If you want to be a long term investor of SPCX, buy $SATS.

Its market cap is 32B, but its SPCX holding worth 43B, and they have other business worth about 30B, with ~15B debt.

The discount in $SATS now is caused by those who cannot sell SPCX (PE/VC/Employee/IPO). So they short $SATS to hedge.

The discount window will close when they are allowed to sell. The first batch will be unlocked when SPCX's price is above 30% of its IPO price ($135), aka $173.5, for 5 days.

$SPCX is now $175.5. So the probability that this discount disappear in next week is greater than 30%.

So buy $SATS, if you believe in Elon and in $SPCX.

Thanks to @Nasdaq bending their listing requirements for $SPCX, passive funds will soon be obligated to buy in at just a 5% free float, with a 3x multiplier.

$SPCX becomes optionable tomorrow—Go long on the manufactured demand, and given that insiders can only sell when it is trading at a 30% premium, many will offload, and that'll be the top to short 🎯

Will be the same story with the @OpenAI & @AnthropicAI #IPO's 📌 it #AI

Goldman Delta 1 head on recent drop in compute rental prices

"For me, the most important metric remains compute rental prices. The market’s central premise has been that compute is scarce. If scarcity persists, prices should remain firm and justify continued capex. If supply rises and rental prices continue to drift lower, that is a direct challenge to the shortage narrative. The first place that pain shows up is hardware. ORNN H100 index rolling over last couple days worth watching. The beneficiaries are the companies selling the complete platform and monetizing usage rather than simply selling picks and shovels. My working conclusion remains that hyperscalers are the structural winners through this phase. The first moment they demonstrate they can deliver equivalent output with lower spend, the market will reward them. The bigger risk sits further upstream in the hardware and infrastructure stack where expectations remain built around persistent scarcity."

BREAKING: Iran says the US has agreed to pay $300 billion in reconstruction funds directly to Iran as part of the deal Pakistan announced, alongside the release of $24 billion in frozen funds with $12 billion released before negotiations even start, per Mehr News.

This directly contradicts Trump's & Vance's claim that no funds will be transferred to Iran at all.

If Trump denies this is true, there never was a deal. If Trump confirms, the US has fully capitulated to Iran's demands.

$SATS closed out Friday at a 45% implied discount to NAV after blowing out at close to 50% intraday

As it stands, $SATS share price of $114 is exactly equal to its shareholding in $SPCX (NET of any hypothetical CGT)

Of course, EchoStar also owns >$40B of spectrum assets (of which 78% already in the form of cash receivables)

Assuming zero OpCo equity value in its legacy businesses (still some optionality here), this yields an extra $73 NAV / share net of further HoldCo liabilities

NAV spread trades are always part art / part science and often hinge on being opportunistic – I think the intraday move on Friday was one such dislocation and ended up compounding back-in at <$110 for the first time since late 2025 purchases in the $75-85 range and some sales in the $130-140 area.

A Renaissance Technologies partner just broke the silence on the fund that makes 66% a year and has never accepted a dollar of outside money

David Magerman wrote the algorithms. then he watched what the money was funding.

"we're not here to help America"

he said it out loud - and Wall Street's most secretive firm tried to make him disappear

1 hr on how the machine was actually built

bookmark & watch. this is the inside account nobody got

Ron Baron asked Elon Musk how Tesla invests $7 billion in a single factory and makes $15 billion a year in profit from it

Musk: "no one was expecting Tesla to be the best at manufacturing in the auto industry - probably in the history of the world "

Baron: "who does that? "

to reach it, Elon slept on a factory floor for 3 years

Ron bet $400M when everyone said Tesla would fail - never sold a single share - made $7B

25-min between a near-trillionaire and the investor who believed in him

bookmark & watch today ↓

This is the chart that everyone should be watching.

If the Token Pricing rolls over, everything from the memory trade to the broader hard-ware and data-centre trade is over for this cycle imho.

The whole setup depends on this..

Stanley Druckenmiller averaged 30% a year for 30 years without a single losing year

Paul Tudor Jones asked him on stage what made him different from everyone else - his answer: size

"I put 350% long into one bond trade - 200 to 300% of my fund into a single currency - put all your eggs in one basket and watch the basket carefully"

"I've never used a stop loss in 40 years - I exit when the reason I bought changes, not when the price is down"

"the world changed on 9/11, the world changed when the wall came down, the world changed election night - these moments set in place two to four-year trends you can play"

bookmark and watch it today ↓

I valued SpaceX for its IPO a few weeks ago, with minimal information and a promise to revisit the valuation, when the prospectus was made public. The prospectus is public, the offering price has been set and my update is up and running. https://t.co/zRjpD1C0wv

🚨BREAKING: A cognitive scientist from MIT has mathematically proven that evolution guarantees we see zero percent of true reality, that most consciousness in the universe exists without a body, and that non-human intelligences with a wider window on reality than ours can reach in and manipulate it the way a programmer manipulates a video game.

Donald Hoffman (@donalddhoffman) is a cognitive scientist at UC Irvine who has spent 40 years building a mathematical theory of the observer. His work was cited by John Wheeler in the "It From Bit" paper. He studied under Marvin Minsky at MIT, spent two decades secretly meeting with Francis Crick to study consciousness, and has nine specific mathematical conjectures on the table that would derive general relativity, quantum field theory and the Big Bang from a single framework. The top high-energy physicists in the world, Nima Arkani-Hamed and Nobel laureate David Gross, are already saying spacetime is doomed. Hoffman thinks he knows what replaces it.

This interview is the first time he has publicly laid out what his mathematical model explains about alien life, embodiment and the structure of reality.

It already derives time dilation and quantum wave functions directly from differences in observer window size. Physics has spent a century failing to solve the measurement problem because it has been looking in the wrong place. The observer has to come first, and no physicalist framework can get you there.

A consciousness with a larger observer window has access to the underlying structure of our reality in ways we can't perceive or counter. A craft going Mach 40 instantaneously in our headset could be a leisurely maneuver in theirs.

The implications for UAP and alien life are immense.

Embodiment, being locked into a body with fingers and toes as your only interface with the world, is a probability zero anomaly in the full space of possible minds. He also says current large language models are dumber than cucumbers. His new framework, the recursive trace logic, is a completely different architecture, and some of the biggest names in frontier AI have already come to him about it.

The framework has no ceiling, and the implication is a single unified consciousness exploring itself through an unbounded number of perspectives, each one capable of waking up.

Death, in this framework, is just the closing of an icon on the desktop.

Full conversation is live now.

U.S.–IRAN PEACE HOPES COLLAPSE

Market expectations for a U.S.-Iran deal by end-June have plunged from over 75% to just 27%. Chance of Strait of Hormuz reopening is now only 22%.

Kalshi traders give just 52% probability of normal shipping traffic before October 2026.

Stalled nuclear talks and renewed clashes are hitting sentiment hard.

https://t.co/dF0iM6Jgcg

$GOOG Hyperscalers, NeoClouds, and LLC off balance sheet borrowing are now gone.

KKR borrowed $400m today at 8%

SoftBank borrowed $990m at 9% Friday

The past couple weeks hyperscalers were scrounging around in international bond markets to find money.

Now that money dried up, all of these companies have to use equity. Every round they raise increases dilution and risk of market collapse. Neoclouds are inevitable.

What does it mean for semiconductors? There is no longer infinite money to raise prices. There is demand destruction.

$soxx $dram $orcl

When $GOOG is forced out of bond markets because lending rates jumped above 9%… Lookout

👆Neoclouds and ability to use off balance sheet LLC leaseback strategies are gone.

Private Credit Markets are Failing.

Now comes pure share sales for the buildout. As Blackrock said, your savings and retirement will pay for ALL of it.

$IREN $ORCL $CRWV $NBIS

Nicolai Tangen, CEO of Norges Bank Investment Management pressed IBM CEO Arvind Krishna directly on whether AI is a bubble (Save this).

And Krishna responded with what has become known inside financial circles as the $8 trillion math problem.

A single gigawatt of AI data center capacity filled with accelerators, liquid cooling, and power infrastructure costs roughly $60 to $80 billion to build and populate.

The industry has committed to more than 100 gigawatts of buildout globally.

That is $6 to $8 trillion in capital expenditure and because AI grade hardware depreciates on a five-year cycle, that entire sum must be effectively replaced and refreshed every five years.

To service the interest on $8 trillion in capital at a conservative 10% borrowing rate, the AI ecosystem would need to generate approximately $800 billion in annual profit, a number that currently exceeds the combined net income of every large technology company in the world.

Goldman Sachs estimates $7.6 trillion in aggregate AI CapEx between 2026 and 2031 alone, and Reuters Breakingviews has flagged that even if the capital is available, physical bottlenecks power permits, land, cooling infrastructure, and electrical grid connections mean that half of the planned data center projects are being cancelled or delayed before they ever go live.

Krishna also raised a second, structurally distinct concern that markets have largely ignored.

He argued that the largest foundation models, GPT, Gemini, Claude, Llama are converging toward commodity status.

When a product is a commodity, switching costs collapse.

When switching costs collapse, pricing power evaporates and margins compress regardless of how much capital was spent building the capability.

Morningstar's equity research team conducted a review of 132 technology companies in 2026 and found that AI had caused moat rating downgrades across roughly 40 major stocks concentrated in enterprise software, IT services, and SaaS with Adobe, Salesforce, Workday, and ADP among the companies whose competitive moats have materially weakened.

The implication is that the companies spending the most on AI model development may be building an asset that is simultaneously the most expensive to produce and the most difficult to monetize with durable margins.

This bear case is serious but it is also incomplete and that is what makes Krishna's framing so important to understand precisely.

When pressed further, Krishna explicitly said he does not believe there is an AI bubble in the technology itself only in a subset of the infrastructure capital that is being deployed against speculative assumptions rather than proven demand.

He draws the same analogy, the fiber optic overbuild of the late 1990s. Dozens of companies went bankrupt laying cable that nobody was using.

And yet that exact "wasted" infrastructure became the physical backbone of every cloud company, every streaming service, every mobile network, and every modern AI training cluster that followed.

The builders lost, the infrastructure won.

And the companies that were built on top of it, Amazon, Google, Netflix, Salesforce compounded for two decades.

The question, as Krishna framed it, is not whether AI is real.

It is which capital deployment earns a return versus which gets stranded and crucially, whether you own the stranded assets or the companies built on top of them.

On winners, Krishna was direct that distribution is the moat on the consumer side, and enterprise is wide open.

The data supports this, Meta with 3.3 billion daily active users across Facebook, Instagram, and WhatsApp is building AI into a distribution network that no startup can replicate at any cost.

Meanwhile, the productivity evidence arriving in real time is beginning to challenge the bear case's revenue projections.

Jensen Huang just showed on stage at Computex that GitHub commits, the universal measure of global software output nearly tripled in the first months of 2026, effectively converting $3 trillion in developer salaries into $9 trillion in productive output.

That is measurable, real time economic value already flowing through the system and it feeds directly back into token demand in a compounding loop that Krishna's static CapEx math does not fully capture.

This is an excellent interview btw

Nicolai (Norwegian Sovereign Wealth Fund CEO) asks the IBM CEO if AI a bubble

Listen very very carefully to his answer

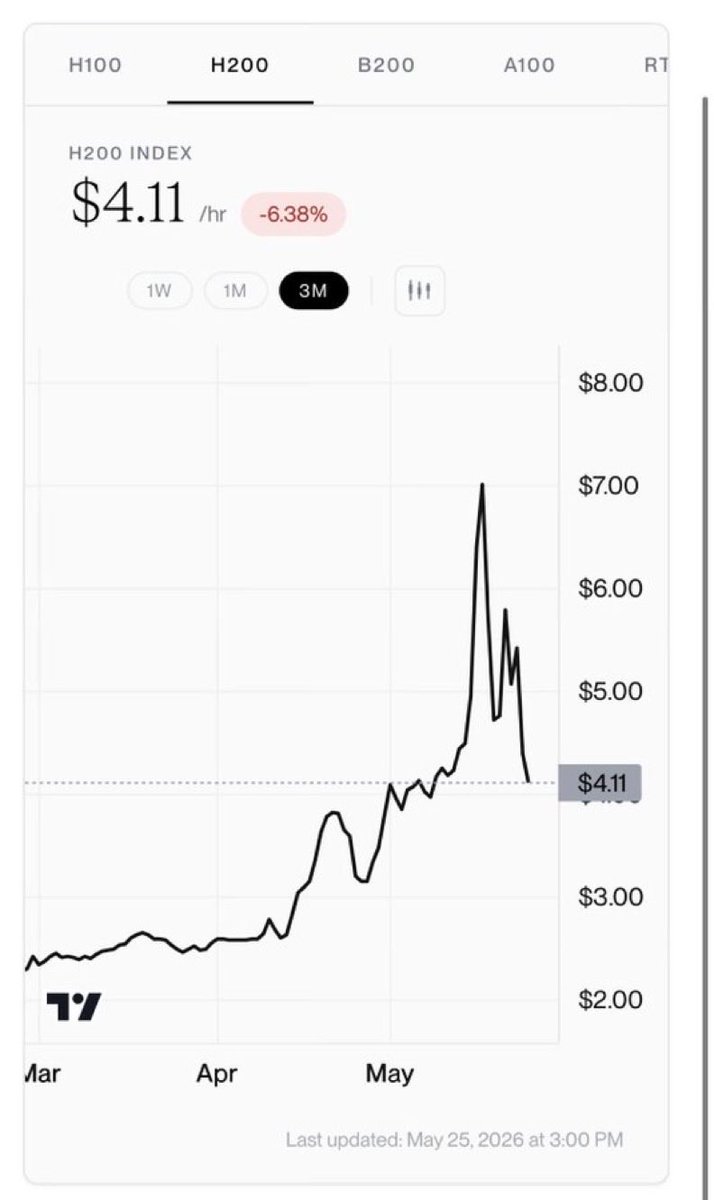

The price to rent an Nvidia H200 just collapsed from $7/hr to $4/hr in three weeks.

A -40% drop in the cost of the single most strategic asset in tech.

When the underlying commodity that powers your entire thesis loses 40% of its value in a month, that usually means one of two things: supply finally caught up, or demand was never as deep as the headlines said.

Either way, somebody is selling.

So why is the AI trade still pricing in scarcity?