Current holdings, in no particular order 👇🏻, DYODD.

🇺🇸 $SMDRF 🇨🇦 $SM.V

@SierraMadreSM

🇺🇸 $GLGDF 🇨🇦 $GGD.TO

@GoGoldResources

🇺🇸 $PGLDF 🇨🇦 $PGLD.V

@P2_Gold

🇺🇸 $BKRRF 🇨🇦 $BRC.V

@BRCSilver

🇺🇸 $KNTNF 🇨🇦 $KNT.TO

@K92Mining

🇺🇸 $VZLA 🇨🇦 $VZLA.TO

@VizslaSilver

🇺🇸 $APGOF 🇨🇦 $APGO.V

@corp_apollo

We have trimmed VZLA & GGD to make room for a new large holding, Blackrock Silver.

The recent pullback have enabled us to add significantly to Sierra Madre, making it our largest PM holding. We believe a significant rerate is coming in the coming 12 months and beyond.

Smaller holdings and new ideas not posted here.

Gold just touched MA200 after months of consolidation.

Lows are already in SILJ & GDXJ.

The next major run in precious metals & junior mining stocks are getting close, our guess a couple of weeks away, give or take.

Carpe diem.

Of course you have an angle.

Re yr 10 points. You're 100% correct on #4 (pollution). #9 & #10 I wouldn't know, individually both correct/incorrect I'm sure. The other 7 points, I would argue are downright false. But that's from my own >20 years personal experience.

That ends this polite discussion on my side. Wish you a very pleasant day 🤗

#thailand

It's all about personal preference and you give your opinion. All good so.

But it's not one fit all and you run your business on your agenda. Also good.

But don't expect your opinion to be the absolute truth to all and everyone.

And again, several of your bullet points were false.

In a conversation with @ResourceTalks, $SM.V CEO @alex_langer, discussed the Company’s strategy for growing profitable production in Mexico, advancing the La Guitarra and Del Toro assets, and creating long-term shareholder value through disciplined expansion and exploration.

📺 Watch the full interview here: https://t.co/okfIefiVcc

$SMDRF | #SierraMadre | #SilverMining | #Mexico

Crux coverage on @P2_Gold

🇨🇦 $PGLD.V 🇺🇸 $PGLDF

Peer comparisons highlight the valuation gap.

$PGLD.V $213M MCap atm

$USAU US Gold, a direct comparable Gold-Copper developer, trades at $350 million despite P2's NPV5 being approximately double at similar metal prices.

$LGD.T Liberty Gold and $DC Dakota Gold command valuations of $805 million and $966 million respectively, suggesting 4-5x upside potential if P2 achieves comparable market recognition.

"At current spot prices, the project delivers exceptional economics with a net present value exceeding $3 billion at a 5% discount rate and an internal rate of return surpassing 100%. The October 2025 PEA outlined production of 109,000 ounces of gold annually plus 33 million pounds of copper over a 14-year mine life. However, management is evaluating a 33% throughput increase that would boost output to over 200,000 gold-equivalent ounces annually.

A critical differentiator is P2's royalty-free structure, providing an estimated $250 million financing advantage unavailable to royalty-burdened competitors. This flexibility becomes particularly valuable as the company approaches construction financing decisions in 2027-2028."

🚨 JUST IN: President Trump says Kevin Warsh will PLUMMET Fed interest rates, which will help Americans afford houses

"I had a ROTTEN head of the Fed. Now I have a great head of the Fed. Kevin Warsh!"

"Housing is all about interest rates. I know more about housing than anybody in history. No president. And they can pass all the bills they want. It's about interest rates."

"You get the interest rates down. Everybody's going to be very, very happy. We're going to get it down very quickly."

One of the better interviewers of mining juniors is Antonio Atanasov who runs @ResourceTalks.

His talk from May 13th with @alex_langer, CEO of @SierraMadreSM, was absolutely great.

Antonio's non-biased approach of not charging the companies for these talks gives a credibility few others achieve.

https://t.co/oiw8nF3ujh

Sierra Madre Receives Mexican Antitrust Approval for the Acquisition of the Del Toro Mine

🇺🇸 $SMDRF 🇨🇦 $SM.V

@SierraMadreSM#silver#gold https://t.co/arq1C8JdJK

Important 2 minutes at the end, view & listen below.

The 1st phase of production expansion is coming online now at the end of Q2, a ~50% increase. Also, it seems as if @SierraMadreSM has fast-tracked the phase 2 build-out, getting ready 1 full year ahead of schedule.

As they reach 1,500 tpd, they will triple current production capacity. This will not only increase ounces produced, but will also cut production costs significantly.

https://t.co/RY91q37HIC

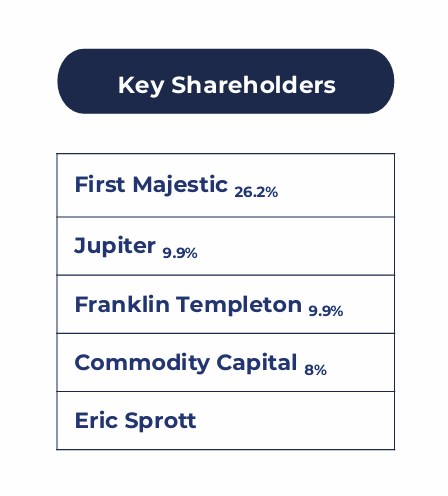

Not all juniors have these kind of institutional shareholders. If one include our holding of @SierraMadreSM , ~80% of the outstanding shares are in firm hands.

We suggest investors should consider what that will do to the share price when #silver hits $150/oz and money start to rotate into the junior mining sector.

🇺🇸 $SMDRF 🇨🇦 $SM.V

CEO @alex_langer has been buying shares or @SierraMadreSM in the market since inception. This week he continued buying.

We love to see mgmt teams with a large ownership in the company they work for. You want them incentivised and not working for a salary only (tend to not end very well).

Insiders own ~25% of Sierra Madre. Ask yourself what that does to how they run the business. This is one of many reasons why we have made SM a large portfolio holding.

CEO @alex_langer has been buying shares or @SierraMadreSM in the market since inception. This week he continued buying.

We love to see mgmt teams with a large ownership in the company they work for. You want them incentivised and not working for a salary only (tend to not end very well).

Insiders own ~25% of Sierra Madre. Ask yourself what that does to how they run the business. This is one of many reasons why we have made SM a large portfolio holding.

New webinar alert! 📺

$SM.V Executive Chairman & COO Gregory Liller and CFO & Corporate Secretary Ken Scott joined @adelaide_cap for an investor update highlighting record Q1 revenue, ongoing expansion work at the processing plant, development progress at the Coloso and Nazareno mines, and the Company’s strategy to continue advancing toward becoming a mid-tier silver producer.

⤵️ Watch here:

https://t.co/7F5GG0LWjh

$SMDRF | #SierraMadre | #Mexico | #Silver

Sierra Madre @SierraMadreSM just reported a record Q1.

Revenue hit US$10.1M — more than double Q1 last year.

That’s real operating leverage showing up as silver and gold prices strengthen.

But the bigger story may be what comes next: La Guitarra expansion, improving grades, Del Toro still ahead, and drilling planned for H2.

@TedJButler breaks down what matters in the full update inside today's Silver Advisor

https://t.co/WbCLZoAKQ7

#Silver #Gold #MiningStocks

Assays from @P2_Gold

🇨🇦 $PGLD.V 🇺🇸 $PGLDF

"P2 Gold Intersects 183.0 g/t Gold & 4.0% Copper Over 1.52 Meters within a Longer Mineralized Interval at the Lucky Strike Zone"

This release carries considerably more value than just the headline hole.

Several holes returned notable intercepts, Lucky Strike now demonstrates the same grade controls as Sullivan, letting the existing mine plan template carry over, and visible gold was intersected in a 100-metre step-out into ground with no prior drilling. Most importantly, management confirms Lucky Strike continues to host high potential for expansion and "has the potential to be significantly larger than the Sullivan Zone."

In Joe we trust 👏

Updated MRE in Q3 & FS in Q4 📈

https://t.co/JTQR6Y2d6s

The 10-year Treasury yield is perhaps the most important financial benchmark in the global fiat system, as it drives valuations and market trends worldwide. It is widely—and erroneously—regarded as the risk-free rate of return.

The 10-year Treasury yield can be thought of as a key barometer of the US dollar-based fiat system—a critical measure akin to its beating heart.

Bond yields move inversely to bond prices. When bond prices fall, bond yields rise.

A rising 10-year Treasury yield signals trouble for the US dollar because it means investors are selling Treasuries, which pushes up the US government’s borrowing costs. That is why the 10-year Treasury yield is a major pain point for the US government.

The 10-year Treasury yield was 3.97% when the war started. Now it is around 4.60%, an increase of roughly 63 basis points.

I expect the 10-year Treasury yield to keep climbing over the coming weeks and months—until it forces the Fed’s hand. At that point, the intervention will be sold as “stability,” but the mechanism will be familiar: suppress yields by debasing the currency.

At today’s debt levels, every 1 basis point increase in the government’s average borrowing cost adds roughly $3.9 billion in annual interest expense. So a 63 bps rise is not trivial—it translates to nearly $250 billion in additional yearly interest costs, materially widening a 2025 budget deficit that was already around $1.8 trillion.

Higher yields mean the US government must pay tens or even hundreds of billions more in interest on its debt. At the same time, the global economy faces even greater added costs because Treasury rates serve as the benchmark for borrowing worldwide.

That is not an insignificant move. However, given all the headwinds I have discussed, I suspect the 10-year Treasury yield is headed much higher because investors will demand higher yields to compensate for rising inflation. Further, if Hormuz remains closed, drastically higher oil prices are all but certain. Higher energy prices mean higher prices across the economy and higher official inflation rates, which means investors will demand still higher yields to compensate.

The problem is that interest on the federal debt is already over $1.2 trillion and is now the second-largest item in the budget. The US government cannot afford yields going much higher because the interest expense would push it toward bankruptcy.

I am not sure how—or even if—the US government can manage this situation. Something has to give, and we will not have to wait long to find out what.

The Iran war may prove to be more than another foreign policy disaster. It could be the trigger that exposes the fragility of the entire dollar-based financial system.