🚨 DO NOT BUY A HOUSE THIS YEAR, UNLESS YOU’RE A BILLIONAIRE!

Rent for now.

Wait for a 2008 type market crash to buy your first house.

I’ve seen every cycle from the 2008 crash to the 2020 blow-off top.

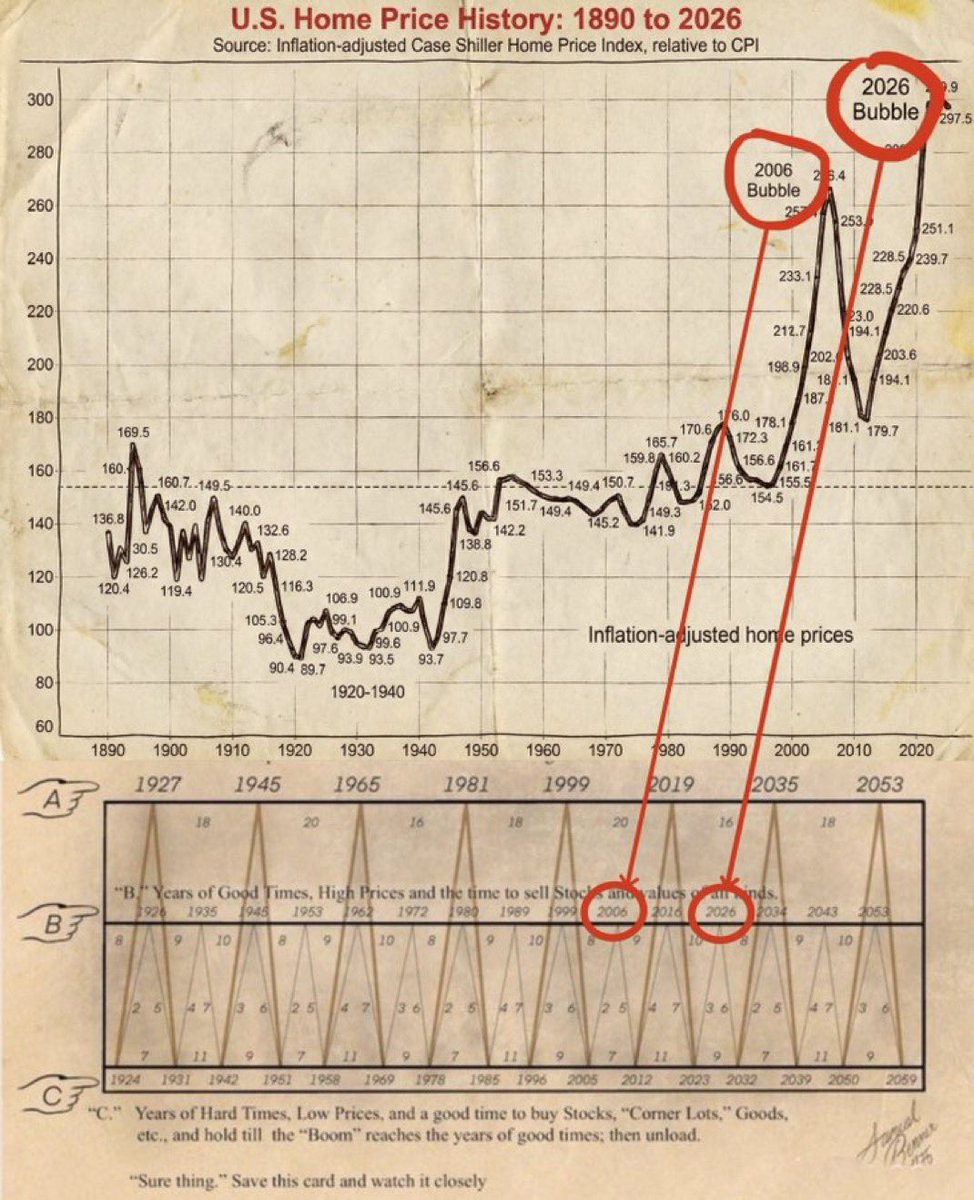

Take a look at this chart.

This 2006 bubble topped around 266.

If you think the current market is safe, you’re overlooking a deep structural stall.

Buying in 2026 is a TRAP, here’s why:

Redfin data shows a massive imbalance: 36.8% more sellers than buyers. Demand is at its weakest level since the 2020 lockdown.

This isn't a healthy pullback, it’s a breakdown in market momentum.

Most homeowners are locked into ~3% mortgages. With 30-year fixed rates stuck around 6.5%, the cost of moving is simply too high.

That means no real price discovery. People can’t afford to transact. You’re paying a sticker price on an illiquid asset that hasn’t been stress-tested by real volume.

Buying now locks you into a punishing monthly payment while upside remains limited.

If you’re levered 5:1 on a house that goes nowhere while you're paying 6.5% interest, you’re not compounding wealth, YOU’RE BLEEDING CAPITAL.

THE MACRO PLAY:

Wait for the exhaustion phase in late 2026/2027.

That’s when the "wait it out" crowd hits life catalysts (divorce, relocation, retirement) and is forced to sell into a cooling economy.

That’s when the affordability reset actually happens.

If you must buy, do it like a shark:

– Stress-test your income for a 20% drop.

– Keep your LTV conserstive (avoid negative equity).

– Only buy if you can survive a decade of flat prices.

Numbers don’t care about feelings. Don’t let your dream home turn into a zombie asset.

I’ve studied macro for 10 years and I called almost every major market top, including the October BTC ATH.

Follow and turn notifications on. I’ll post the warning BEFORE it hits the headlines.