of A$655 million (£334 million).

🤝 He secured a joint venture deal with Cairn Energy and ConocoPhillips, valued at $200 million.

🛢️FAR was recognised as the most successful Australian oil explorer for over a decade

🛢️FAR also made the world’s biggest gas discovery in 2014

All for a ridiculous £12m mc .., £100m+ awaits.

#EPP 🚨RNS 🚨 it’s showtime!!!

This is the moment the market should be paying attention.

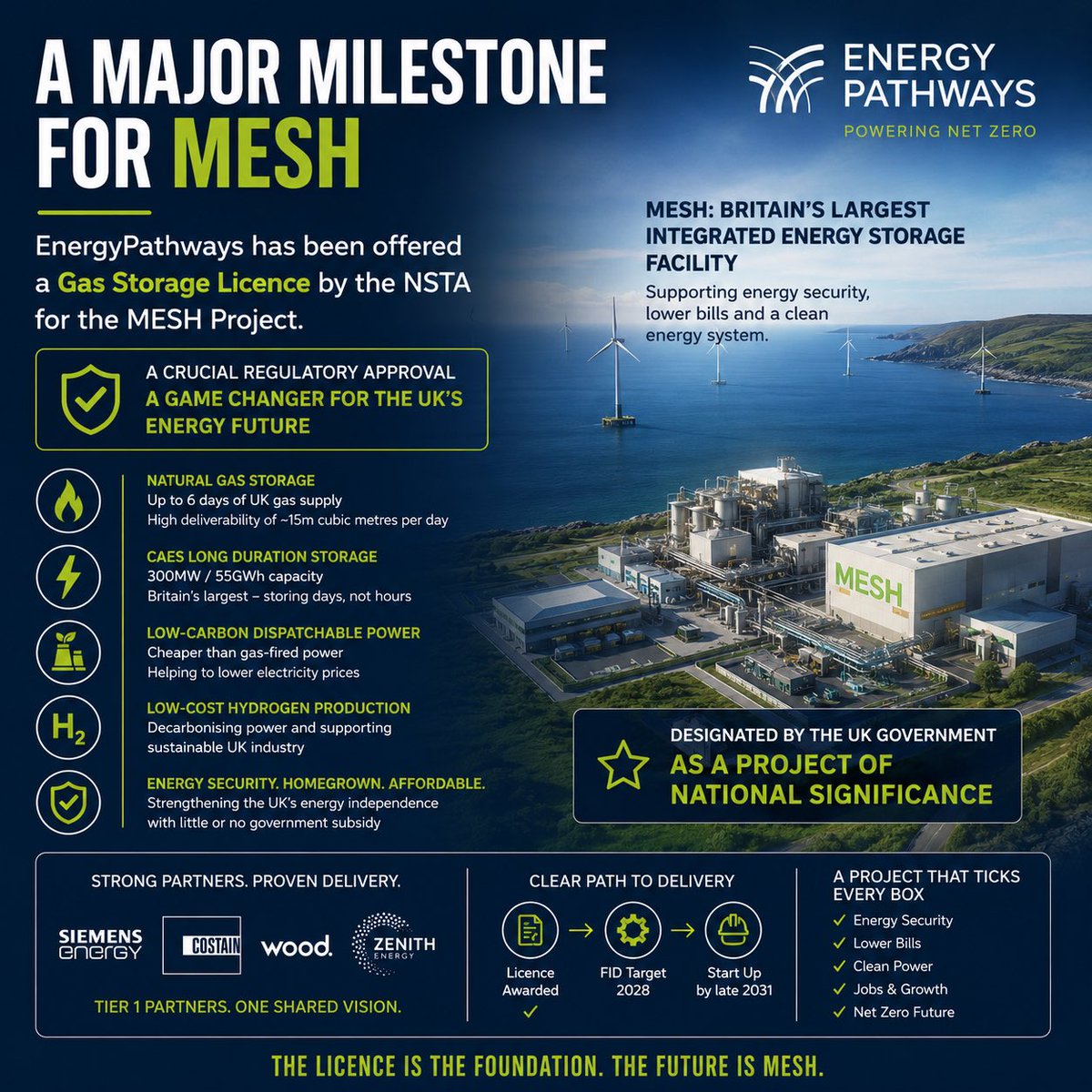

EnergyPathways has been offered a Gas Storage Licence by the NSTA for MESH.

That’s not just a tick box it removes one of the biggest risks hanging over the entire project.

We’re now looking at:

• Up to 60 salt caverns

• Multi-TWh storage potential

• 6 days of UK gas supply capacity

Let that sink in… this is national infrastructure scale.

Gas storage is commercially viable on its own

CAES is commercially viable on its own

Two standalone revenue engines, one integrated project.

• “Nationally significant” UK Government backing

• Tier 1 partners already involved

• Exposure to energy security, storage & hydrogen and you’ve got a project sitting right in the middle of the UK’s biggest energy themes.

https://t.co/WWVb79TWnz

Our CEO Glenn Corrie has shared a new letter outlining how the global energy landscape is shifting — and why the next phase of the transition will be defined by energy security, affordability and scalability.

Read the full letter below 👇

https://t.co/dJXLeDyyfP

$HZR

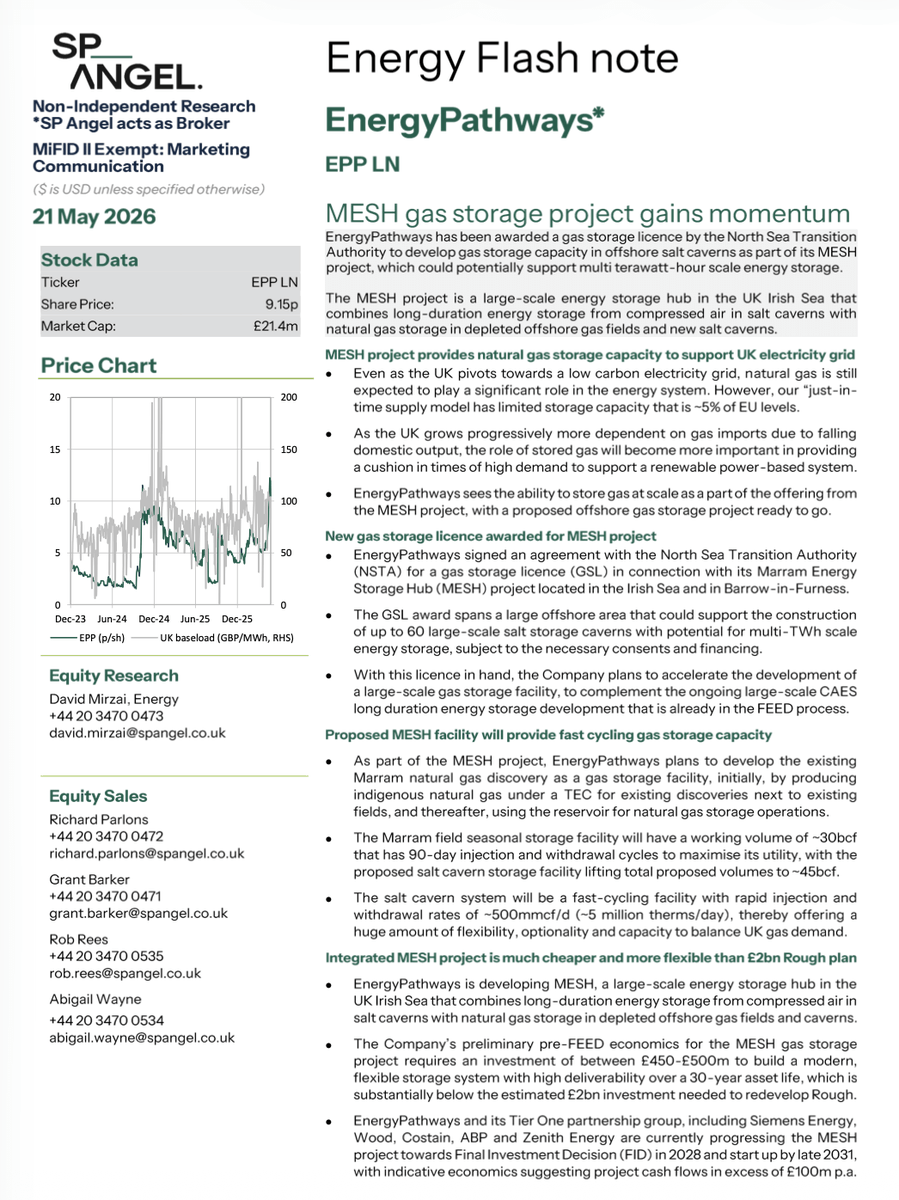

EnergyPathways #EPP is delighted to announce it is to be awarded a Gas Storage License (GSL) by the North Sea Transition Authority for its flagship MESH project located in the East Irish Sea and onshore in Barrow-in-Furness.

This decision marks a major milestone in the development of the wider MESH project, with the GSL spanning a substantial offshore area that could support up to 60 large-scale salt storage caverns with potential for multi terawatt-hour scale energy storage and is expected to be Britain’s largest integrated energy storage facility.

The planned MESH Project has already been designated by the UK Government as a project of “national significance” and will comprise compressed air energy storage (CAES), natural gas storage transitioning to hydrogen storage and complementary hydrogen production for clean power and sustainable industry uses.

EnergyPathways plans the following:

· A natural gas storage facility that will double Britain’s meagre gas storage capacity and provide up to 6 days of national energy supply, securing Britain’s energy future and reducing its over-dependence on expensive gas imports.

· CAES storage of 300 MW / 55 GWh capacity, which is expected to be Britain’s largest LDES facility. This will provide game-changing “days not hours” of electrical storage, essential to harness the billions of pounds of wind power currently being wasted and passed on to consumer bills;

· Low-carbon dispatchable power generation that will be far cheaper than the expensive gas-fired power upon which Britain relies and which sets the power prices for all of Britain’s electricity, including renewables;

· Low-cost hydrogen production capability that will be used to further decarbonise MESH dispatchable power and new sustainable industries planned in Barrow-in-Furness, including EnergyPathways’ proposed graphite production plant; and

· A project that delivers homegrown energy and requires little or no government support at no added cost to consumer bills.

EnergyPathways, along with its Tier One partners, including Siemens Energy, Costain plc, Wood plc and Zenith Energy will now progress the MESH project to a Final Investment Decision in 2028 and start up by late 2031. The Company has already initiated several funding and capacity offtake discussions.

EnergyPathways CEO, Ben Clube said:

“I am delighted that we have met the NSTA’s criteria to offer EnergyPathways this crucial Gas Storage Licence, one of only two NSTA energy licence awards in the last two years.

“The UK Government recognises MESH and other forms of long-duration energy storage as having a vital role in lowering energy prices, bolstering energy security and achieving a clean energy system."

#MESH #EnergyStorage #CleanEnergy #LDES #GasStorage @energygovuk@Siemens_Energy@CostainGroup@ZenithEnergy

@thetimes: Strait of Hormuz blockade is causing a fertiliser crisis

UK lost sovereign fertiliser capability in 2013 and imports 100% of it's ammonia.

@energy_pathways current projection 110,000 tonnes Ammonia pa, (est. £55 - £100m rev) 👀

#EPP#MESH

https://t.co/CI0e3KiulD

#EPP news is big

#EPP just de-risked its flagship project in a BIG way. Pre-FEED completed with Siemens Energy confirming economic viability, that’s not hype, that’s hard engineering + numbers backing it.

Now they’ve officially launched FEED 🚀

💴 Funded

➡️ Minimally dilutive (£15m)

📅 Clear path to FID in 2028

And what are they building?

⚡ Potentially the WORLD’S LARGEST CAES project

⚡ 300MW / 55GWh (!!) multi-day storage

⚡ Critical solution to the UK’s renewable curtailment problem

This directly targets one of the biggest inefficiencies in the UK grid today: wasted wind energy costing billions annually.

What’s even more bullish:

🇬🇧 The wider MESH project has “national significance” status

🏦 Interest already coming from major global project finance banks

📊 Positioned for Ofgem’s LDES cap & floor scheme (huge for revenue visibility)

And here’s the kicker…

CAES can does not need the gas storage licence …

This is how billion-pound infrastructure stories start, early validation, strategic funding, institutional interest… then scale.

Market cap vs potential here? Doesn’t look aligned. Expect a re-rate to kick off once market start to click.

#EPP is no longer just a concept, it’s moving into execution with one of the most important energy storage assets in the UK.

DYOR, but this just got very interesting 🔥

So let’s look closer at #EPP EnergyPathways

Progressing and not reliant on the gas storage license:

World’s Largest CAES project (UK’s largest LDES): Based on the storage capacity, output duration and benefitting from massive curtailed wind energy, estimates for revenue pa are around £150m+ (may be higher with cavern expansion and government subsidy or cap and floor benefits)

The Irish Sea has two huge wind farms to come online in the shape of Mona and Morgan. So expansion of the salt caverns with Siemens Energy is likely. Also EPP own the IP for CAES tech.

The project lifespan is 25 years+ so LDES alone is a company maker.

Reliant on Gas Storage License:

Gas Production: Marram alone has 46BCF of gas, based on current spot pricing that’s worth £500m (this doesn’t include Knox or Lowry fields) the figure will be a little lower due to the provision of cushion gas needed to facilitate storage.

46BCF is just natural gas and doesn’t include nitrogen in the mix which will be utilised to create clean ammonia.

Gas Storage: Marram alone has the equivalent storage capacity of Centrica’s Rough Facility 50-60BCF

The revenue value of gas storage is based not just on gas in place, but the opportunity for volatility trading (fill with cheap summer gas to sell on winter peaks)

Based on Marram alone annual revenues are approx £400m+ (but based on the UK’s low gas storage capacity this is conservative)

Hydrogen/Ammonia: This is a harder market to asses as an emerging sector. So based on the initial projected feedstock of 20,000 tonnes let’s value it when it’s used to create Ammonia as that market is very real.

Production of 110,000 tonnes pa is projected. The last domestic UK ammonia producer closed in 2023 and as of 2027 there’ll be a border levy on imports so this will affect chemical & farming Industries. Annual revenues for ammonia, based on volatile pricing could be between £55-100m pa.

Graphite: High grade synthetic Graphite (circa 60,000 tonnes pa) is set to be refined (With Mitsui Japan) to create nuclear/military grade graphite, elevating the price dramatically. Company estimates revenues of £500m pa

EnergyPathways has a suite of revenue streams offering diversification through products and industries at a time where they’ll be the only domestic producer of graphite and ammonia, they’ll effectively be doubling the UK energy storage capacity at a time of critical need and urgent demand. And it requires little or no government funding (however GB Energy or National Wealth Fund may invest)

The offering is also diverse enough to be valuable to any government from Labour to Reform so it is in effect apolitical. (Is Reform going to turn down homegrown North Sea gas, domestic graphite for defence and Ammonia for Jeremy Clarkson and the farming community?)

The tier one partnerships with Siemens Energy, Wood & Costain give the project credibility in the eyes of the government, as does the fact the world’s and UK’s largest CAES/LDES facility is going ahead at pace and it makes the project very real.

MESH is proposed as the flagship project for EPP and Siemens and “one of many” projects that will target favourable geology/infrastructure in the North Sea Continental Shelf.

The risk is that the storage license won’t be granted… But that would require the government to decline something they critically need and requires little or no taxpayer subsidy. They’d have to have a damn good reason to decline.

The second argument is that “it’s not operating until 2030, so why buy now”, the counter is that at £12m MCAP, when project level funding hits and the GSL is granted and the government and media takes up the story this stops being worth £12m.

The project will no longer be a “retail” focussed stock and with projected yields for investors to be 25% per annum over a 25 year lifespan then pension funds, institutions and family offices take over the register, and they invest for significant and sustained future growth not a quick 10% slice.

As per Tuesday’s #EPP RNS “Worlds largest CAES and UK’s largest LDES RNS”

The initial draw down of funds to progress the project has been advanced.

More interestingly is the passage: “Additionally, a sum of money has been set aside to fulfil the Company’s proposed work commitments set out in its gas storage licence application, for which a decision is pending fromthe North Sea Transition Authority (NSTA).”

https://t.co/hc2oNZdAG1

RNS: EnergyPathways #EPP Launches FEED for the World’s Largest CAES and the UK's Largest LDES Project

EnergyPathways and @Siemens_Energy confirm commercial viability of the MESH Compressed Air Energy Storage (CAES) project. FEED has been launched, funded by a £15m Financing Agreement.

CAES Project Highlights:

• A 300 MW CAES facility with 55 GWh storage capacity, offering multiday discharge capability and critical grid stability services.

• Project commerciality and economic viability confirmed with EPP’s major project technology partner Siemens Energy.

• The Gas Storage Licence award decision is not required for this project to proceed.

• Participation in Ofgem’s LDES cap and floor second round expected to commence later this year.

• FID planned for 2028 with operational startup at the end of 2031, subject to regulatory approvals.

• Requires little or no government/taxpayer subsidy.

• Local support received for MESH planned onshore facilities from “Team Barrow”, a private/public partnership to strengthen and diversify Barrow-in-Furness’ economy.

• A £15 million financing agreement in place to fund FEED. Expressions of Interest for project financing also received from leading global banks and project financing discussions are underway.

The MESH CAES Facility

The MESH CAES facility is expected to be the world's largest CAES facility and Britain's largest LDES project, and will have a power capacity of around 300 MW and energy capacity of 55.2 GWh, providing over 7 days of sustained power output.

The facility will use surplus power from Britain's grid and nearby offshore wind farms to compress air into large, purpose-built, offshore salt caverns. When required, the stored air will be withdrawn, heated and expanded, via a high‑efficiency cycle turbine designed for hydrogen fuel heating, to generate decarbonised dispatchable power.

An onshore sustainable industry park will be developed at Barrow-in-Furness to support the MESH project. It will include the CAES storage operations base as well as a low carbon hydrogen and graphite production facility.

Ben Clube, CEO of EnergyPathways, said:

"I am delighted to kick off the FEED programme for our MESH CAES project. This project, when brought online, will be an invaluable asset for the UK's electricity network and will help deliver the objective for a clean energy system.

Importantly, we expect UK consumers will see the benefits of our CAES project through lower power bills. By harnessing Britain's abundant wasted wind power, it can be used to produce low-cost dispatchable power to reduce our dependency on expensive gas imports for our power supply.”

#CleanEnergy #LDES #CAES #EnergyStorage #MESH @energygovuk@ZenithEnergy@ofgem

We've just released the following announcement: EnergyPathways PLC - CAES Project Update & £15m Financing Agreement

Check out the full announcement and join in with the conversation at: https://t.co/vKalCcIgQ5

#EPP