In case you were wondering why $APP is up 11% today... it's because Edgewater Research published a note this morning saying that $META is now unlikely to bid on non-IDFA traffic which has been one of the reasons why $APP has been lagging lately because non-IDFA traffic is a big part of $APP's competitive advantage.

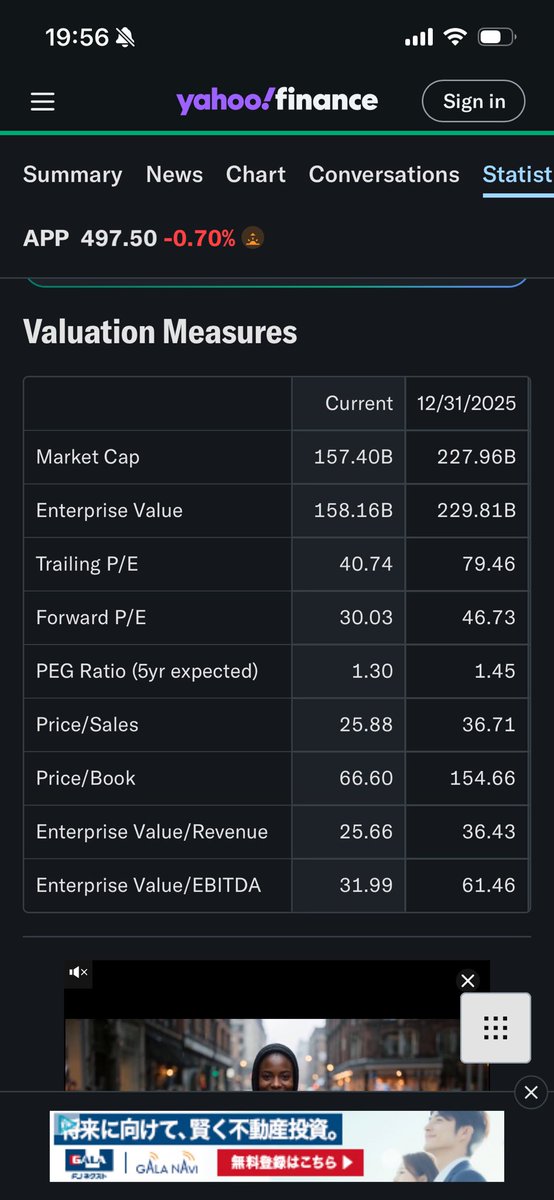

With this headwind off the table it means $APP is definitely too cheap at 25x NTM EPS with EPS growing at least 60-70% this year and probably another 40-50% next year unless their upcoming "general availability" launch goes better than expected in which case EPS next year could be up 50-60%.

Keep in mind that $APP is going to do at least $8.3B in revenues this year with just 900 employees... they have 84% ebitda margins and 72% net income margins... their SBC is only 4% of FCF... it's hard to find a more efficient company on the planet than $APP

NFA.

DYOR.

*I own $APP personally and so does @FirstWaveFund

Lumentum $LITE is under-shipping the market by >30%. Even after planning to increase capacity by 50%, the company expects the gap to widen.

That imbalance is driving pricing power, margin expansion, and EPS growth — and the $NVDA CPO ramp has barely begun. Read more below.👇

https://t.co/56L1uRo7JW

If people don’t realize why I’m so interested in $SIVE M&A.

Sivers likely customers were:

Lightmatter when they were tiny -> became $4B+ company.

Lightelligence when they were tiny -> became $10B+ company.

Ayar when they were tiny -> now funded by $NVDA, $AMD, and others.

Celestial when they were tiny -> bought by $MRVL and became their growth vector. Probably would be valued $10B+ standalone.

I’m extremely sure Sivers knows what to acquire for optical IP.

They were just stuck in a catch-22 and lacked the funding to do so originally, despite owning one of the most valuable laser chokepoints.

Future NASDAQ listing and recent growth unlocked downstream IP acquisition potential now.

Astera Labs $ALAB stock surged ~13-15% today (trading near $250) primarily because CEO and CFO comments at the J.P. Morgan Technology, Media & Communications Conference reinforced explosive AI connectivity demand. They highlighted strong Q1 results ($308M revenue, +93% YoY), upbeat Q2 guidance (~$360M), and accelerating ramps in the Scorpio family (expected to become the largest product line by year-end), plus tailwinds in optics, inference, and hyperscaler adoption—fueling investor enthusiasm for its role in scaling AI infrastructure. This positive reaffirmation acted as a clear catalyst after a recent pullback.