HardAssetAlpha focuses on how policy, geopolitics, and regulation influence capital allocation in energy, defence, and industrial markets.

For free below for anyone looking to understand how the energy market actually works beyond headlines👇👇

https://t.co/KKzSUSGllW

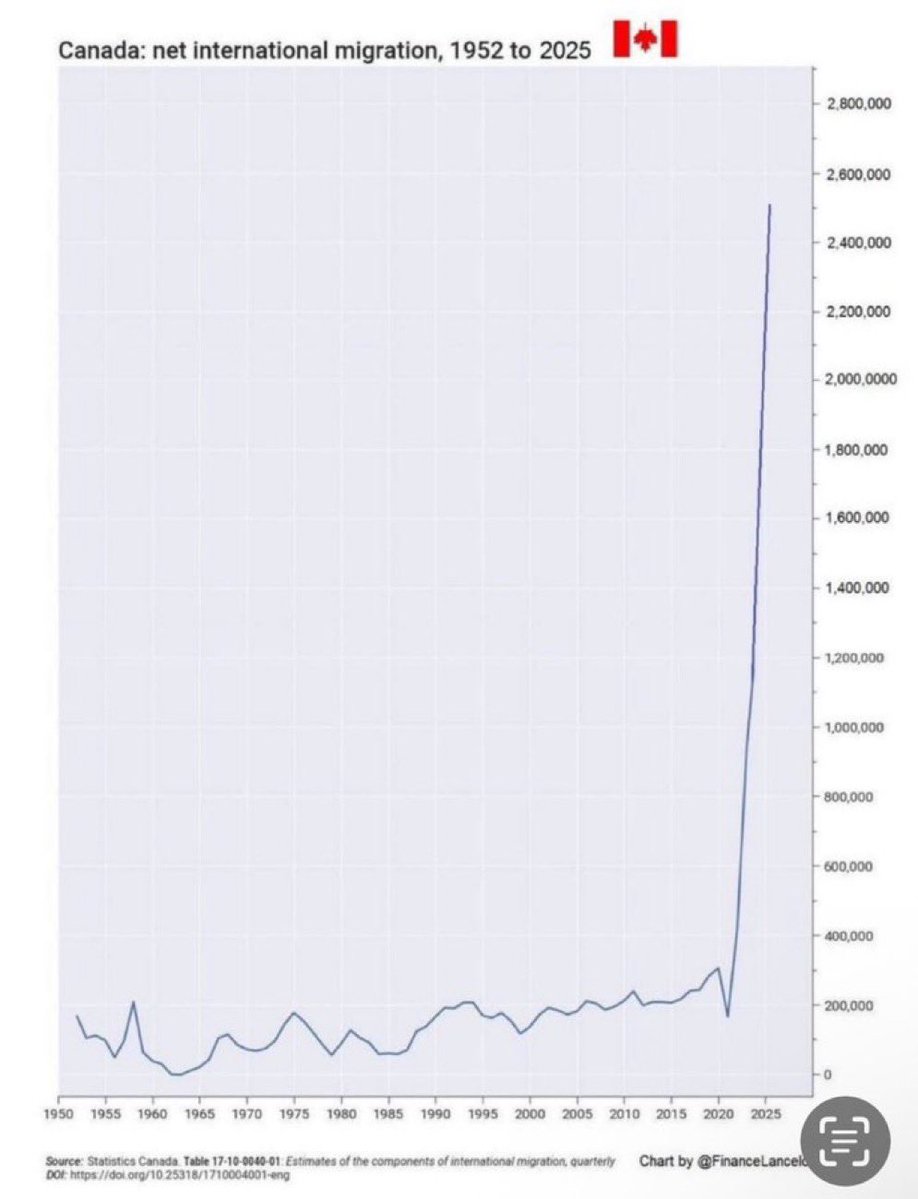

That chart is jarring, but yelling about it doesn’t really help anyone.

Canada’s population growth has clearly gone off trend, and the problem isn’t people moving here, it’s that everything else stayed stuck. Housing didn’t keep up. Infrastructure didn’t scale. Healthcare and transit were already strained. Then the numbers jumped anyway.

Until we demand aggressive trade and manufacturing in house. Say goodbye. We are NOT a tech focused economy. Mining. Metals. Ong. Real tangible good that’s have actual levers in the global balance. These goofballs will drive my generation into their graves - which at this rate will in the future USA!

•The new Fed Chair has not been warmly received. He is viewed as closely aligned with Trump and more willing to cut aggressively, which brings inflation risk back into the conversation.

•The AI trade is wobbling. Nvidia and OpenAI are clearly misaligned, adoption has been slower than early expectations, and the road to real returns is longer than markets priced.

•Microsoft continues to spend aggressively on AI capex. That investment may pay off long term, but in the near term it is pressuring margins and the stock.

•Gold and silver going parabolic was a warning. That kind of move usually signals fear and a flight to safety, not confidence.

•The Epstein tapes story has reopened questions around elite capture and policy credibility in the US. Markets do not like institutions that look compromised.

•China openly floating the yuan as a future reserve currency matters at the margin. With roughly 80 percent of countries trading more with China than the US, this is a direct challenge to dollar dominance.

•The US dollar is under pressure from multiple angles, including Japan selling and China applying leverage.

•The Supreme Court ruling on Trump’s tariffs has been delayed again. If the tariffs are struck down, it adds fuel to everything already in motion.

•US equities are not cheap. The average PE is around 31, roughly double the long term norm. Buffett has been clear there is very little he finds attractive.

•If the Fed is forced to cut, inflation risk likely resurfaces.

•Housing remains the hidden pressure point. Affordability and transaction volume never normalized, and Trump has not forgotten what triggered 2008.

•Geopolitical risk is real. Iran remains unstable. China continues to assert claims on Taiwan, which directly ties into TSM and Nvidia, the most critical node in the market today.

•Crypto is still weak. It has not proven itself as a safe haven, and negative sentiment is spreading.