$META Q1 2026

"We're on track to deliver personal superintelligence to billions of people." - Mark Zuckerberg

DAP +4%

Ad impressions +19%

Avg. price per ad +12%

Revenue +33%

EBIT +30%

*marg. 41% (41)

EPS +62%

$AMZN Q1 2026

"We're in the middle of some of the biggest inflections of our lifetime, we're well positioned to lead, and I'm very optimistic about what's ahead for our customers and Amazon." - Andy Jassy

Revenue +17%

*AWS +28%

*Online Stores +12%

*Physical Stores +5%

*Third Party Sellers +14%

*Subscriptions +15%

*Advertising +24%

EBIT +30%

*margin 13.1% (11.8)

EPS +75%

FCF LTM -95%

$GOOGL Q1 2026

"2026 is off to a terrific start. Our AI investments and full stack approach are lighting up every part of the business." - Sundar Pichai, CEO

Revenue +22%

*Google Search & Other +19%

*YouTube Ads +11%

*Google Network -4%

*Google Cloud +63%

EBIT +30%

*marg 36% (34)

EPS +82%

$UNH

Based on my estimates, if you buy UnitedHealth stock at 530$ in next 10Y you'll get:

🔴 1.5%/year (worst s.)

🟡 8.8%/year (average scenario)

🟢 15.5%/year (best s.)

My rating: HOLD ☑️

Price target 1Y: 560$

$CVS $CNC $ELV $HUM $CI $WMT $JPM $BAC $C $WFC $BLK $PFE $JNJ $LLY

Chuck Akre in his old letters talked about looking for "coiled springs" - opportunities where the company's real economic value was growing faster than the stock price.

Getting the fundamental growth + stock re-rating higher gets you the Davis Double Play.

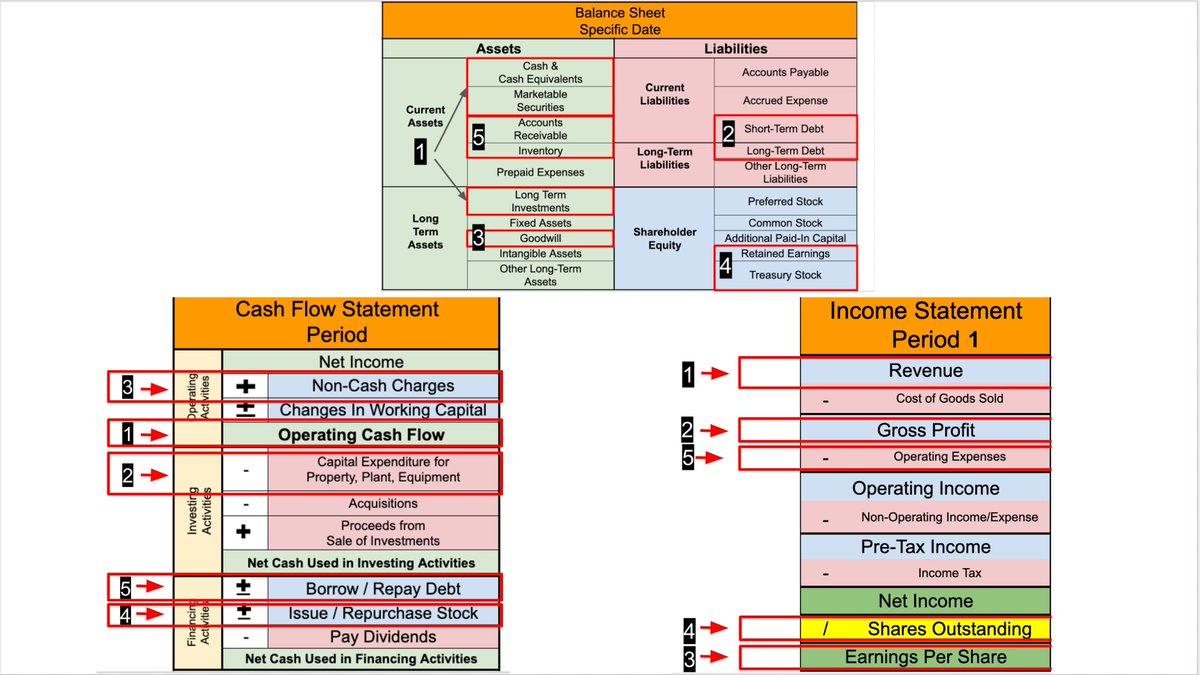

I have an MBA and used to work as a Professional Investor.

I’ll teach you the basics of a

- Balance Sheet

- Income Statement

- Cash Flow Statement

In a few minutes.

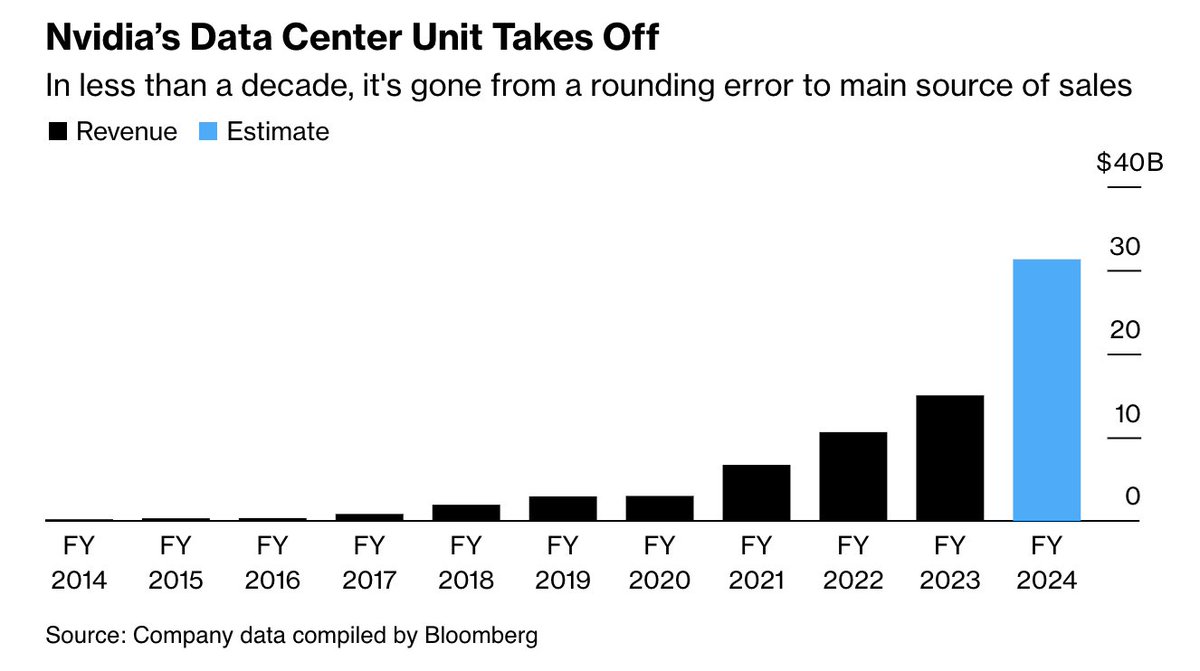

Good $NVDA morning:

"Data Center compute revenue nearly tripled year-on-year, driven primarily by accelerating demand from cloud service providers and large consumer Internet companies for our HGX platform, the engine of generative AI and large language models" - $NVDA CFO

Will Adyen be able to re-accelerate growth back to its medium-term guidance of mid-20s and low-30s net revenue growth and bring EBITDA back to its long-term guidance of 65%?

Yes, I think it will, and here's why.

Let's dive right in.

1. Investment phase similar to 2020

While the market is selling off as a result of Adyen investing to scale its team in a difficult environment, it was not so long ago that Adyen was in a similar position.

In 2020, Adyen was in its investment phase when the market environment was difficult due to the COVID-19 pandemic.

There are lots going on in the table below, but look at 2020:

Growth decelerated rapidly from 2019 levels as a result of the pandemic, from 43% in 2019 to 28% in 2020.

Investments to scale the team continued in this difficult environment as management continued to build for the long-term. This caused EBITDA margin to fall from 60% to 54%.

In addition, when we look at the wages and salaries over the processed volume, it is at a similar level in 1H20 and in 1H23 at 5.8 basis points, indicating that Adyen was clearly in its investment phase similar to today.

Subsequently, we all know that revenue reaccelerated to the mid 40% range and this lead to EBITDA margin reaching 64% in 1H21, close to its long-term EBITDA target of 65%.

While the market conditions and competitive environment is different, I think this highlights management's ability to control EBITDA margin and the clear relationship between how investments to scale the team leads to accelerated net revenue growth.

2. Operating leverage improvement and revenue acceleration in 2024

Similar to what happened in 2020, 2023 is Adyen's investment phase.

This was actually already communicated earlier when management guided in advance for its investments in the team in 2023 to be at a similar pace to 2022.

However, Adyen expects to slow hiring in 2024 and transition out of its investment phase.

There are 2 things that will happen:

Firstly, with the pace of hiring slowing down in 2024, I expect EBITDA margin to bounce back. Operating leverage will improve as the business grows faster than the team does.

Secondly, given that Adyen is investing to scale its teams today, and again, here there are two aspects.

The first one is that Adyen is boosting its tech team, which made up 75% of its new hires in 1H23. This will bring new functionality to Adyen, improve the delta between Adyen and competitors and lead to more differentiation and in turn, market share gains.

The second one is that Adyen has been adding to the commercial team, especially in the US, which I expect will provide tailwind to the net revenue numbers starting 2024 as the team is at the right scale.

3. Growth is not always linear

Growth will never be linear.

I think the market's worry about Adyen's 21% net revenue growth in 1H23 falling short of medium-term guidance is overdone.

As can be seen in the table below, from 1H21 to 1H22, Adyen grew net revenue way faster than its medium-term guidance of mid-20s and low-30s net revenue growth.

There are clearly challenges that Adyen face today that led to this lower growth in 1H23, and I will address this next, but the message here is that growth will have periods where it will overshoot or undershoot.

If growth is indeed linear, all business leaders would have a much easier job today.

4. Nothing has changed

The US market has always been competitive and prone to price competition. This is because it has a huge domestic market, there is less complexity etc.

Price competition has always been around in the US, but the only difference in 1H23 was that it was more intensive than in prior years. This is likely due to the more difficult macro backdrop which is resulting to customers optimizing for profits.

However, Adyen's strategy has been consistent and to me, the one that is the most sustainable.

By not competing on price, this allows Adyen to have a greater ability to invest in the team and its products. In turn, this leads to Adyen providing differentiated functionality.

As a result, in 1H23 and in prior years, Adyen's strategy is to differentiate itself from the competition and not go the route of providing the commoditized payments that competitors are doing.

In short, Adyen is playing the long game and these competitors are playing a short (and painful) game.

5. A model that wins in the long-term

Adyen is operating a business model that focuses on product differentiation.

On top of that, all the functionalities and products are made available on a single platform.

As a result, Adyen is able to run its business very efficiently, meaning it operates at a very low cost.

At the same time, it also offers the best product and highest functionality.

One disadvantage of this model is that it takes time to build new products and functionalities because Adyen does not do acquisitions, so it needs to hire the right team for its strategy.

While Adyen can definitely choose to compete on price, it has chosen this business model because it is the sustainable one that wins in the long-term.

It allows Adyen to be in a unique position to invest and deliver the best product to customers and bring about a flywheel effect.

In my opinion, while any company can compete on price, the best companies compete on product differentiation, which creates a more sustainable moat.

6. Valuation

Adyen $ADYEN $ADYEY is trading at 30x 2024 P/E.

While not exactly extremely cheap, I think that this is a more than a reasonable valuation for a company like Adyen, which is growing at 30% EPS CAGR from 2024 to 2026, with a solid management team with a long-term view, a long growth runway in payments and continued investments in its business to improve its differentiation and competitive moat.

7. Concluding thoughts

I think this should be an easy buy decision for long-term investors given that the market selloff was largely driven by investors with a short-term mindset.

This is a high quality compounder, in my view.

Given that Adyen has an impressive 5-year average ROIC of 27%, as the company continues to invest in its business, this drives future returns on its business and further compound the business.

Solid free cash flow generation allows the company to have room to invest without needing any additional capital.

Bottomline here is that sentiment has certainly soured but I do think that we will see Adyen re-accelerate growth and boost EBITDA as soon as in 2024.

Given that valuation is now more reasonable, the opportunity set here looks attractive here to me.

Disclosure: I just started a position in Adyen.