Analyst on the @Hedgeye Communications Team working with @hedgeyecomm. Focused on the Video Game Industry and other internet/media names.

Not Financial Advice

Is Anthropic’s Claude a Bigger Risk to Microsoft Than Investors Think? ⚠️

Software analyst Oliver Richardson @HedgeyeCommOR and Global Technology analyst Felix Wang @HedgeyeTech debate whether Anthropic’s newly announced Claude update along with the broader rise of AI agents, could create meaningful pressure on Microsoft.

Hedgeye CEO @KeithMcCullough weighs in and reiterates his bearish signal on shares of $MSFT.

***This clip is from "The Call @ Hedgeye"

$RBLX reported a good quarter, bookings +63% compared to consensus of +53%. The problem, and why upside appears limited, is that $RBLX is a bookings growth stock. Guidance for FY 26 implies further decels throughout '26. Could turn in 4Q but that is when GTA VI releases...

@HedgeyeComm Yea at a minimum it looks like the barriers to game development are going away. $RBLX was already moving in this direction via low code studio tools, but this likely accelerates that move.

The implications for the other names are less clear and more interesting...

Call Thursday, 12/11 at 2:00pm ET $NFLX $WBD

The central question is straightforward: is this “thesis drift,” or a high-ROIC, opportunistic acceleration of Netflix’s long-term vision?

A lot of analysis and data to go though as we dive deep into the deal structure and market/industry impact.

Please contact [email protected] for access.

One complaint from $PSKY is that a meeting between $WBD and the EU where the topic of discussion was EU concerns about media concentration from a $PSKY acquisition potentially mounted to sabotage of the $PSKY offer. However, the government in the U.S. has made its preferences about who should own the $WBD assets clear. The question I would ask $PSKY management is how that is not sabotage of the $NFLX and $CMCSA offers?

Paramount is calling foul on how Warner Bros. Discovery has conducted its sale process.

In a letter reviewed by CNBC, Paramount attorneys told WBD CEO David Zaslav that Paramount was questioning the “fairness and adequacy” of the process. Read the full letter. ⬇️ https://t.co/VEc5XLmFTv

Despite reports that Call of Duty: Black Ops 7 has been underperforming the game still topped the @PlayStation November download charts. Call of Duty has been the most downloaded game in the release period as far back as the data goes. Will be interesting to see full year rankings.

Early thoughts on $RBLX: we were right to be ahead of the street on topline but reported numbers were still below what our data indicated. Commentary around tough comps in '26 and the need for further investments pressuring shares in the pre-market.

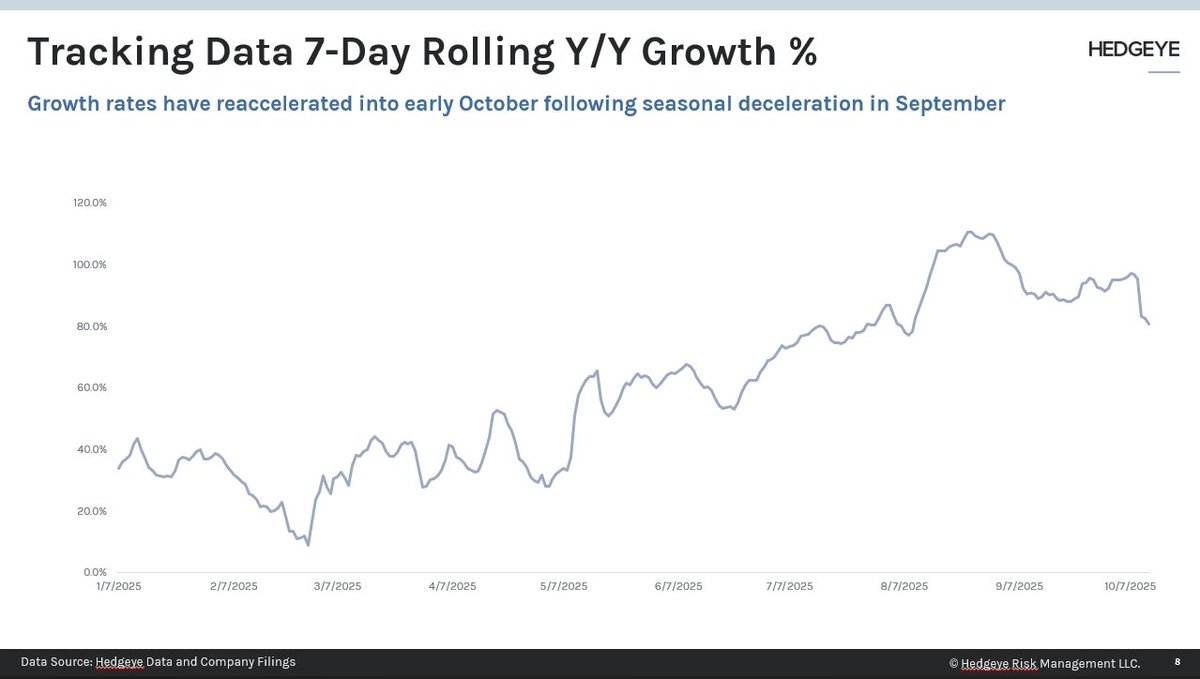

We published our Metaverse Tracker on $RBLX this morning. Trends last week were negative W/W for the second week in a row. Looking for strength through the end of the month driven by Halloween events which should show up through the end of the week.

We published our Metaverse Tracker on $RBLX today with a first look at Q4 data. October tracking to growth M/M from September. Data last week was negative compared to the prior week but trends for the month overall still looking strong particularly Y/Y.

We published our Metaverse tracker note this morning on $RBLX. The data is showing an important change in trend for the month of October. Historically October has been a fairly variable month, usually up with some exceptions, so data tracking is important here.

Here is the note for people to judge for themselves 😁 - love to know where you disagree, why are outlook is “weak” and not well substantiated? Thanks!

“We are moving SPHR from an Active Long to the Long Bench. The stock is up ~58% since we made it an active long on August 24th, in anticipation of the successful launch of The Wizard of Oz (WoZ) on August 29th, 2025. The move is driven by increasingly unattractive risk/reward, even as the data continues to track well for the show (Exhibit A). As we highlighted in our presentation on 9/19 (click here for the replay including a detailed write-up), we think fair value for shares is $70-$75 (Exhibit B), but with the stock now in the high $60s and the main catalyst, the launch of WoZ, behind us, our view is that playing this name from bench makes more sense.

The next catalysts on the calendar are potentially another MSGN renewal, likely with Fios, and the 3Q25 earnings report, which could cause some near-term volatility.

As we laid out in our presentation, the regional sports network industry is in secular decline, and MSGN already had an ugly renewal with Altice earlier this year. We are not expecting the next renewal to be positive either, as continued cord-cutting pressures subscriptions, which drives carriers to demand lower fees, negatively affecting MSGN and other RSNs.

If management were to divest MSGN ahead of this renewal or coincident with it, that would be neutral to net-positive for the equity in our view - but not something we want to bet on at $68/share.

We think that reported Q3 results could be softer within the broader context of the successful WoZ launch. While WoZ has exceeded expectations, due to the late August release the show will only impact the last 5 weeks of the quarter, with the rest of the Experience segment being made up of the older shows.

$SPHR will also not have any corporate takeovers in Q3 compared to 3 in Q2, which represents a QoQ headwind to AOI. None of this is new information, but in the context of the recent stock move, these factors may matter more in the high $60s than they did in the $40s or $50s.

In our bull case scenario, we can underwrite shares to $85+, but this is driven by consistently pushing ASPs higher in the out years along with consistently higher utilization rates in the Experience segment.

This scenario is not our base case, and we have some concerns with the 2026 Experience renewal plan, with From the Edge being planned to take over from WoZ. Our view is that WoZ, being well-known licensed IP, justified the ticketing price increase as well as helped the venue achieve and maintain the high utilization numbers we are seeing. From the Edge is an extreme sports movie, not well-known licensed IP.

We plan to continue to track the data for SPHR and provide updates, but at this point, we are happier playing this name from the long bench.”

We just published a note on $SPHR moving it from an Active Long to the Long Bench. Risk/Reward isn't as good here in the high $60s even with the WoZ data tracking well. We're happy to play upside from the bench and will continue to provide updates on the data.

@thecfcritic I model out the data monthly based on seasonality and the broader trends in the data until we are intra period and I actually have numbers. Hours engaged was surprising to me in 2Q, higher than I thought it would be, I look at it on a per DAU/per day basis.

We published our $RBLX Metaverse tracker yesterday, our DAU estimate ticked down to 143.9m for Q3. The data last week trended negatively following w/w growth the previous week. October as a month has a fair bit of variability so it will be key to watch as we start getting data.

$TTWO and $RBLX are the last 2 large public U.S. video game companies. $EA's portfolio is clearly worse than $TTWO's so what is the read through there... $RBLX is a platform and should be viewed differently imo even if games are the end product.

$EA is heavily reliant on licensed IP which is structural handicap to its margin structure, its marquee titles are over indexed to the annual release model, and Apex is dying just to name a few points.

Given that the launch of Battlefield will be a high variance outcome (it will either work or it won't) I get why $EA would want this deal, but why Silver Lake wants to own this is asset is beyond me. The core portfolio of games is not good.

Breaking: Videogame giant Electronic Arts is nearing a roughly $50 billion deal to go private in what would likely be the largest leveraged buyout of all time https://t.co/RyVt6tE55s