NEW ACCOUNT NOTICE:

For anyone that may have been following me here, please follow my new account @KarmaCollects. Twitter suspended this one, and now unsuspended me (after 4 months of appeals), but I will continue to use the other account moving forward. Please follow it!

@BuurbQ I imagine that “we scummer” encapsulates you and your whole inbred “family” (figurative and literal) over there. Go host another troll space, Brian. I hope when this is over you’ll find meaning in your life outside of being a social media curmudgeon. “Scummer”? What a dork. Smh

FINRA's BS "Enforcement" on Barclays: Why @FINRA is GUILTY of Regulatory Concealment.

We're constantly told America has the most transparent, safest, most secure public markets on the planet, the "gold standard" for investors and companies brave enough to go public. Yet here we are again with FINRA handing out yet another limp slap on the wrist while demonstrating that they don't care AT ALL about market integrity or individual investors. Let's look at this Barclays case, and why this "regulatory action" is a slap in the face to public companies and investors alike.

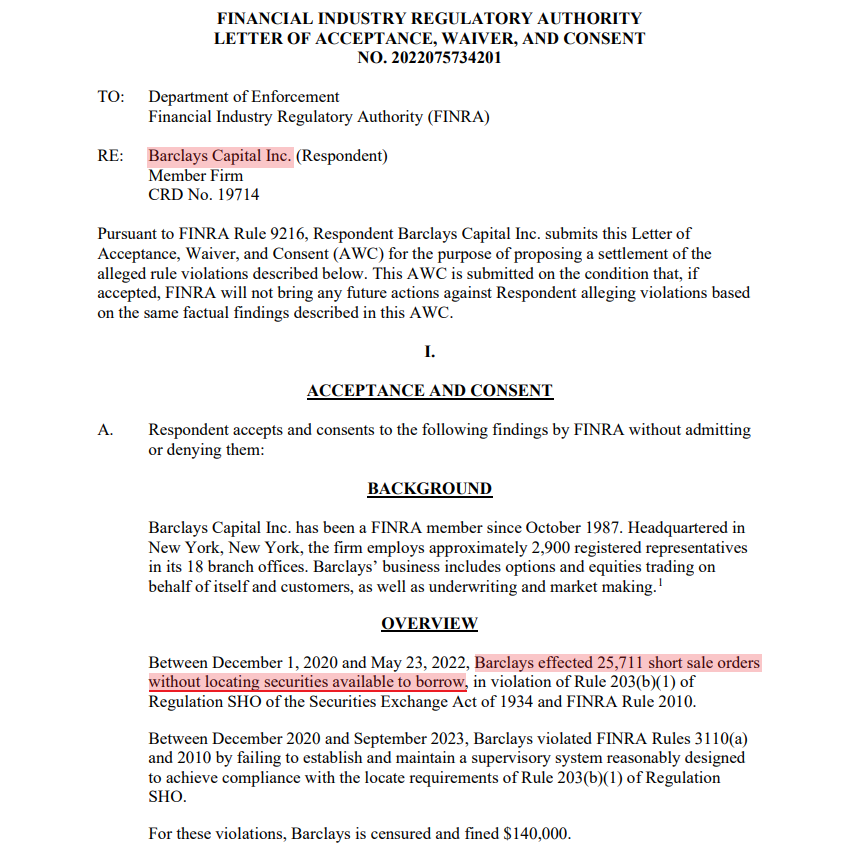

In their recent Letter of Acceptance, Waiver, and Consent (AWC), Barclays admitted to executing 25,711 short sale orders in equity securities between December 2020 and May 2022 without bothering to locate borrowable shares. That's a straight-up violation of Rule 203(b)(1) of Reg SHO... the "locate requirement". This rule is designed to prevent exactly this kind of naked short selling, but here it is happening in broad daylight. On top of that, from December 2020 all the way through September 2023, FINRA failed to maintain any reasonably designed supervisory system to catch this crap. Reused trading accounts with leftover "market maker" coding just let them skate by, and FINRA's response? A measley $140,000 fine plus a censure. No admission of guilt, of course. Just the usual "without admitting or denying the findings."

Now think about that for a second. 25,711 improper short orders over 18+ months. How much cash do you figure Barclays and their clients made off those trades? Do you know how insanely profitable shorting without locates in potentially hard to borrow names can be? These practices depress prices, triggers stops, and creates synthetic supply that never actually existed... all at the SAME TIME! We're talking potential millions (or more) in profits, fees, and spreads for a massive global bank like Barclays, whose overall profits run in the billions annually. All while the investing public is literally stolen from in the process. And FINRA hits them with pocket change fines? $140k is literally nothing to these institutions. It's a fraction of their cost of doing business. Less than a rounding error. And yes, similar Reg SHO cases against big players have seen fines in the $2M–$5M range for thousands of violations, but compared to how much they MADE on this conduct? This isn't enforcement... it's a fking participation trophy for breaking the rules.

As if you needed further proof of how FINRA protects bad actors while making investors a sacrificial lamb, lets tie in the MMTLP situation. Both the issuing company's estate, and the Next Bridge Hydrocarbons spinout company, and all investors involved in BOTH, have been screaming for a full share audit, blue sheets, and real transparency around the December 2022 trading halt and alleged naked short positions. One hedge fund alone (Anson Funds) has allegedly admitted to being short 10 million shares, nearly 4x the reported total of 2.65 million short shares that FINRA has stated on the record. Around a HUNDRED congressional members total have advocated for this data to be turned over, and FINRA balked at every single one of their requests. Yep... instead of handing over the data and letting the facts come out, FINRA has battled investors in court at every turn, resisting subpoenas, claiming it's too "burdensome," and burning through serious legal fees to keep the details hidden.

Now... here's what really pisses me off: The companies whose stocks get caught up in this Barclays mess? They get zero notification. Nothing. Not a single ticker named in the AWC. Just vague talk of "equity securities." So if your company's share price was artificially depressed by this naked shorting, if your hardworking investors got screwed by phantom shares that shouldn't have existed in the most "free and fair markets in the world"... too fkin bad. Go play detective with old threshold lists and short interest data if you want. Spend a fortune on lawyers and forensic analysis just to figure out if you were targeted. FINRA ain't helping, and as the MMTLP situation demonstrates, will likely spend money to fight having to be transparent with you. Meanwhile, when some company has a data breach and your personal info gets stolen, you get a nice letter in the mail informing you of such, which is often followed by a settlement check of some kind. But when Wall Street players flood the market with synthetic shares that can tank your stock and strip you of your hard earned savings? Crickets from FINRA and the SEC. MONEY SPENT BY THE REGULATORS TO CONCEAL THE TRUTH. NO transparency. No help. And no one cares.

This is supposed to be the most transparent market in the world? Gimme a fkin break. FINRA polices brokers with confidential investigations, generic public settlements, and fines so weak that they barely register. There's NOTHING transparent about it. No mandatory share audits. No one gets fired or HEAVEN FORBID criminally charged for what basically equates to printing counterfeit money. Then on the other side of it, no restitution to issuers or investors. No heads-up so companies can evaluate their legal options. Just more regulatory concealment that lets this shit fester and keep right on goin.

So let's call it what it is. The system is built to protect the players, not the public companies or the hardworking investors upon whom our free markets were originally built. It has now become a fking blueprint for how to abuse loopholes, market structure, and "oversight" itself without real consequence. Regulators lead everyone to believe we have rules with teeth. SEC Chairman Paul Atkins is out here touting that the market is more secure and fair then ever. It's not true. Instead, they look the other way while naked shorting goes on, companies get damaged, and the fines are treated like a joke.

This isn’t some isolated screw-up. It’s the pattern. And it erodes trust in the entire market.

Now, circling back to MMTLP, thankfully, just two short days ago, the judge overseeing the Meta Materials bankruptcy proceedings has compelled FINRA to turn over data from their trade reporting facilities related to BOTH MMAT, and MMTLP (the preferred shares which were then exchanged for shares of Next Bridge Hydrocarbons, a company that is still ongoing and not in bankruptcy). Data that when supplied, provides transparency to investors who have been, in some cases, irreparably harmed. All of this comes much to the VISIBLE dismay of FINRA's attorney, who one could swear was going to break down and cry upon hearing the judge's ruling.

This situation with Barclays just further demonstrates the lengths FINRA will go to in an effort to NOT be transparent at all in their role as a "market regulator". Investors and/or a company DESERVE TO KNOW if their company was the target of naked shorting. But instead of simply releasing the data, FINRA will go to any lengths to protect and insulate these bad actors from potential claims for their THEFT. And make no mistake about it, it's theft PLAIN AND SIMPLE. When you then see how FINRA has fought every single solitary court proceeding calling on them to provide the very transparency that they are allegedly mandated to provide, you start to see the picture real clear: FINRA will spend hundreds of thousands if not millions of dollars to be opaque, rather then spend a fraction of that to provide transparency. Gee... I wonder why. The pattern is clear, and it stinks.

But as it relates to the MMTLP shareholders fighting for justice, the round room that FINRA was scurrying to find a corner to hide in just shrunk on them. I told you many times: We aren't going anywhere until this is resolved, and I hope every last one of your collective asses ends up on the chopping block when the data comes out.

And to the experts, journalists, and their tribe of trolls without any semblance of a life outside of social media, all of whom who still claim naked shorting does not exist: I very kindly ask you to read the below, and then very promptly go f (restraining myself)... get a life.

Thank you.

@Harvard1988@KarmaCollects @Thebestfigen @LeaKThompson Are you on crack? That’s George McFly and Lorraine Baines from the night they went to the “Enchantment Under The Sea Dance”. Jennifer was Marty’s girlfriend, played by Claudia Wells in number 1, and Elizabeth Shue in 2 and 3.

@Diamondhanninja@KarmaCollects You are too. You’re very good at turning perfectly good oxygen into C02, and replying and blocking like a goon. Who are you anyway? You don’t speak in spaces, did nothing with Congress… seemingly have contributed zero. If you’re a shareholder, a leech is what you are.

@OpiolaKenneth @KarmaCollects@_einfachman_@sing16888 That’s what I thought. You wouldn’t even bet a thousand bucks if it was for real. Good riddance, Krusty.

@tweeterola@KarmaCollects@CassandraRules If I’m wrong, cite something to make a point. You can’t. We went in, blew up nuclear facilities that have been a concern for decades, then left. It’s not a war.

IDGARA about your assessment of my opinions. I lay them out, and you just say “you’re so wrong”, and block. GTFOH.

NEW ACCOUNT NOTICE:

For anyone that may have been following me here, please follow my new account @KarmaCollects. Twitter suspended this one, and now unsuspended me (after 4 months of appeals), but I will continue to use the other account moving forward. Please follow it!

Hey @DOGE_SEC, if you want to investigate abuse at the @SECgov… $MMTLP would be a great place to start.

These people have been fighting for two year.

Transparency withheld is justice denied!

We have a huge opportunity to not only make market oversight efficient, but fair. Luckily, we have the right guys heading up @DOGE in @elonmusk & @VivekGRamaswamy. Here are my thoughts on why.

@teresagoody@DonaldJTrumpJr

$DJT $TSLA $MMTLP $AMC $GME

https://t.co/RZPMnICQIh

My name is Andrew. In January 2022, I made an investment that has since become a wild, eye opening lesson in the corruption that runs rampant on Wall St. A lesson that cost many good people EVERYTHING, including their families, homes, and sadly, their lives. This is our story 🧵.

$MMTLP So I want to leave this here as a stand-alone informational video to any of you who would like to use it to explain our story in 3 minutes to someone. Take it. Use it. Send it out. I made the video, but all of us contributed, so it belongs to all of us. Keep fighting.

After going through and comparing @FINRA's recent response to @RepRalphNorman's inquiry into $MMTLP, it's unmistakably clear that several crucial questions have been addressed with insufficient clarity, or left out entirely. While I'm sure that @bleedblue18 and the crew will tear apart the VERACITY of the claims that FINRA is making, here's a breakdown of these key issues FINRA failed to adequately address and/or blatantly left out of their letter:

1) Provide a timeline of trading of MMTLP on the OTC markets; the actions taken by the SEC, self-regulatory organizations, the issuers, the transfer agent, and any other relevant parties during the time MMTLP was traded, and the transaction that produced NBH shares.

- The absence of a comprehensive timeline detailing the trading of MMTLP, actions by relevant parties, and the transaction leading to NBH shares is concerning. Such a timeline is essential for transparency, providing investors with a clear understanding of the sequence of events surrounding MMTLP's trading and the actions taken by regulatory bodies and market participants. Without this information, it is challenging to assess whether appropriate regulatory measures were taken to address any irregularities and ensure market integrity during MMTLP's trading period. Additionally, insight into the transaction producing NBH shares is crucial for understanding the distribution of shares and its impact on shareholders' interests. Overall, the lack of a detailed timeline deprives investors of critical information needed to assess the fairness and transparency of the trading process, regulatory oversight, and corporate actions related to MMTLP.

2) The Former CEO of Torchlight Energy Resources stated that “MMTLP was never designed to trade.” Please provide a detailed explanation, including the relevant statutory authority and procedures, that allowed for MMTLP shares to trade on the OTC market.

- FINRA's response lacks clarity on the statutory authority or procedures enabling MMTLP shares to trade on the OTC market, especially given the above statement made by John Brda, the former CEO of Torchlight Energy Resources. Understanding the legal framework and regulatory mechanisms governing MMTLP's trading is crucial for all market investors to gauge the legitimacy and regulatory compliance of such activities. FINRA stated that "It does not appear that Meta Materials took effective steps to restrict public trading in MMTLP". They don't say they didn't take ANY steps, they only say that Meta Materials was not EFFECTIVE in the steps they took to restrict public trading. What FINRA does not specify, is what steps they would deem to have been effective. The investing public has already been told that both John Brda and Meta Materials reached out to FINRA to request that the trading be stopped, and both were told that FINRA's decision to allow the security to trade under the MMTLP symbol was FINAL. Without a clear explanation from FINRA, concerns and outcry will persist regarding the regulatory oversight and adherence to established procedures in permitting MMTLP shares to trade, particularly if the former CEO's assertion implies irregularities in the trading process. After 14 months of opacity, investors deserve transparency and assurance regarding the legal basis for MMTLP's trading status on the OTC market to make informed decisions about their investments.

3) Provide the relevant statutory authority, jurisdiction, and adherence to established industry standards regarding the U3 trading halt of MMTLP issued on December 9, 2022.

- While FINRA provided some information, there are still gaps in understanding the statutory authority, jurisdiction, and adherence to industry standards regarding the halt. They have continuously referred to "uncertainty in the settlement and clearing process", however they neglect to mention that EVERY SINGLE MAJOR U.S. BROKER DEALER informed their clients that trades on 12/9 and 12/12 would be STRICTLY limited to closing orders ONLY. That means, NO BUYING. Understanding the legal basis and regulatory protocols governing such trading halts is vital for ensuring market integrity and investor protection. Without a clear explanation from FINRA that considers all of the above, concerns remain regarding the justification and regulatory compliance of the U3 trading halt, potentially leaving investors without the necessary confidence in the regulatory framework surrounding MMTLP trading activities.

4) Provide the exact date and circumstances surrounding FINRA’s determination to implement the U3 halt, including all unredacted communications between FINRA, SEC, governmental agencies, any outside organizations, FINRA members and non-FINRA members, and any other individuals. Also include all information surrounding the SEC or FINRA’s knowledge of the share price in any public or non-public exchange before issuance of the U3 halt.

- While FINRA did touch upon the U3 trading halt in their response, the details provided were insufficient to fully understand the sequence of events leading to the halt. They did not offer specific dates, circumstances, or communications leading to the halt, nor did they provide information about the SEC or FINRA's awareness of share prices before the halt. In fact, not a SINGLE communication was offered. As a result, there remains a significant gap in understanding the decision-making process behind the trading halt and the regulatory oversight exercised by both the SEC and FINRA.

5) Provide the first date and time that FINRA or its agents advised any market participant in any manner that MMTLP would no longer trade on December 9, 2022. Include any relevant documents or communication.

- FINRA's response lacks clarity regarding the specifics of when they first informed market participants about MMTLP's cessation of trading on December 9, 2022, and whether they provided relevant documents or communication to support this. While they mentioned their role in implementing the trading halt, they did not offer precise details about the initial communication with market participants, leaving uncertainty about the transparency and timeliness of their notifications regarding the halt. Considering that in the days prior to the halt, broker dealers, members of the investing public, and even the VP of the OTC Markets, Jeff Mendl, were all led to believe by FINRA that we would have until December 12th to close our positions, this is especially concerning.

6) Did FINRA issue a Blue Sheet request for MMTLP during the period of October 2021 through December 2022? Why or why not?

- FINRA's response lacks clarity on whether they issued a Blue Sheet request for MMTLP during the specified period, despite the knowledge we learned via FOIA that they did request such data on December 5, 2022. Additionally, there is no explanation provided for why they pursued this avenue of inquiry, or what they learned FROM the blue sheets, leaving even further gaps in understanding regarding their investigative actions related to MMTLP trading. This information is crucial for transparency and accountability, as the issuance of a Blue Sheet request could shed light on the trading activity surrounding MMTLP and potentially uncover any irregularities or manipulative practices. Understanding why FINRA did not provide this information is essential for evaluating the thoroughness of their response and ensuring that all necessary steps were taken to investigate the trading activity in question.

7) How many questions, complaints, and/or inquiries have you received regarding MMTLP?

- FINRA's response does not include a specific count or detailed information regarding the number of questions, complaints, and inquiries they received regarding MMTLP. Meanwhile, we KNOW that they track this information for their annual reports. Understanding the volume and nature of questions, complaints, and inquiries related to MMTLP is vital for assessing the extent of investor concern and market disruption caused by the trading activity surrounding this security. Without a clear account of the number and substance of these communications, it's challenging to gauge the severity of the situation and the adequacy of FINRA's response. This information is essential for ensuring that regulatory bodies are adequately addressing investor grievances and taking appropriate action to safeguard market integrity.

8) Provide the statutory or legal justification used by the SEC and FINRA to ignore public requests and congressional inquiries regarding MMTLP.

- While they provided some information, there are still gaps in understanding the statutory authority, jurisdiction, and adherence to industry standards regarding the halt. There's no clear explanation provided by FINRA regarding the statutory or legal justification for the SEC and FINRA's handling of public requests and congressional inquiries concerning MMTLP. Understanding the statutory or legal justifications behind the handling of public requests and congressional inquiries concerning MMTLP is crucial for ensuring transparency and accountability in regulatory processes. Without clear explanations from FINRA, there may be concerns about the regulatory bodies' adherence to legal mandates, their responsiveness to public and congressional inquiries, and the fairness and consistency of their actions. Clarity on this matter is essential for upholding the principles of regulatory oversight and maintaining public trust in the regulatory framework.

9) Provide the delivery of a certified audited and consolidated count of shares that were held by all U.S. and foreign financial institutions, together with their clearing firm counterparties including trades not reported in the consolidated audit trail (CAT), related to MMTLP on the date of December 12, 2022...

- Believe me, we're not surprised that this was avoided. That withstanding, it is important to note that the absence of a detailed and certified audited count of MMTLP shares held by financial institutions and counterparties raises concerns about the accuracy and transparency of the information provided by FINRA. Clarity and transparency in this regard are essential for ensuring market integrity and investor confidence, as well as for facilitating informed decision-making by all stakeholders involved. How can there be any confidence in the market if our regulators can not keep track of how many shares of a security are in circulation? When you are an SRO with absolute immunity that is tasked with providing transparency to the investing public, responding a request for the most quintessential form of transparency there is (a simple share count) by saying "we can't do that", is absolutely unacceptable. Full stop.

10) Have all MMTLP shareholders received their NBH shares?

- What is perplexing is even though we already know the answer (NO), there's no explicit confirmation or denial provided by FINRA regarding whether all MMTLP shareholders received their NBH shares. The lack of explicit confirmation regarding the distribution of NBH shares to all MMTLP shareholders raises concerns about the completeness and accuracy of the corporate action process. Without clear assurance that all shareholders received their entitled NBH shares, there remains uncertainty and potential discrepancies in the distribution process. This ambiguity could undermine investor trust and confidence in the fairness and transparency of the market, highlighting the need for thorough and transparent communication regarding corporate actions and share distributions.

11) Do you have evidence to suggest the existence of fraud and manipulation related to MMTLP transactions, such as illegal forms of naked shorts and counterfeit shares, that could distort the market?

- FINRA keeps saying that they have "found no evidence that there was significant naked short selling in MMTLP involving FINRA member firms at the end of its trading ". However, they do not expound upon what they deem as "significant". What does that mean? You found some? How much, exactly if you don't mind? While recent public relations from NBH have discussed attempts by short sellers to acquire more shares than reported currently short by FINRA, the lack of direct acknowledgment or evidence provided by FINRA regarding fraudulent activities surrounding MMTLP transactions raises concerns. The absence of clear confirmation or rebuttal regarding the existence of illegal naked shorts and counterfeit shares undermines investor confidence in the integrity of the market. Investors rely on regulatory bodies like FINRA to actively monitor and address instances of fraud and manipulation to ensure a fair and transparent trading environment. Therefore, the failure to provide conclusive information regarding these allegations leaves lingering doubts and underscores the need for thorough investigation and accountability measures to uphold market integrity.

12) Have you seen any indications of insider trading and/or pump and dump related to MMTLP transactions?

- We know who submitted this question to Rep. Normans office, and we know why. What is curious to me is there's no explicit acknowledgment or denial by FINRA regarding indications of insider trading and/or pump and dump related to MMTLP transactions. FINRA's response to inquiries about potential insider trading and pump-and-dump schemes related to MMTLP transactions lacks any clarity, presumably to continue allow the perceived uncertainty related to this matter to linger. The absence of a clear acknowledgment or denial regarding these concerns leaves room for speculation and raises doubts about the effectiveness of regulatory oversight. It's crucial for FINRA to provide unequivocal statements regarding the presence or absence of insider trading and pump-and-dump activities to reassure investors and uphold the integrity of the market. While certain members of social media did TALK about this security through various mediums, we know there was NO concerted campaign to pump this security amongst insiders, and we know that none of them sold an amount of their position off that would justify the use of the word "dumped". Just come out and tell the public so that they can finally know it too.

13) Are your organizations willing to work with NBH to determine a resolution for existing shareholders? For example, some investors have expressed concern that, even though their brokerage account statements include shares of NBH in their account, these shares may not have actually been delivered to their broker-dealers.

- This particular response is especially concerning. FINRA's response lacks a definitive statement regarding their willingness to collaborate with NBH to address investor concerns regarding the delivery of NBH shares. Investors who hold shares in NBH expect regulatory bodies to actively engage with issuers to ensure the fair and timely distribution of shares. The absence of a clear commitment from regulators to work with NBH (after 14 months of this issue persisting, mind you) to resolve these issues is absolutely egregious at this point, and raises questions about their dedication to investor protection and market integrity. It's imperative for FINRA to demonstrate a proactive approach to addressing investor concerns and facilitating communication between stakeholders to uphold transparency and trust in the market.

14) Identify any regulatory or legislative gaps that should be addressed to ensure the SEC, FINRA, and other regulated entities may better protect investors and strengthen market integrity.

- FINRA's response fails to pinpoint regulatory or legislative gaps that could be addressed to enhance investor protection and strengthen market integrity, despite the specific inquiry. Identifying these gaps is crucial for regulatory bodies like FINRA to effectively fulfill their mission of safeguarding investors and maintaining fair and orderly markets. By highlighting areas where current regulations may fall short, FINRA could contribute to the development of targeted reforms that better address emerging challenges and risks in the market. The absence of such insights raises concerns about FINRA's ability to adapt to evolving market dynamics and adequately protect investors in the face of changing threats and vulnerabilities. Are we to believe that you did absolutely nothing wrong here? We're sorry but the extensive record clearly demonstrates otherwise.

Overall, the tone and content of FINRA's response leave much to be desired in terms of addressing investor concerns and ensuring market integrity. While the response provides some information, it falls short in addressing key questions and providing sufficient clarity on critical issues surrounding MMTLP. Investors and stakeholders expect regulatory bodies like FINRA to be transparent, responsive, and proactive in addressing concerns related to market activities. However, the lack of comprehensive answers and detailed explanations in FINRA's response may further erode investor confidence and raise doubts about the effectiveness of regulatory oversight. As such, there remains a significant gap between the expectations of investors and the actual responsiveness of regulatory authorities, highlighting the need for greater transparency and accountability in regulatory practices. Bottom line: FINRA had the opportunity to methodically address each point raised in the letter, one by one. However, they chose to compile 16 pages of mostly insufficient responses, seemingly in an effort to sidestep or outright disregard the true essence of the inquiry.

I've said this once, and I will say it again: @SECGov and FINRA: Get on the phone with Greg McCabe and resolve this issue. Because we are NOT GOING ANYWHERE... until this is resolved.

🚨 Your financial freedom is at risk! The $MMTLP situation exposes how bad actors on Wall Street are jeopardizing your wealth. If you have any accounts tied to the US Stock Market, you NEED to know about this. 📉💔 Watch my interview with @KarmaCollects as we dive into the details on the fight to protect your investments:

https://t.co/Td6Fe3CO78

$MMTLP The new approach I’m taking with Congress is unstoppable. From getting the zoom meeting to making the ask therein, this method has so far been very effective. If you want to shove your foot down FINRA’s throat, please DM me. See for yourself.

:cracks knuckles: Alright, let’s do this:

Dr. Trimbath, I’m actually glad I didn’t make your head explode. Your reaction (seeming unsurprised by anything that’s unfolded in this situation) only makes me more confident that we are in the right. To me, that’s a good thing. Someone with 24 years of experience and your breadth of knowledge being unsurprised only confirms at the highest level what I already knew: that for the last two years, we haven’t been fighting for some pipe dream. Respectfully, I understand that after 24 years of waging this battle against the massive issues in our markets, your focus is on the broader problem. But for some of us, life hangs in the balance of the outcome of this specific situation.

So, for me, the focus will remain on getting some kind of share audit for MMTLP holders or a reconciliation that fixes the problem for us individually, which will allow people like you, who are fighting for something SO important, to use that to demonstrate the need for overhauls to fix the broader problem. I genuinely appreciate the space you gave us, and if I feel your time wouldn’t be wasted, I’ll reach out privately. At the very least, I’m grateful for the conversation we had and am even more convinced that our fight is unique given the nature of our non-tradable status, leaving us, and the data, frozen in time.

I can’t speak to how your comment about not having your head explode is intended, but I genuinely appreciate your perspective. Either way, I’d rather you be unsurprised than shocked to the point of disbelief. So thank you, Dr. Trimbath, for engaging with us. Your perspective only strengthened my resolve.

And here’s a spoiler alert for you all: We’re gonna win.