Wockhardt’s 25-year bet is finally paying off. 💊

While most global pharma companies exited antibiotic research, Wockhardt stayed committed.

The result? Zaynich—the first novel drug discovered, developed, and owned by an Indian pharmaceutical company to receive US FDA approval.

Why Zaynich matters to Wockhardt:

• Invested ₹6,800 crore over 25 years in R&D.

• Developed 6 novel molecules, with 3 already commercialized.

• Phase 3 trial success: 89% vs 68.4% for the standard treatment.

• Targets a $7–9 billion market with $1.5–2 billion peak sales potential.

• Wockhardt returned to profit in FY26 and aims to become an innovation-led global pharma company, with Zaynich as its biggest growth driver.

This is more than a drug approval.

It marks India’s shift from a generic medicine powerhouse to a global drug innovator.

#Wockhardt #Zaynich #Pharma #IndianStocks

#HSCL raises stake in IBC to 20.47%

Linked to commercial rollout of HSCL's LFP cathode & advanced anode materials

Access to IBC's R&D (California), manufacturing (South Korea) & upcoming Bengaluru gigafactory

Strengthens HSCL's downstream play in the battery value chain

#NIFTYMIDSML400 is now 7.62% away from its 20 SMA.

This kind of move doesn’t come from weak hands. Bulls are clearly in charge.

Last time we saw this was right after the 2020 crash.

What followed was a long, relentless rally.

With its longest-range mass-market scooter yet, Ola Electric doubles down on vertical integration and indigenous cell technology to widen EV adoption in India

(@avishekb001 reports)

#OlaElectric#EV

https://t.co/PrYRSFWGyX

Study This Company :

Investing in Cartrade=Investing in OLX +CarWale+BikeWale.

Now 40% down from AlltimeHigh.

Trading at just PE 40 with ₹1,145 Cr cash in the bank.🔥

#CarTrade is the ONLY internet company with such a powerful business at this cheap valuation.

Debt-free + cash-rich + 30%+ growth + fresh AI push.

No Financial advice, DYOR

#Nifty 24480

I'm no more bearish at these levels. Probably a bounce and then retest of today's lows (or slightly lower) and that should be it. We then go higher in a 5 wave advance:

#Nifty 25178

All those who are worried about with what will happen tomorrow should take comfort from the fact that there is demand zone just 200 points lower. A horizontal demand zone and a rising channel both meet around 25000 zone so that will provide good cushion to any sharp pullbacks at open tomorrow:

Quality power management expecting more than 900 crore in revenue with 22% margin in FY26.

Revenue triple from 300 to 900 compare to previous year.Another Multi bagger.

You can buy and hold this stock for 5 year it can give 5x return.

#QPower#Multibagger#Power #StockMarketIndia

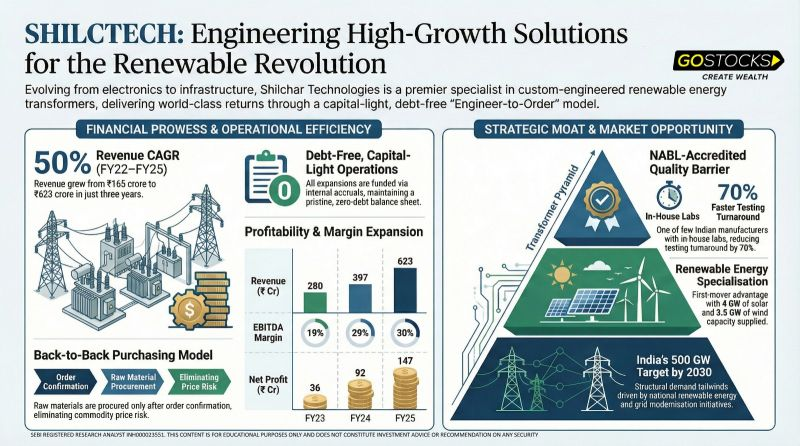

Shilchar Technologies :

The "Engineer-to-Order" Moat : Why Customization is King

Shilchar has successfully moved away from the traditional "stock-and-sell" commodity model to a sophisticated Engineer-to-Order (ETO) philosophy. Every transformer is custom-designed from scratch by an in-house team of over 15 electrical and mechanical engineers.

This creates a powerful technical lock-in: once a customer commissions a Shilchar-designed unit for a 100MW solar farm, switching to a competitor involves re-engineering and re-qualification by utilities that can take 6 to 12 months and cost upwards of ₹20–50 lakh in additional engineering fees.

This technical "stickiness" is most visible in the renewable segment, where the repeat order rate is a staggering 85–90%, compared to just 40–50% in the general industrial sector. The company's leadership remains deeply rooted in this technical excellence, with a founder-led focus on the design room rather than just the boardroom.

Shilchar Technologies is on a trajectory to reach 14,000 MVA of capacity by 2027, but the real story is its move up the value chain. The entry into the 220 KV class transformer segment is the company's "crown jewel" expansion.

This shift moves Shilchar from being a distribution-level player to a transmission-level infrastructure provider, a domain previously reserved for the world’s largest industrial conglomerates.

While the sector remains subject to commodity cycles and forex fluctuations, Shilchar’s 30% margins suggest that in the energy transition, the real value lies in the intelligence and reliability of the infrastructure that binds it all together.

Market cracked. But 4 stocks didn’t get the memo:

🟢 Newgen Software +17.19% (Vol: 61m — massive)

🟢 Datamatics +13.67%

🟢 Tata Inv Corp +7.50%

🟢 Oil India +5.13%

Rule #1 of price action — stocks that refuse to fall when everything else does are telling you something.

#JustStox

Only problem with market is that the biggest buying opportunity comes when we all are frozen with fear…looks like the bear market in small caps has officially ended with Donald Trump’s tweet signing trade deal with India

Wonderful to speak with my dear friend President Trump today. Delighted that Made in India products will now have a reduced tariff of 18%. Big thanks to President Trump on behalf of the 1.4 billion people of India for this wonderful announcement.

When two large economies and the world’s largest democracies work together, it benefits our people and unlocks immense opportunities for mutually beneficial cooperation.

President Trump’s leadership is vital for global peace, stability, and prosperity. India fully supports his efforts for peace.

I look forward to working closely with him to take our partnership to unprecedented heights.

@POTUS@realDonaldTrump

If this can happen, then gold prices may reach ₹10 lakh per 10 grams because of de-dollarization. If the whole world starts de-dollarizing and major countries like BRICS begin dumping dollars, gold could emerge as a new currency and source of power, potentially driving its price to ₹10 lakh per 10 grams.

Company: Rama Phosphates

Update Type: Board Meeting Outcome | Sentiment: Positive 🟢

Summary: Q3 standalone net profit surged 283% YoY to ₹1,402.56 lakhs; revenue grew 32% to ₹23,822.69 lakhs. Management reported record nine-month performance. Key unique developments include receiving Environmental Clearance for the Dhule greenfield project (trial production Q4 FY2026) and a five-year lease extension for the Nimbahera unit.

Rama Phosphates Ltd Q3 FY26 Results: ₹238 Cr Quarterly Revenue, PAT Rockets 283% YoY, EPS ₹3.96 – Revival or Just One Good Monsoon?

1. At a Glance – Blink and You’ll Miss the Turnaround

Rama Phosphates Ltd, a name that spent years quietly sitting in the “cyclical, boring, subsidy-dependent” corner, suddenly woke up in Q3 FY26 and chose violence — the good kind, the balance-sheet-cleansing kind. With a market cap of around ₹649 crore and a stock price hovering near ₹185, this fertiliser-and-chemicals veteran just posted quarterly sales of ₹238 crore with a net profit of ₹14 crore. That’s not typo money; that’s a 283% YoY profit jump, the kind that makes screeners blush and Telegram channels foam at the mouth.

Debt is down to ₹103 crore, debt-to-equity sits at a modest 0.26, promoters are holding a chunky 75% stake, and the company is no longer in the ICU of CDR. ROCE is still a sleepy 7.81% and ROE is a grandma-like 3.77%…

Read full piece: https://t.co/mA7SMiYSCv

Balu Forge Industries Ltd Q2 FY26: Forging Profits Hotter Than the Steel They Make — ₹2,995 mn Revenue, ₹650 mn PAT, OPM 28%, ROCE 31%, and Still No Smoke Breaks in Belgaum

1. At a Glance

Balu Forge Industries Ltd (BFIL) has officially become that rare Indian smallcap that can flex both biceps — growth and margins — without tripping on leverage. The company clocked ₹2,995 million in consolidated revenue for Q2 FY26, up 34.4% YoY, while net profit jumped 35.5% to ₹650 million. The Operating Profit Margin (OPM) stood tall at 28%, with a ROCE of 31.3% and ROE of 25.4%, reminding every engineer why crankshafts deserve more love than crypto.

At a market cap of ₹7,151 crore and a P/E of 29.3x, the market’s already giving them a decent “forged premium.” But hey, when you grow sales by 49.8% and profits by 79.7% in a year, you can afford to strut. The company’s debt is a mere ₹81.5 crore, and with a debt-to-equity ratio of…

Read full piece: https://t.co/LL7OOcg5PZ