The major indices pulled back on Friday, with the NYSE registering a distribution day. Distribution now stands at four for the NYSE versus just one for the Nasdaq Composite, not at ominous levels. Even so, the market is beginning to show signs of coming under pressure.

Going forward, we want to see current holdings tighten up and consolidate constructively without violating key support or triggering stops, while the major indexes avoid stacking additional distribution days.

At this stage, we recommend harvesting profits in extended names or, at a minimum, back stopping stops to protect gains in stocks that have become stretched from proper buy points. At the same time, attention should stay focused on high-quality setups—particularly leaders building the right side of new bases or emerging through sound pivot areas. A pullback will likely manifest itself rotationally as opposed to taking all stocks down like a bear market.

Exposure should be reduced in lagging stocks and any positions that trigger predetermined stop levels.

Sector performance on Friday was broadly negative, with Energy (+0.9%) the lone area to finish higher. Basic Materials (-4.3%) led the downside, followed by Consumer Cyclical (-2.8%) and Utilities (-2.3%).

Looking at the past four weeks, Technology was the strongest-performing group (+10.0%), followed by Energy (+7.7%). Meanwhile, Basic Materials (-6.2%), Utilities (-4.8%), and Health Care (-3.4%) were the weakest areas.

Hot CPI and PPI readings, combined with the 10-year Treasury yield emerging from a prolonged base, have put inflation and interest rates squarely back in focus. Rising yields are becoming an increasingly important variable for equities, particularly as they impact valuation-sensitive growth areas of the market.

Oil is another key area we are monitoring closely. A decisive breakout to new highs in crude would likely add further inflationary pressure and create an additional headwind for stocks.

At the moment, the recent uptick in inflation has effectively tied the Fed’s hands. Expectations for near-term rate cuts continue to fade as policymakers remain focused on preventing inflation from becoming entrenched again. As a result, any incoming economic data that reinforces the higher-for-longer narrative on inflation and rates will likely weigh on the market and increase volatility. https://t.co/JXzFFTmMtn

US10Y chart of the day Friday, hit IWM MDY hardest, as a result breadth narrowed. XLE XOP rose as WTI rose back to 100, watch for WTI break over 106 would pressure stocks further. HYG, a risk-on barometer, gapped down, closed Friday at up gap support.

Rotation into IGV as MSFT notably strong on Friday amongst mega caps. CRWD PANW continued their vertical move up. Keep eye on YOU. CSCO ONDS VIAV GEV PWR BE RKLB GOOGL DDOG BAND YOU FTNT DOCN STRL holding their earnings gaps.

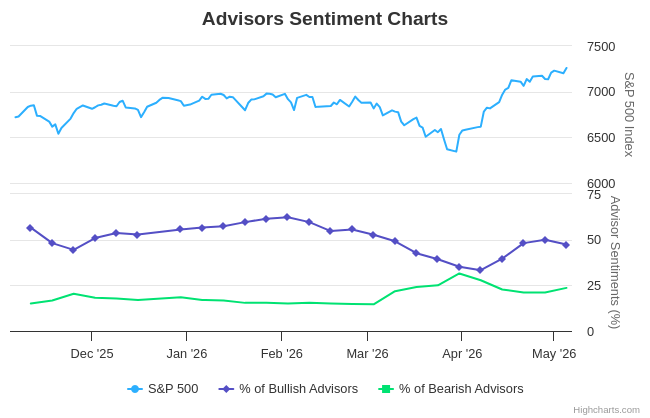

Stocks are pushing to all-time highs while sentiment is getting more bearish—bulls down, bears up. That’s a sign of disbelief. Investors are fighting the rally, which is a classic Lockout Rally condition. https://t.co/7NiHKuPACd

Price action has bullish feel. Possible that market has already priced in war and oil headline chaos and maybe ignoring that going forward. Leaders leading SMH, optical, etc.

SPX weekly with V-shaped recovery look due to big ceasefire gap up day, but closed at/near 10-/20-week SMA. Look for retest at/into gap area. IMHO, feels like bottom is in, but volatility is still elevated though subsiding.

SPY futures weekly held inverted hammer with close above body 2 weeks ago. Daily morning star candle pattern, after daily higher low buy area in small consolidation just before ceasefire headline. Was a good time to add to index ETFs investments.

Today’s market strength was textbook. This is exactly what markets do during corrections when they get stretched to oversold levels. As I said just recently, "some of the biggest rallies occur during bear markets and corrections." Today was a perfect example.

Traders rushed in after headlines hit that Iran’s president signaled a willingness to end the conflict with the U.S. The Dow exploded higher by 1,125 points. But let’s not confuse cause and effect. The news may have been the trigger, but the market was already set up for a rally. It was oversold and primed. Now comes the part where discipline matters.

We ignore the first few days of a rally attempt. That’s potential noise. What matters is whether the market can follow through and whether leadership begins to emerge and proper setups develop.

Technically, this is a classic snapback: Indexes that broke below the 200-day are rallying back toward it, while Indexes that held the 200-day are bouncing off it. That’s typical countertrend behavior until proven otherwise.

Expect volatility to remain elevated. That’s not where low-risk money is made, but it's certainly where the risk is. Your job during corrections is simple: identify the stocks showing the best relative strength and the tightest price action. Those are your future leaders when the market finally turns.

On the macro side, nothing has been resolved. Higher crude prices are still a problem. Yesterday’s rally did nothing to materially bring down oil. The bigger issue is still in play and the jury still out. Oil at these levels feeds inflation, pressures growth, and gives the Fed a reason to stay on hold longer. Yields stay elevated in that environment.

To cut through all the noise, I look to the market itself, which has a much better track record of telling us the truth than the politicians, the analysts, the news, and the gurus.

The four steps of the bottoming process are:

1. Oversold – The difference between an ordinary pullback and an oversold condition starts with price, but it does not end there. Poor breadth and and a lack of volume confirmed follow through describe a one-sided market, and one not to trust.

2. Rally – Inevitably, the market bounces from its oversold condition. A high-quality rally is broad-based. A low-quality rally is defined by short covering and driven primarily by the stocks that have declined the most. Again, the character of the rally is important to distinguish. So far, we simply don't have enough data to make a confident determination, so patience is the watch word while we wait.

3. Retest – After the rally, there is almost always a retest. The popular averages approach, and in some cases breach, their oversold lows. The key to a successful retest is less selling pressure, such as fewer stocks below their moving averages, fewer stocks, sectors, and markets making new lows, less total volume, and less downside volume. If the retest fails, the process reverts and we generally start looking for divergences during lower lows. In the event of unexpected news, it is possible for the market to recover in a "V" fashion with no retest. In that case, we look at breadth confirmation and participation.

4. Breadth thrusts – In the final phase, not only do benchmark indices rally sharply with few pullbacks, but they do so with an extremely high percentage of stocks, sectors, and markets participating, or what technical analysts call breadth thrusts. In rare cases, the market has skipped step 3. With strong enough breadth, retests are not necessary. The Covid bottom is an example of a pretty powerful V-shaped recovery.

Bottom line:

This was an oversold rally, sparked by headlines—but not defined by them, and certainly not confirmation of a reliable bottom.

Now we watch:

--Quality of follow-through

--Emergence of leadership

--Market internals and model health

If the rally lacks quality, if economic pressure builds, or if leading stocks begin to deteriorate, then this remains what it likely is—a rally within a correction.

Stay objective. Let the market prove itself. If you are going to trade, do so incrementally.

https://t.co/JXzFFTmMtn

Back to the market. Oil is surging, volatility is expanding, and sentiment is quickly turning bearish—that’s your first clue. When fear spreads wildly, you have to start thinking contrary. But let’s be clear: Powell has signaled he’s on hold until there’s clarity out of the Middle East. That means uncertainty remains the dominant force—for now.

After last week’s meeting, Fed Chair Jerome Powell emphasized that further evidence of easing inflation is required before additional policy easing is considered: “If we don’t see that progress, then you won’t see the rate cut.”

Market expectations have shifted. In just a week, bond traders moved from anticipating rate cuts to pricing in roughly a 50.0 percent probability of a rate hike by October. In Europe, markets are now pricing in as many as three ECB rate hikes by year-end.

Recession risk is rising as the Iran conflict prolongs and oil prices are elevated. A slowing U.S. economy could hurt corporate profits and also exacerbate emerging stresses in the private credit market.

At some point, we’re going to get a sharp snapback rally. That’s inevitable. But don’t confuse a reflex rally with a new uptrend. Some of the most powerful rallies happen inside bear markets and major corrections—they trap the impatient and reward them with whipsaw action.

The market is news driven. If this conflict resolves quickly and favorably, we could see a classic V-shaped recovery. If not, the market is going to likely need time to repair to establish a durable bottom.

Oil will eventually present a good shorting opportunity. Equities will bottom. But timing is everything—and for the low-risk trader, volatility is the enemy.

That's why I’m never concerned with buying at the lowest price—I want the right price. I want alpha, and I want it fast and efficient.

Grinding for pennies in chaotic conditions is for gamblers and action jumkies. Those are hard-penny environments—and that’s where amateurs get chopped up.

Professionals have what I call sit-out power—the discipline to wait for easy-dollar conditions, when the odds are clearly in your favor. How long do they wait? As long as it takes. That's where the discipline comes in.

https://t.co/JXzFFTmMtn

The market's character is still one of a bear market or cyclical correction; strong open, fade into close and major average living below the 200-day line. Before a reliable bottom can be established, we need to see better price and volume action, including better action from breakout names forming bases.

We are clearly NOT out of the woods yet. The market backdrop is one where sentiment has improved with rising pessimism, but not a full capitulation. The VIX has reached bear warning levels, but remains below true washout extremes. A volatility washout is not required for a bottom, but would add conviction.

Bullish Scenario

--The war ends

--Oil prices recede

--Stagflation concerns ease

--Central banks continuing their easing trajectory

Under this scenario, we would expect:

-A broadening market advance

-Emergence of new leadership from sound bases

-A Follow-Through Day (FTD) on the NYSE and/or NASDAQ confirming institutional buying with little in the way of immediate distribution

-Significant drop in volatility

Bearish Scenario

--The war persists or escalates

--The Strait of Hormuz remains disrupted

--Oil prices make new highs

--Stagflation becomes evident in hard economic data

This would likely result in:

-Limited general market rally attempts with most breakout stocks failing

-Lack of follow-through from breakout names

-Further deterioration in breadth and leadership

-Dearth of setups in buyable position

-Continued elevated volatility and distribution

In that case, sentiment would likely need to reach higher levels of pessimism before a durable market bottom could form. In its absence, and end to the factors that are pressuring the market could cause the market to bottom in less dramatic fashion.

The market has been discounting higher oil prices and geopolitical uncertainty. Sentiment is finally turning more bearish, which from a contrary standpoint is a step in the right direction. However, in the short term, volatility is likely to remain elevated as bullish sentiment unwinds and bearish sentiment approaches an extreme.

As noted, this is likely a cyclical correction within a broader secular bull market. Patience and vigilance will be key to identifying the next leaders in the coming advance.

Oil will ultimately present a compelling opportunity on the short side, and equities will eventually find a bottom. That said, I don’t play guessing games or try to catch falling knives. One of the most difficult lessons for traders to internalize is that the right price is not necessarily the lowest price.

In the near term, remain defensive. Keep exposure tight and highly selective. Focus only on the highest-quality setups and demand confirmation with meaningful follow-through before committing additional capital or increasing exposure to aggressive levels. The market is offering very little margin for error—discipline and patience are essential.

https://t.co/JXzFFTnkiV

WTI, chart of recent weeks, weekly spinning top with very long wicks, a bit of indecision, uncertainty from war, geopolitical headline risk, after breakout from multi-year DTL. XLE strength as a result. XLF weakness continue to be concern.

Can SPY hold weekly inverted hammer, support gap, 650 level support and make a potential rounding top reversal? Up to war/geopolitical headlines. Mostly in observation mode.

There are still a good number of stocks forming bases following strong prior uptrends, and so far market pressure has not caused widespread technical damage. However, after running my stock screens, the dominant theme is right-side volatility — which often starts as pivot “leakage.” An increasing number of patterns have become volatile. For truly low-risk buy points to emerge, that volatility needs to subside. Patience is key. Let the setups come to you.

From a macro perspective, the backdrop remains supportive of a continued bull market, with the long-term trend still intact. The conditions typically associated with a secular bear market are not currently present. Corrections should be viewed as cyclical opportunities within an ongoing secular bull.

That said, the current environment is challenging for directional breakout trading. Our own STEM risk model has suggested maximum caution (RED) since Feb.4.

However, waiting for the war to end may not be the best course for timing individual stock trades. The market is a discounting mechanism. A bottom could occur before geopolitical clarity emerges. The best stocks tend to set up, emerge and lead the general market.

https://t.co/JXzFFTmMtn

https://t.co/FfBnR93ojq

https://t.co/TFyCpPHZis

After beaten down, lagging, MAGS (long) weekly piercing candle, undercut & rally? Can it follow-thru? Chop continues, but leaders still leading LITE CIEN COHR GLW MU SNDK WDC STX AMAT LRCX KLAC GEV VRT PWR BE. XLF lagging, concerning. See if can bounce back thru 200MA or rejects.

@markminervini Looks like 76.4 fib low in both 1980 and 2011. However, time to base is shorter, 31 vs. 16 years. 37 is buying time for the next run. It's insurance. Buy physical, trade paper.