Started a post with intention to share portfolio moves since mid March, but got into portfolio management a little bit. Usefulness of cash position for psychology, thin line between investing-trading and some food for thought.

https://t.co/7YdjHOYX6L

@AstutexAi -Not pure, but a tailwind for sure. CEO mentioned they also working to extract certain new protein that will "contribute significantly"

https://t.co/50reV5pEyp

-rally on thin volume, order book

-input/output(though lagging) prices support margin expansion

https://t.co/Vk8wREqIi3

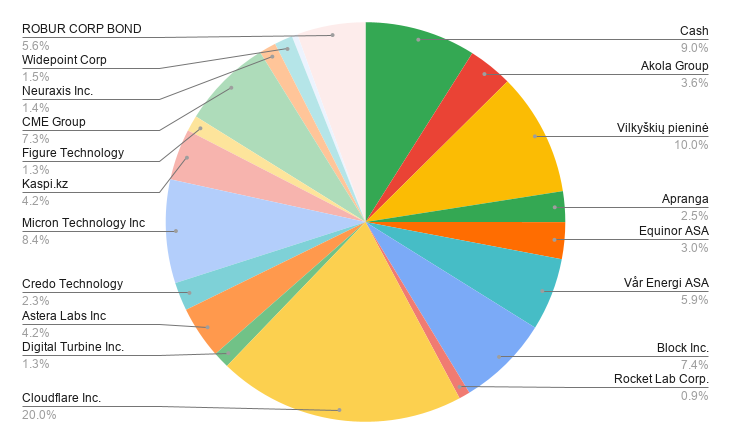

1/2 Migrated portfolio administration to gsheets.

P.S. Paragon Advanced Labs ($PALS) - no label

Recent moves:

1. increased $WYY x2 at $18.89. Shallow work w/ LLMs point to significant EPS, FCF ramp in 2027, after winning significant contracts. Will monitor guidance in next call

Great Britain is restructuring its army based on the "Ukrainian model".

The British government has released a defense investment plan. Its core philosophy marks a shift away from the old concept of "expensive toys" in favor of the tactics Ukraine has used to decimate the Russian army.

The Royal Navy will no longer receive funding to develop up to eight Type 83 destroyers and Type 32 frigates. The war in Ukraine has demonstrated that massive, costly ships are vulnerable.

Instead of investing in floating fortresses, Great Britain is investing in at least six command vessels. These are designed to coordinate swarms of underwater hunter drones, unmanned missile platforms, and aerial sensors. The British acknowledge drawing inspiration from Ukraine, which—despite lacking a navy of its own—has devastated the Russian Black Sea Fleet using a combination of sea drones and missiles.

The government is allocating £5 billion exclusively for "drone transformation" (Ukraine deploys around 200,000 drones per month).

Great Britain will establish Europe’s largest testing center for unmanned aerial systems (UAVs), as well as a dedicated unit to continuously ramp up production.

The Royal Air Force is launching a program for autonomous jets designed to fly alongside manned combat aircraft as robotic wingmen.

Ukraine should carefully consider whether it wants to include NATO in the Ukrainian defense alliance.

@DeItaone I vividly remember, big tech bond yields having lesser yield than 10Y treasuries. Big tech balance sheets look way nicer to investors.

So what Apollo should be asking instead: who will buy US Treasuries?

Bought $INTC on a two pillar thesis before trump in July 2025:

-Lip-Bu Tan transformation ($CDNS trust transfer)

-Taiwan insurance during most incompetent WH admin. US based advanced node fab insurance

Sold after merely x2. Keep thinking I need to be back in. Pillars still there

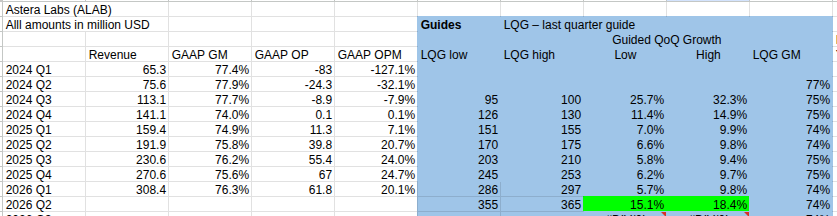

Not an easy hold. $ALAB +196% YTD

Trades at TTM 264 P/E, yet next qtr cons. revenue is avg of mgmt guide. Astera consistently beat their guides by on avg. 11% since 24'Q3

Their Q2 guide shows significant acceleration, right as Scorpio X ramps, which market rightfully prices in

Usually a lurker on here but dipping my toes briefly into the "k-shaped economy" discourse.

At PNC we track the debit & credit spending trends of a fixed cohort of ~4 million households.

Long story short: lower-income spending/balance sheet trends have been on a tear in 2026

2/2

2. Took small position in $RKLB today at $90 after $IRDM acq. news. There are only 2 companies with proven track record of space launches. Acquisition expands TAM and it's a sector I believe only few companies will dominate, and one of them should be worth a lot more than 50B

So $MSTR went from "never sell" $BTC to "we only sold a meaningless amount" to "we can now sell $1.25bn to prop up our preferreds". So if you're a common shareholder, you know exactly where you stand. And if you own Bitcoin, you know your most bullish proponent said "our Prefs are the most important thing to us". Economically the right decision, (i.e. buyback of prefs at discount AND stock etc), but the problem is you're selling the very commodity you built your entire strategy around. I get the short-term pop, but they no longer have the premium to NAV funding which enabled the entire structure to perpetuate. And historically, when I've seen companies lose their premium, their acquisition currency, despite all the capital structure gymnastics, it doesn't bode well for future returns. I've seen this happen w/ companies that are serial acquirers and they lose their valuation premium, and the whole valuation construct falls apart. Curious if others have a different read.

UBS raises $MRVL ´s PT to $340 and $ALAB ´s PT to $400 as it becomes more bullish on the long-term CXL opportunity as well as some decent estimate updates for CY27E and CY28E.

Arcuri believes CXL is moving from an emerging technology to a critical enabler of agentic AI infrastructure. As CPU architectures evolve and AI systems become increasingly memory-intensive, the firm expects CXL fabrics to connect CPUs, XPUs and memory pools across racks, significantly expanding the addressable market.

He also thinks the next wave of AI infrastructure isn't just about faster accelerators but about connecting CPUs, XPUs and memory more efficiently. If that thesis plays out, CXL could become one of the most important interconnect technologies of the second half of the decade.

Huawei Shanghai R&D Campus:

30,000 research personnel, average age 31.4. Exactly one year ago, the headcount was 10,000 lower, but the average age stayed the same.

@SouthernValue95 It literally doesn't matter? CXMT cannot satisfy China demand this decade. So there's 0nreason besides the small price arbitrage. It's like bannin Iranian oil. India and China buy it anyways, but price diff is less