I believe $BRUN is a screaming buy on a ridiculous sell-off AH. I believe it is the second best Neocloud investment behind $NBIS. I have added to my position.

Why the sell off?

A post was made on X by @saso_capital reporting ~54 million insider shares will become eligible to sell next Monday. Including 29.5 million Class B shares held by CEO Andrew Karos.

A few different financial influencers found out about this information and sold after-hours, notifying their followers. This created enormous selling pressure during an illiquid after-hours on a stock with an already extremely low float.

I don’t judge anyone’s decision to buy or hold a company. There is a potential risk of selling pressure lowering the stock price short term.

At the same time however, this is a unicorn neocloud stock with jaw-dropping growth metrics:

$BRUN ARR tripled from $30M to $96M in 4 months. Contracted backlog went from $120M to $1.45 billion as of June 1st. 1,233% year over year ARR growth. Free cash flow positive. $NVDA Preferred Cloud Partner. One of only 8 companies globally with Exemplar Cloud status. FY2026 ARR guidance of $400M+.

Karos owns 48% of this company. He built it. The pipeline keeps converting. The numbers keep accelerating. That is not someone who listed to dump.

The growth is real. The overhang is real. Both things are true. Likewise with my $IREN thesis, compute demand is insatiable, and a company as well-ran as Boost Run will likely explode in growth, and stock price.

Not financial advice. Do your own research.

Observaties vanuit het riool (2)

Het gesprek over X in Nederland raakt steeds verder los van het platform zelf. Wie talkshows, Kamerdebatten en opiniestukken volgt, krijgt de indruk dat X vooral bestaat uit politieke radicalisering, democratische ondermijning en permanente maatschappelijke ontwrichting.

Terwijl onderzoek naar het daadwerkelijke gebruik iets veel banalers laat zien.

Uit een analyse van Fingerspitz, gebaseerd op cijfers van onder meer Newcom Research, GWI en X zelf, blijkt dat het platform in Nederland in 2025 ongeveer 2,8 miljoen gebruikers heeft, waarvan circa 1,4 miljoen dagelijks actief zijn. De gebruikersgroep bestaat grotendeels uit mensen tussen de 28 en 59 jaar, met interesses die vooral draaien om sport, entertainment, technologie, reizen, gaming, financiën, muziek en actualiteit.

Dat klinkt niet direct als de voorhoede van een digitale staatsgreep. Wereldwijd worden dagelijks honderden miljoenen berichten geplaatst. Omgerekend naar Nederlands gebruik kom je al snel uit op vele miljoenen berichten per week. Tegen die achtergrond krijgt het Volkskrant-onderzoek naar 80.000 berichten aan politici tijdens een verkiezingsweek een beetje een ander perspectief.

Binnen de onderzochte selectie trof men honderden bedreigingen en duizenden berichten die als haatdragend of intimiderend werden geclassificeerd. Ernstig genoeg, zonder twijfel. Maar nog steeds een specifieke politieke steekproef in een verkiezingsweek. Het moment dat X met name druk is met politiek.

Niemand weet hoeveel accounts of personen daar precies achter zitten. Zoals op vrijwel alle sociale platforms produceert een kleine hyperactieve minderheid een groot deel van de zichtbare inhoud. Zonder inzicht in de onderliggende data blijft onduidelijk hoeveel activiteit afkomstig is van echte gebruikers, gecoördineerde actiegroepen of bots. AI maakt het eenvoudig om op grote schaal reacties, verontwaardiging en intimidatie te simuleren. Dat maakt de toon niet minder giftig, maar wel de analyse ingewikkelder.

Er wordt nu over X gesproken alsof het een politiek platform is. Maar tijdens verkiezingen gaat X over verkiezingen, zoals het tijdens het WK over voetbal gaat, bij de introductie van de nieuwe Ferrari over Ferrari en tijdens een NS-storing over gestrande reizigers. Wie op een willekeurige avond kijkt naar wat trending is, ziet geen aanval op de democratische rechtsorde, maar voetbal, reality-tv, beurskoersen, huizenprijzen, BN’ers, transfers, consumentenfrustratie en collectieve woede over een internetstoring.

X is in de praktijk geen ideologisch strijdtoneel eerder een permanent openstaande digitale kroeg. Een rumoerige plek waarin sportjournalisten, beleggers, gamers, politici, wielerfans, marketeers, complotdenkers en verveelde nachtbrakers ongecoördineerd door elkaar heen praten zonder structuur of hiërarchie.

Toch wordt juist die zichtbare politieke laag steeds vaker benoemd alsof die het platform als geheel definieert. Dat komt niet alleen door algoritmes, maar ook doordat journalisten, politici en opiniemakers elkaar permanent op hetzelfde platform observeren. De politieke bubbel kijkt voortdurend naar zichzelf en gaat die spiegeling uiteindelijk aanzien voor de maatschappelijke werkelijkheid. Daardoor ontstaat een vertekening. Een platform waarop mensen dagelijks praten over voetbal, muziek televisie, files, crypto, datingproblemen, vakanties en falende treinen wordt in het publieke debat steeds vaker beschreven alsof het hoofdzakelijk bestaat om democratieën te ondermijnen. Het zegt waarschijnlijk met name iets over de politieke en de media wereld die zichzelf op X dag en nacht in de gaten houdt.

I genuinely think $XFAB is very compelling at $1.5B MC, despite recent volatility.

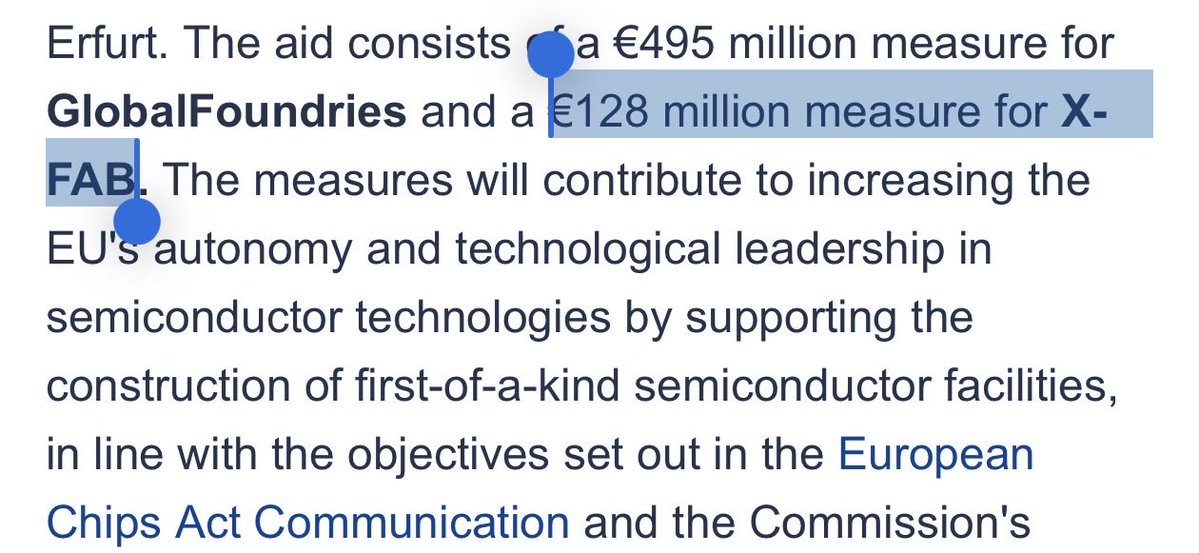

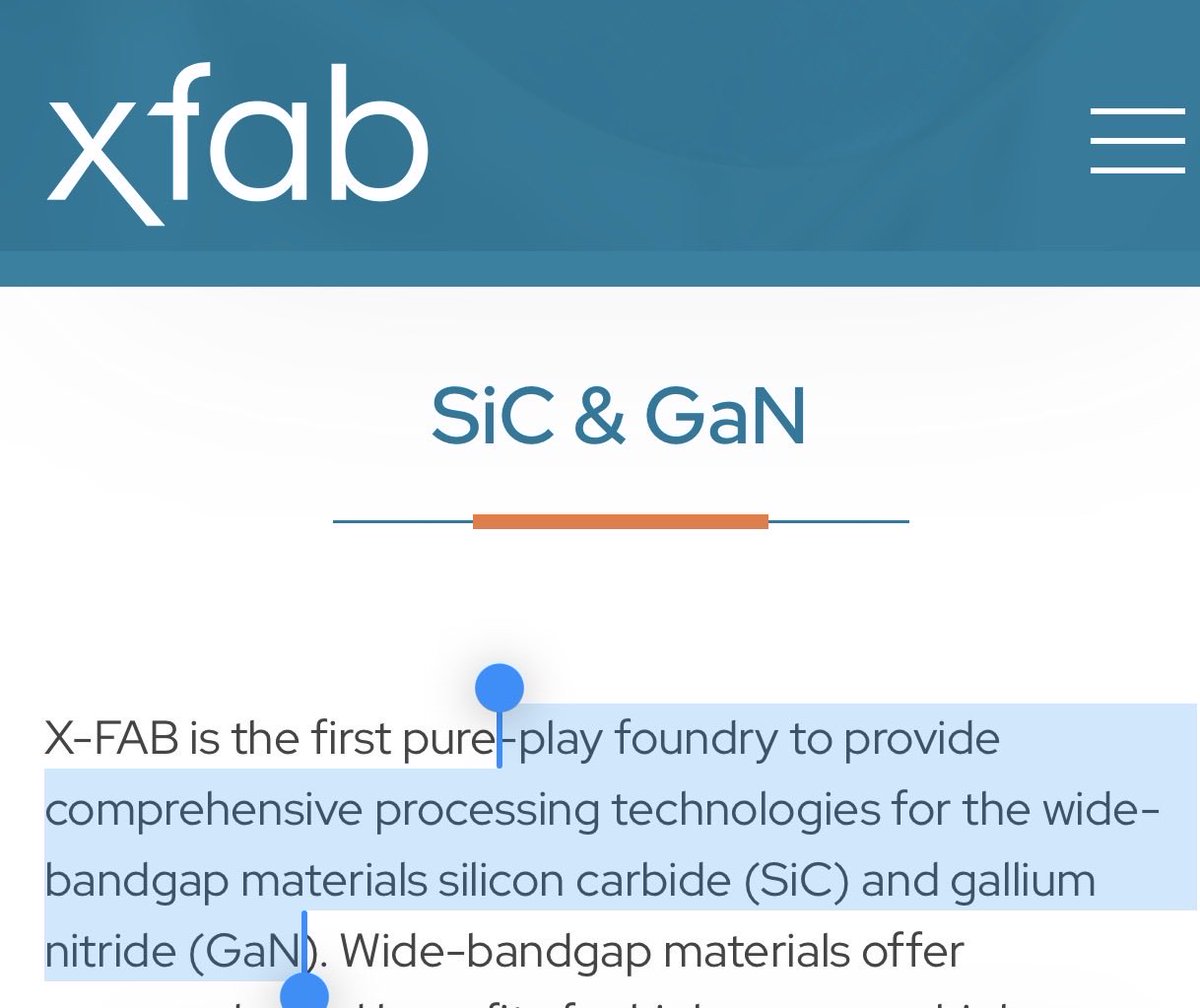

Per NIST filings stated they were the only high volume SiC foundry in America.

Making them extremely “critical infrastructure”… Verbatim from the US Gov.

And they’re the first comprehensive pure play foundry for SiC/GaN.

So it’s very compelling exposure as $NVDA pushes 800 VDC and as other power semi players from $NVTS and $WOLF are all re-rating hard.

For long term photonics exposure:

They were literally listed in CHIPS Act 2 blueprints… with $NOK / $NVDA evaluations right now.

And production ramp up in 2027/volume production H1 2028 expected.

So you have a company at $1.5B MC:

Critical both on the power semis front to the US government.

And critical to both photonics front to the EU government.

Coming off of a legacy drag cycle with auto and others (similar to Soitec).

I think I’d follow EU/US government signals for what’s critical infrastructure given expected dual continent subsidies…

Over random media analysts trying to cause unnecessary volatility saying it’s a memestock with no fundamentals.

@aleabitoreddit Thank you so much for generously sharing your insights and research @aleabitoreddit! Thanks to you I have realised my fastest 10-bagger ever with $SIVE.

@daniel_koss I often sell 50% of my position when I’m up 100%. That makes it easier for me to hold on to the other 50% and wait for it to 10x, labeling it as a ‘free ride’. I know I’m sort of fooling myself, but this mental accounting trick works for me.

JUST FINISHED READING $HIMS Q1 2026 EARNINGS.

-> DEMAND IS EXPLODING.

-> THE BUSINESS IS REACCELERATING.

-> AI, DIAGNOSTICS, PEPTIDES, AND PERSONALIZATION = ONLY JUST BEGINNING.

BUYING MORE TOMORROW.

👇

My overall view following this quarter is that Hims & Hers is now better positioned than ever to capitalize on what could become a multi-trillion-dollar shift toward personalized, preventative, and AI-driven healthcare.

Over the past two quarters, the business has had to navigate several major short-term headwinds simultaneously, including:

1. The fallout and later reinstatement of the Novo Nordisk partnership

2. The transition away from compounded GLP-1 products

3. The sexual health business transition

4. Revenue recognition changes tied to shipping cadence adjustments

These factors temporarily slowed the business and created the perception that growth was stagnating.

However, considering the scale of these transitions occurring all at once, the company has actually executed remarkably well.

Importantly, this quarter further disproved the narrative that the business was overly dependent on compounded GLP-1s or solely reliant on the weight loss category.

Just a year ago, many argued that the compounding transition would severely damage the company and potentially cut the subscriber base dramatically. That simply has not happened.

Instead, management now expects a meaningful reacceleration in the business, particularly within the U.S. market, which is the primary driver behind the company’s increased full-year guidance toward $3 billion in revenue.

Several developments stand out as especially important:

1. Management stated that current customer demand exceeds even prior peak periods, including some of the strongest campaigns in 2025

2. The Novo Nordisk partnership appears to be performing significantly better than expected

3. The business is aggressively investing into AI, diagnostics, personalization, wearables, and longitudinal health data

4. These investments are reinforcing the company’s competitive moat in ways that many competitors likely cannot replicate economically

5. Management believes the company is exceptionally well positioned to capitalize on the future peptide and longevity market

6. The Eucalyptus acquisition is not yet included in current guidance, providing additional upside potential

International expansion continues, while the core U.S. business itself is now reaccelerating

What is increasingly clear is that Hims & Hers is evolving far beyond a traditional telehealth company.

Management is building a vertically integrated healthcare ecosystem centered around AI, diagnostics, proactive medicine, personalization, and continuous patient engagement.

The long-term vision appears to be a platform serving tens of millions of subscribers globally, where healthcare becomes increasingly personalized, data-driven, preventative, and integrated directly into everyday life.

In my view, this business still appears to be in the very early stages of that transformation.

Gerard Pique : “I’ve played in many El Clásicos. I’ve seen great Barcelona teams, great Real Madrid teams, periods where the balance was close and periods where one side had superiority. But what we are watching right now under feels completely different.

Barcelona are not just winning these games anymore, they are controlling them emotionally, tactically and psychologically. Every time Madrid think they can compete, Barça raise the intensity and remind them who owns the game. The pressing, the movement, the confidence on the ball, the mentality… everything is on another level.

People still call it a rivalry because of the history, the badges and what El Clásico means around the world. But if you really watch the matches carefully, it doesn’t feel like a rivalry anymore. It feels like ownership. Barcelona walk into these games with authority while Madrid look nervous, reactive and dependent on moments instead of identity. That’s the biggest difference.

What impresses me most is how fearless this Barça team is. Young players demanding the ball, defenders playing high without panic, midfielders controlling the rhythm like they own the stadium. Flick has completely changed the mentality of the club. Barça don’t play El Clásico hoping to survive anymore, they play it expecting to dominate from the first minute.

And honestly, I think that hurts Madrid fans the most. Not the defeats themselves, but the feeling that Barcelona are becoming comfortable in these games again. You can lose a Clásico, that’s football. But when the other team starts treating victories over you like routine, then you know the balance of power has shifted badly.

This Barcelona side reminds me of the eras opponents feared before the match even started. That aura is coming back. Madrid still have world class players, of course they do, but collectively they don’t look close to Barça right now. Flick has built a machine that knows exactly how to expose them every single time.”

@TadekSolarz@KarelMartel7 Of ondernemers stoppen na het vergaren van 1 miljoen met hard werken, het nemen van risico’s en daarmee het creëren van werkgelegenheid , afdragen van vpb, omzetbelasting en loonbelasting. Kortom een 95% heffing leidt ertoe dat iedereen uiteindelijk slechter af is.