Chris Mayer on margin of safety

"Margin of safety comes primarily from the quality of the business with a combination of a good entry price.”

Margin of safety is not just a 30% discount, it's also about owning the right businesses

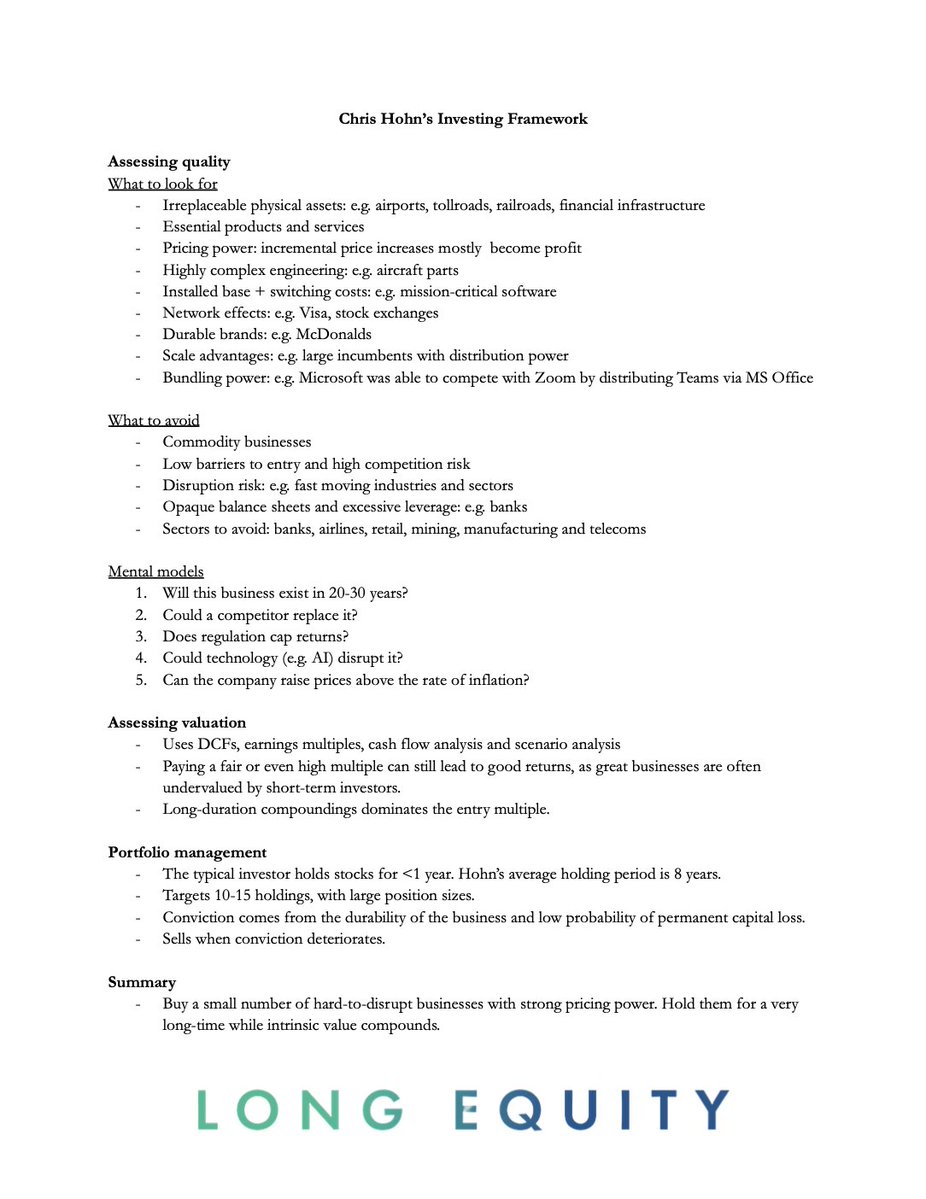

I recently rewatched a great interview with Chris Hohn (TCI Fund), as well as reading the recent FT article. Here are my notes on how he invests:

What would you add?

This is a terrific article by @CostasMourselas & @ameliajpollard about legendary hedge fund manager Sir Chris Hohn. It's full of rich insights into his character, his high-conviction investment style, his passion for philanthropy & his friendship with Warren Buffett (who shares his devotion to Moody's). For example:

Extract #1: "He had little doubt of his destiny, he says. 'Bob Dylan said from a young age . . . he knew he was going to be successful. He was operating in intuition,' says Hohn. 'My intuition, which is the intelligence of the soul, said my purpose here was to help people.' On a simpler level, he loved investing, calling it 'one of the purest ways to apply intellect to making money.'”

Extract #2: "For Hohn, the key metric for any company is pricing power, highly valuing the ability to push through inflation-busting price increases. He is not dazzled by stratospheric revenue growth like other investors. 'Chris likes buying global monopolies or duopolies,' says TCI analyst Ben Walker.' His investment style is also partly informed by a desire for control. Like Buffett, he thinks of himself as an 'owner' of his stocks, rather than a speculator, and it is from this mindset that he acts as an activist to defend his interests in a company. For instance, Hohn does not like to short, or bet against, stocks, because the investor on the other side of the bet can recall their shares at any time and crystallise a loss. Short sellers can also be subject to short squeezes, where investors target them by buying the stocks they are betting against, forcing them to close their position. 'I don’t like to hold my destiny to other people,' he says."

Extract #3: “I learnt over the last 20 years that you are better off to find a great company which is well managed and well governed than try to find a bad company and change the management or sell the company,” Hohn says.

https://t.co/Y8GKZFcCJ2

Thoughts on $SPGI

Revenue grew 10% and EPS grew 14%, and margins expanded again, which is exactly what you want to see at this scale. This isn’t growth you have to question or adjust, it’s growth that converts directly into profit. That’s always the first signal you’re dealing with something high quality.

When you look deeper, the operating leverage really stands out. Operating profit grew 27% on just 10% revenue growth, which tells you a lot about the underlying economics. That only happens when you have real pricing power and very low incremental costs.

The growth is also coming from the right places. Ratings grew 13%, Market Intelligence grew 8%, and Indices grew 17%, each with very different characteristics. Together they create a model that is both durable and scalable, with transaction upside, recurring revenue, and asset linked growth all feeding into each other. That combination is very hard to replicate.

Indices is really the crown jewel here and they are still underestimated. Asset linked fees grew 18%, which basically means as more money flows into ETFs and passive investing, $SPGI gets paid. There is almost no incremental cost, so most of that revenue turns into profit. It’s not just a good business, it’s a toll road on global capital flows, and those flows continue to move in one direction over time.

What’s important to understand is that this is not really just a ratings business anymore. It’s a data, benchmark, and workflow tied to global capital markets.

The reason margins can stay this high is because the product actually improves with scale. Every new issuance, every ETF, every dataset strengthens the moat. Instead of competition compressing returns, scale reinforces them. That’s a very different dynamic than most businesses.

There is also a simple but powerful structural tailwind here. Every dollar that moves from active to passive is effectively a small tax paid to $SPGI. You don’t need to predict markets perfectly, you just need to understand where capital is flowing. Over time, that flow continues to benefit them.

Capital allocation is good, they bought back $1b of stock and are planning to return 100% or more of free cash flow this year through buybacks and dividends. Free cash flow was about $919m, which shows how little this business needs to reinvest to keep growing. That combination of high margins and high returns is where the long term compounding happens.

They have $1.8b in cash and continue to generate consistent, high quality cash flows. This is not a business that needs heavy reinvestment so it funds growth internally and still sends a large portion of cash back to shareholders. That’s a very powerful position to be in.

They expect 6% to 8% revenue growth and EPS around $19.50, which on the surface may not look exciting. But considering margins, buybacks, and capital returns, you still get strong EPS compounding over time. This is not a hypergrowth story, it’s a durability story.

Strategically, they are simplifying the business. The mobility spin off and energy asset sales suggest a focus on higher return segments and better structure. Over time, that usually leads to a better business and often a higher multiple if execution is solid. It also makes the story easier to understand.

There is also a second order dynamic that is easy to miss. The more volatility and uncertainty you have in global markets, the more people rely on benchmarks, ratings, and data to make decisions. In other words, the same conditions that hurt most businesses can actually increase the relevance of $SPGI. That’s a very unique position.

Of course, there are risks. Ratings is still tied to debt issuance cycles, competition will evolve especially with AI, and margins won’t expand forever from these levels because they are already very high. But those are normal tradeoffs for a business of this quality. The key question is not whether it’s perfect, but whether the core advantages remain intact.

🌹

I genuinely hate earnings season. It’s fine to get an update on how the business performed over the last 90 days, but it comes with so much noise. Excitement, optimism, pessimism, overreactions, and endless opinions, it’s largely a distraction.

The biggest mistake people make is treating earnings like the end game when it’s really just a temporary scorecard. A single quarter tells you almost nothing about the long term trajectory of a business. Stocks can move 10% or more overnight while the actual value of the business barely changes (both to the upside and to the downside).

Businesses don’t move in a straight line. Sometimes you get a tailwind, sometimes a headwind. Some quarters are strong, some are weak. That’s just the reality of operating in the real world.

What actually matters is free cash flow per share and the underlying economics of the business. Buybacks, dilution, reinvestment, returns on capital, etc. That’s where the real compounding happens, not whether EPS missed by a few cents.

If you owned 100% of a private business, you wouldn’t care about one quarter. You’d care about what it earns over years. Public markets just make people forget that. That’s why earnings season creates so much useless volatility.

🌹

I've just started working on my yearly letter for Feather Fund subscribers. If things don't change a lot by the EoM (of which I'm sceptical), the letter will reflect a terrible underperformance, but it might be fun to read.

#Investing#SP500