Alle Halbleiter Interessierten sollten sich den 22. Juni in den Kalender eintragen. Da findet die virtuelle Industrial Technology Conference von mwb statt.

Mit dabei: u.a. AT&S, Aixtron, LPKF Laser, SUSS MicroTec & Nynomic.

@l_m_s15 Habe das nochmal nachgeschaut. Es scheint als hätten die dafür ganz gute Schallschutzlösungen. Der CFO hat es allemal so klingen lassen, als wäre die Innenstadtoption das Unterscheidungsmerkmal zu anderen Herstellern.

@l_m_s15 Er hat auch hervorgehoben, dass sie die beste kWh-Leistung pro qm haben. Könnte für urbane Datenzentren ein entscheidender Verkaufspunkt sein.

@l_m_s15 The future of ukraines energy infrastructure will lie in decentralized power plants" (currently bombed out soviet power plants).

Fand ich sehr interessant

@MoodyWriter13 Riding many trends, presentation has 300 views on yt from mid-May.

I found this quote compelling:

"The future of urkaine's energy infrsatructure will be based on decentralized power plants"

@MoodyWriter13 I read a lot about they transiton to inference and that being close to the data centre will be important to reduce latency. But gas turbines are too loud, so might this be an ideal solution ?

@MoodyWriter13 He adds this is irrelevant when you are in texas but if you operate a data centre close to urban areas this is essential. -Additionally he mentioned that they are quiet which makes them suitable for urban areas.

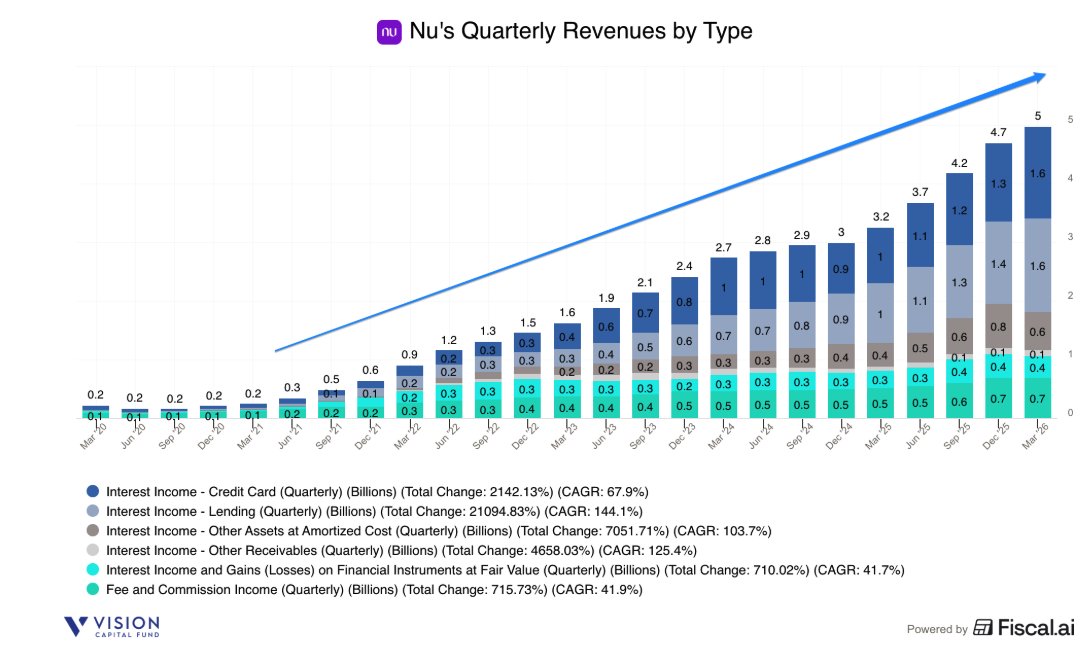

Nu Holdings $NU 1Q26 Earnings

- Rev $5.0b +53% ↗️🟢

- GP $1.9b +41% ↗️🟢 margin 37.8% -308 bps ↘️🔴

- EBT $1.2b +42% ↗️🟢 margin 24.7% -196 bps ↘️🔴

- Net Inc $871m +56% ↗️🟢 margin 17.5% +38 bps ✅

- ROE 29% +200bps ↗️🟢

- Adj ROE 31% +100bps ↗️🟢

- Efficiency Ratio 17.6% -380bps ↘️🟢

Revenue by Type

- Credit Income $3.2b +61% ↗️🟢

- Float Income $1.4b +57% ↗️🟢

- NII $3.3b +61% ↗️🟢

- Risk-adjusted NII $1.5b +50% ↗️🟢

- Credit Loss Allowance $1.8b +72% ⤴️🟢

- NIM 21.1% +190bps ↗️🟢

- Risk-adjusted NIM 9.5% +20bps ↗️🟢

Biz Metrics

- Total Cust 135.2m +14% ↗️🟡

- Brazil 115.5m +10% ↗️🟡

- Brazil (Individual Cust) 109.1m +9% ↗️🟡

- Brazil (SME Cust) 6.4m +31% ↗️🟢

- Mexico Cust 15m +36% ↗️🟢

- Colombia Cust 4.7m +62% ↗️🟢

- Activity Rate 83.4% +20bps ↗️🟢

- Total Active Cust 112.8m +14% ↗️🟡

- Active Cust - Credit Card (Consumer + SME) 58.4m +7% ↗️🟡

- Active Cust - Unsecured Lending (Consumer + SME) 15.1m +22% ↗️🟢

- Total Purchase Volume $39.5b +30% ↗️🟢

- PV (Credit Card) $27b +36% ↗️🟢

- PV (Debit Card) $12.5b +18% ↗️🟢

- Mthly Avg Rev Per Active Cust $15.9 +37% ↗️🟢

- Mthly Avg Cost Per Active Cust $1.0 +43% ➡️🟢

Credit Metrics

- NPL 15-90 5.0% +20bps ↗️🟠

- NPL 90+ 6.5% +10bps ↗️🟠

Credit Portfolio by Type

- Credit Portfolio $37.2b +54% ↗️🟢

- Credit Card $24.3b +49% ↗️🟢

- Loans $12.9b +64% ↗️🟢

- Loans (Unsecured) $9.9b +68% ↗️🟢

- Loans (Secured) $3b +58% ↗️🟢

Interest Earning Portfolio (IEP) by Type

- Total IEP $22b +59% ↗️🟢

- Credit Card non-IEP $15.2b +48% ↗️🟢

- Credit Card IEP $9.1b +52% ↗️🟢

- Loans to customers $12.9b +64% ↗️🟢

Deposits by Geography

- Deposits $42.4b +34% ↗️🟢

- Brazil $33.7b +38% ↗️🟢

- Mexico $5.9b +9% ↗️🟡

- Colombia $2.8b +56% ↗️🟢

- Cost of Deposits 88% of Interbank Rate ➡️🟢

- Loan to Deposits (LDR) 58.3% +980bps 📶🟢

1 | Same playbook of growing ARPAC vs keeping ACPAC combined with strong operating leverage in decreasing efficiency ratio to drive growing profitability

For several years now, our results have followed the same earnings-generating formula: a growing, more engaged customer base, monetized at higher ARPAC on a scalable low-cost platform translating into outsized earnings…Customer growth combined with ARPAC expansion, which has expanded sequentially every quarter since we began reporting and now sits at around $16 per active customer, compounded into record revenue, reaching $5 billion for the first time in our history. The higher revenue translated into strong operating leverage in the quarter, leading to a record low efficiency ratio below 18%..

2 | Seasonality, growth, and mix drove higher provisions, and do not see credit portfolio deteriorating in asset quality.

Bringing it all together, the three drivers we just walked through, 1, seasonality, 2, growth, and 3, mix, are exactly what shaped the moves in NPL 15-90 and in ECL allowance this quarter. There was no sign of credit portfolio degradation.

Together, growth and seasonality account for 86% of the entire allowance increase. Intentional risk expansion contributed $69 million, product mix, $16 million, and other minor effects, the small remainder. Now, not one of those components reflects deterioration in underlying credit quality.

3 | Nu tends to be extremely conservative about how they build in their credit provisions, regardless of where they are in the credit cycle.

Look, we feel that our balance sheet is fairly robust. We try to be extremely conservative in how we build our provisions over time. I have also to say that the provisioning that we have been doing over the past quarters, they do not reflect any directional outlook that we have on the credit cycle of each of the markets in which you operate. The way that we have tried to, you know, do credit underwriting and consequently to do credit provisioning, is one where we always assume that the future will be worse than the past, irrespective of where any of us think we may be in the credit cycle.

4 | The unit economics of the three main unsecured credit products remain solid, and duration remains lower, allowing them to have the agility to adjust when needed.

you can see the unit economics of our 3 core unsecured credit products, namely credit cards in Brazil, unsecured lending in Brazil, and credit cards in Mexico. Right? They account for the majority of our unsecured exposure. I would, you know, underscore 2 things. First, if you go through their unit economics, it's kind of a healthy unit economics in our view, but more importantly, if you take a look at the ratio between losses and the net margin, you can see that they can withstand a lot of risk worsening and still being NPV positive. Right? If you take a look at the duration of each of those portfolios, we operate intentionally with much lower duration than the average of the market. This is a feature that is not a bug. Why? Because it allow us to navigate with lots of agility at a very granular level. All this to say that we are provisioning conservatively as we have provisioned in the past. Nothing has changed.

5 | See the recent income tax exemption or reduction and Desenrola 2.0 to be a tailwind and neutral to positive.

The first one is the income tax exemption or reduction that has been announced in Brazil at the beginning of this year that basically benefits consumers with up to BRL 7,400 per month of income. It may very well be a tailwind for us. It's hard to calibrate the magnitude, but that has not been taken into account in the provisions and credit results before.

The second one is the Desenrola 2.0 that we briefly mentioned, and you also wrote about it, that

I think can be a fairly important kind of a renegotiation tool sponsored by the federal government

for our customers, which we believe can be, for Nubank, either neutral or positive.

6 | Brazil remains the largest market for Nu, and there is a long growth runway. The addressable profit pool exceeds $100 billion in annual gross profits, and Nu currently only has a 7% share of it.

With that as our backdrop, let me start with our biggest market, where we still have a long road ahead of us. Brazil is, by any measure, one of the most attractive banking markets in the world. Across just the products and segments we serve today, the addressable profit pool already exceeds $100 billion in annual gross profit and is expected to keep showing healthy growth for years to come. As we expand our product shelf and deepen customer engagement, that profit pool becomes even larger. Even after a year of meaningful share gains, it's still day one for Nubank in Brazil. Our share of that pool stands at roughly 7%, even though we're already the largest private financial institution in Brazil by customer base, with the strongest brand and the highest customer satisfaction scores.

7 | In Mexico, the runway is even larger. The profit pool exceeds $40 billion in annual gross profits, and Nu today only has below 1% of it.

In our second-largest market, the runway is even bigger. The opportunity in Mexico is, in many ways, where Brazil was one decade ago. The profit pool of the products we want to serve consumers with already exceeds $40 billion in annual gross profit and is growing faster than most major banking markets in the world. The banking system in Mexico remains structurally under-penetrated. Cash still dominates everyday transactions. Less than half of adults hold a formal credit product, and a meaningful portion of the population still lacks access to banking. Our share of that profit pool is still below 1% today, a fraction of where we are in Brazil and a fraction of where we believe we can go.

8 | For Mexico, it is even more particularly compelling because Nu is actually helping the market to grow with digital banking.

What makes this opportunity particularly compelling is the dual dynamic at play. We're not only taking share of the existing pie, we're also helping grow it, bringing simple, digital, transparent financial products to broader segments of the population that have historically been left out of the formal banking system. That combination is what gives us such a long horizon ahead, and the proof of that thesis is already starting to show up in the numbers.

9 | Mexico's unit economics continue to improve. ARPAC has nearly doubled, and they have now moved from a quarterly loss to their first quarter of profitability ahead of plans.

The same earnings-generating formula I described at the start of our remarks is now unfolding in Mexico, only earlier in its curve. In four years, our customer base there has grown from just over 2 million to 15 million today, roughly 7 times larger. ARPAC has nearly doubled, even as we have onboarded millions of newer, less mature customers. Our efficiency ratio has come down by 78 percentage points. On the bottom line, we have moved from a $30 million quarterly loss to our first quarter of IFRS profitability, a milestone that arrived ahead of our own internal plan.

10 | It is underappreciated that Nubank has actually built one of the largest SME customer bases in Brazil with zero CAC, see it as blue ocean underserved customer segment, and have ambitious plans to grow this business.

I actually think this is probably one of the most underappreciated opportunities we have at Nu. We should be speaking more about it, but we're not so thank you for asking the question. The reality is we've kind of silently have built the largest SME base in Brazil with over 5 million SME customers, effectively built with 0 customer acquisition cost. Since Brazil has a very large number of SME, a significant percentage of employment in Brazil, something like upwards of 70% operates in small businesses.

A very large percentage of over 110 million customers have their own businesses, so we were able to cross-sell SME product to them, and that took us at a 0 CAC to build this base of upwards of 5 million customers…We see a blue ocean in that space, really. SME. This is a very underserved segment. I think we're also, while we began at the base of the pyramid with the very small micro entrepreneurs, we've been slowly going up the base and starting to serve companies that have more than 10 to 15 employees. I'll leave it at that for now, but we have an ambitious plan on that space.

11 | Using AI to really rebuild Nu in three phases: AI assistant, Workflow reinvention, and AI native bank. The first phase is nearly complete. The second phase is currently in motion, and the third phase foundations are increasingly visible.

We're applying the same logic to AI. We're not just adding AI to banking. We're rebuilding banking around AI. This transformation is already underway and unfolding in three phases at different stages of progress. The first phase, AI assistance, is largely complete. We're reaching close to 100% utilization of AI tools among our employees across all functions of the organization. This enablement is driving productivity gains across the company, with engineering throughput up over 50% YoY, weekly token consumption nearly 10 times higher than at the start of the year, and testing cycles 90% faster.

The second phase, workflow reinvention, is in motion. The principle is simple: AI executes, humans hold judgment. Customer journeys are being rebuilt end to end, and new AI-native customer experiences will reach our customers this year, deepening engagement and expanding monetization. A number of teams at Nubank are already working on products and features that we had originally planned to launch only in mid-2027.

The third phase, the AI-native bank, is still early, but the foundations are visible. AI Private Banker functionalities, such as financial insights, payments, credit advice, and debt resolution across the app, are already serving more than 15 million monthly active users. NuFormer, our set of proprietary foundation models, are in production today for credit card decisioning in Brazil and Mexico and for unsecured lending in Brazil.

12 | Nu is now using real-time AI evaluation for every personal loan request and is able to do it at quickly and at scale.

We're now able to use real-time AI valuation for every personal loan request, priced and approved individually based on its predictive net present value in under 1 second. These capabilities have been a meaningful driver of the significant expansion in our credit portfolio over the last 12 months, enabling us to grow limits with resilience, not just speed.

13 | Nu is uniquely positioned to win the AI-accelerated world, anchored by three structural advantages: Skilled first-party data, their proprietary technology stack, and their talent and culture that is focused on a single AI mandate.

We believe Nu is uniquely positioned to win AI-accelerated world, anchored by 3 structural advantages. First, our scaled first-party data. 135 million customers transacting on our platform every day, generating 1 of the largest, cleanest, and most differentiated financial data sets in the world.

Second, our proprietary technology stack, cloud native with core banking systems built internally, data unified across the company, and the ability to move from experiment to production in days rather than quarters.

Third, our talent and culture, a world-class bench of employees from more than 50 nationalities with offices across 6 countries, all working under a single AI mandate, and one we keep reinforcing with the recent appointment of Carl Rivera as our new Chief Product Officer. AI is not an experiment at Nubank. It is reshaping how we build, how we decide, and how we deserve, and we're still very early in what this transformation will eventually deliver.

14 | Credit portfolios have a much shorter duration, allowing them to react faster, more decisively, and at much more granular levels before they become a systemic issue.

With a significant buffer, these portfolios remain NPV positive even at substantially higher levels of expected losses. The short duration of these portfolios is worth pausing on. Why? Because it means that if we ever did observe unexpected asset quality movements, we can react fast and we can react decisively, and we can do so at very granular levels well before they become a systemic issue. We are not a long book lender waiting quarters and quarters to see the impact of a credit policy change. We see it in days, and we act on it immediately. That is what grounds our strategy.

15 | See the opportunity to expand the US as highly asymmetric as a call option with limited downside and unlimited upside, and the maximum downside is an OPEX headwind of <100bps of the consolidated efficiency ratio.

That is why we are excited to be expanding our model to the U.S., deliberately and at a measured pace, treating it the way we treat every new market, as a call option. We invest a relatively small amount of capital and resources while we protect our core. Once we see product market fit, we're ready to scale. To be precise, the maximum OPEX headwind we expect from U.S. investment in each of 2026 and 2027 is less than 100bps on our consolidated efficiency ratio. This is inside the 20% efficiency ratio level Lago mentioned before.

For a company at our scale, that is quite affordable. Beyond that, any additional investment is explicitly contingent on clear evidence of product market fit and a credible path to profitable scalability. Even in a scenario where we do not find product market fit, the cost to you as a shareholder is less than 100bps on our efficiency ratio. Temporary and fully absorbable without touching the trajectory of our core businesses.

16 | Expanding to the US will be extremely challenging, as there are many competent competitors, but if NU can get it right, it will be a very huge opportunity to the upside.

The upside, if we do find product market fit, is a second Nu. We have seen this movie before in both Mexico and Colombia. The asymmetry between a bounded downside and an uncapped upside is at the center of our investment thesis in the U.S., and potentially the world, and it does not change our long-term trajectory on efficiency.

I definitely do not want to minimize the challenge that a country like the U.S. will be extremely challenging. There is a lot of very competent competitors, but we think we have an insight, and we'll see how that goes. The good news is that if we're wrong, it's a little loss. If we're right, it's gonna be a huge opportunity for us.

17 | NU thesis TLDR: growing customer base, expanding credit portfolio that is growing profitably and resiliently, combined with a diversified gross profit base and has one of the strongest balance sheets

To wrap it all up, this was another quarter that demonstrated the durability of our business model. Number 1, a growing and engaged customer base. Number 2, an expanding credit portfolio growing profitably and resilient. Number 3, a more diversified gross profit base. Number 4, one of the strongest balance sheets in financial services.

18 | Nubank is incredibly well positioned to strengthen its place as LATAM's leading digital bank, with a long and visible growth runway in their core markets, with a superior cost structure that is 20-30X more efficient than their incumbents that own 90% of the profit pool.

Nubank is incredibly well-positioned to continue strengthening its place as Latin America's leading digital bank. While our consumer base is large, our total market share is still small, that gap represents a long and visible growth runway in our core markets. This remains our number 1 priority. We continue to have conviction that the digital banking thesis we started to execute in 2013 is a global thesis, not a local or regional one. First principles reasoning shows our advantages travel. Our cost structure is 20 to 30 times more efficient than the incumbents that still own 90% of the world's banking market. Our technology gives us the agility to move fast in any environment. Our differentiated approach to credit gives us the tools to compete and grow within a segment that represents over 70% of the world's consumer banking profit pool.

19 | Nubank's primary investor concern is if they can credit underwrite at scale through multiple credit cycles in LATAM, but they have clearly demonstrated that they can across time and in different countries. Credit risk always remains the first priority.

The ones that I would highlight, first is kind of asset quality. I think when Nubank was founded, you know, 13 years ago, The bank had a fairly strong thesis and hypothesis on its ability to do credit underwriting at scale throughout multiple credit cycles in Latin America, which is one of the most volatile regions of the world. It was a hypothesis we couldn't prove at that point in time.

You fast-forward the move, you know, 13, 14 years. I think we can, both in Brazil, in Mexico and in Colombia, already now clearly highlight that we have developed the ability in terms of process, systems and talent to be able to do credit underwriting in a resilient manner at scale. I think the velocity to which Nubank has been able to gain market share has now encouraged or impressed some of them. I think the credit underwriting capabilities of the bank and concerns with no asset quality will always remain, and they should remain, because for any kind of digital bank that has been able to attack credit, we will always have credit risk first in our priority list.

20 | Locals are always very skeptical whenever Nubank launches in a new country, largely because they're just consumed by the status quo.

Well, the only thing I would just add to everything that Lago said on the internationalization is that it's interesting that every time we've launched a new country, the locals have been skeptical. When we launched Brazil, the locals were very skeptical. When we launched Mexico, the locals were very skeptical. The capital came from the foreigners. Sort of the same thing kind of repeats. Sometimes being a local is a little bit of a blessing, sometimes a little bit of a curse. Because if you're a local, by definition, it's very hard for you to reimagine how things can happen differently. You're too consumed by the status quo.

➡️ Final Takeaways on Nu Holdings $NU:

NU is the “GEICO” of LATAM digital banking. Strong business traction supported by 📶 customers, more/faster cross-sell, leading ↗️ revenues per customer, combined with the significant competitive cost advantage of a lower cost to acquire & serve ➡️, strong risk management, and lower cost of funding (retail) that really drives its long-term highly durable profitable growth. Continue to watch its expansion into Mexico and Colombia, and its continued building on its strengths in Brazil (secured lending with payrolls, higher credit card spend with the higher income Ultravioleta credit card. Strategic about entering the US with limited downside and strong upside if they can execute strongly. Not worried about higher near-term (4-6 quarters) expenses of higher efficiency ratios weighing on profitability. If markets give us better buying opportunities, we will gladly take it.